Smart: David was a software engineer earning $180,000 a year. He had a 401(k) that he had never once adjusted from its default allocation.

He had three credit cards carrying a combined balance of $22,000, on which he paid the minimum monthly payment while simultaneously contributing to an employer-matched retirement account, effectively borrowing at 22 percent interest to earn a 3 percent match.

His dining out expenses had tripled in the four years since his last promotion, a period during which his self-described financial security had barely moved.

He knew, in the abstract, that he was not doing this right. He had read several books about personal finance. He could explain compound interest and the power of tax-advantaged investing with some fluency.

What he could not explain, and what neither the books nor his general intelligence equipped him to understand, was why his behavior consistently diverged from what he knew.

David is not unusual. The behavioural economics literature, built substantially from the foundational work of Daniel Kahneman and Amos Tversky beginning in the 1970s, has spent fifty years documenting precisely this gap: the reliable, predictable, systematic ways in which human beings make financial decisions that contradict their own stated preferences and objectives.

These are not random errors. They are patterned failures, produced by cognitive mechanisms that were adaptive in the environments where human psychology evolved but that create significant liabilities in modern financial markets and consumer economies.

The intelligence that makes someone an excellent engineer, lawyer, or doctor does not inoculate them against these mechanisms, in some respects, it may sharpen the post-hoc rationalizations that obscure them.

The goal of this article is not to shame the David-like choices that appear in most people's financial histories.

It is to map the machinery, the specific biases, emotional processes, and cognitive shortcuts, that produce those choices, and to describe what the research suggests actually helps. Understanding the mechanisms is not sufficient to overcome them, but it is necessary.

"The investor's chief problem, and even his worst enemy, is likely to be himself.", Benjamin Graham, The Intelligent Investor (1949), a framing the behavioral economics literature has since documented in precise empirical terms

Key Definitions

System 1 and System 2 thinking: Daniel Kahneman's framework, developed through decades of research and synthesized in his 2011 book Thinking, Fast and Slow, distinguishes between System 1 (fast, automatic, emotional, intuitive processing) and System 2 (slow, deliberate, effortful reasoning).

Most financial decisions, even high-stakes ones, are made predominantly by System 1.

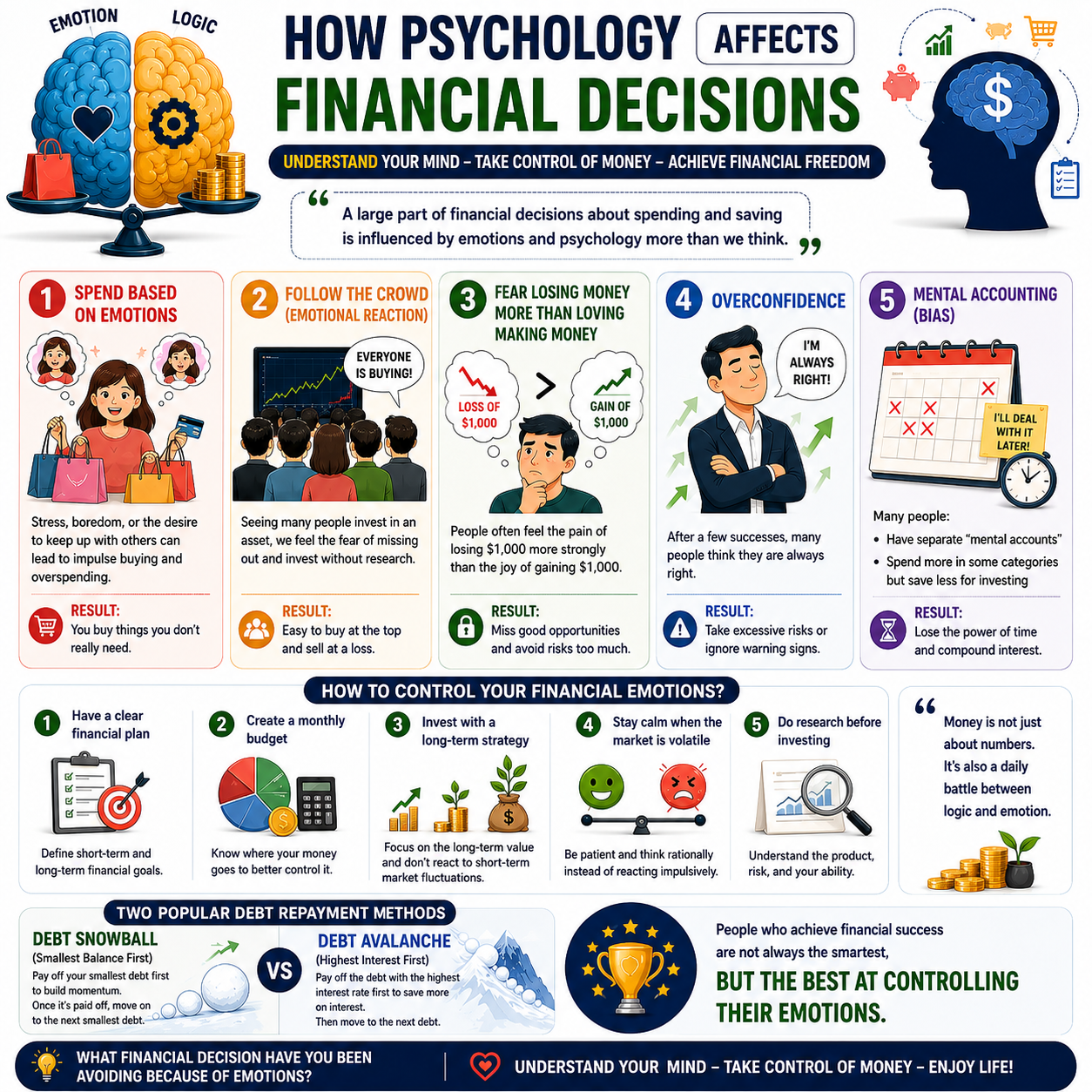

Loss aversion: The empirical finding, central to Kahneman and Tversky's 1979 prospect theory, that losses are felt approximately twice as intensely as equivalent gains. Losing $100 produces roughly the same emotional response as gaining $200.

Present bias: The tendency to overweight immediate costs and benefits relative to future ones, beyond what standard discounting would predict. Also called hyperbolic discounting, it produces the consistent preference for smaller-sooner rewards over larger-later ones.

Mental accounting: Richard Thaler's concept describing the psychological tendency to treat money differently depending on its source, category, or intended use, as if money kept in separate mental "accounts" has different properties despite being perfectly fungible.

Sunk cost fallacy: The tendency to continue investing resources (money, time, effort) in a course of action because of what has already been spent, rather than making decisions based solely on future expected returns.

Common Cognitive Biases in Financial Decision-Making

| Bias | Description | Financial Example | Consequence |

|---|---|---|---|

| Loss aversion | Losses feel ~2x more painful than equivalent gains | Holding losing stocks too long to avoid realizing a loss | Suboptimal portfolio returns |

| Present bias | Overweight immediate rewards vs. future ones | Spending today rather than saving for retirement | Retirement savings gap |

| Mental accounting | Treat money differently based on its source or label | Spending a "bonus" freely but saving regular income | Fails to optimize total wealth |

| Sunk cost fallacy | Continue because of past investment, not future value | Keeping a bad investment to "recover" original cost | Deepens losses |

| Overconfidence | Overestimate ability to pick winning investments | Frequent active trading based on own "insight" | Transaction costs erode returns |

| Status quo bias | Prefer doing nothing over making a change | Never adjusting default 401(k) allocation | Suboptimal asset allocation |

Prospect Theory and the Asymmetry of Gains and Losses

The single most influential finding in the behavioral economics of money is also, in some ways, the most counterintuitive. In a rational model of financial decision-making, a $100 gain and a $100 loss should register with equal magnitude, opposite in direction but equal in weight.

Kahneman and Tversky's prospect theory, first published in Econometrica in 1979, demonstrated systematically that this is not how human beings actually process financial outcomes.

The value function in prospect theory is S-shaped and asymmetric. Gains produce diminishing marginal satisfaction relatively quickly, the difference between gaining $100 and gaining $200 feels meaningful, but the difference between gaining $1,000 and gaining $1,100 feels modest.

Losses, by contrast, produce a steeper emotional response and diminishing marginal pain more slowly. And the entire curve is kinked at the reference point, the current position, with the loss side dropping more steeply than the gain side rises.

The practical consequences of this asymmetry are substantial. In investing, loss aversion produces what behavioral finance researchers call the disposition effect: the tendency to sell winning investments too early (locking in gains before they can reverse into losses) and hold losing investments too long (refusing to realize a loss).

Brad Barber and Terrance Odean documented this pattern in a landmark 2001 study analyzing 35,000 brokerage accounts over six years.

Not only did most individual investors trade more than was optimal, generating costs that eroded returns, but their trading was systematically asymmetric in precisely the way loss aversion predicts: they sold winners at twice the rate they sold losers.

The disposition effect is irrational in a purely financial sense. A stock trading below your purchase price should be evaluated on its future prospects, not its history relative to your entry point. The fact that you paid more for it is economically irrelevant to what it will do next.

But psychologically, it is intensely relevant: selling at a loss requires acknowledging failure, crystallizing a bad decision into a realized fact. The unrealized loss exists in a state of painful but uncertain suspension, perhaps the stock will recover, perhaps the decision was not truly wrong.

Selling closes that ambiguity permanently and painfully.

Present Bias: Why the Future Always Loses

If loss aversion explains why people make poor decisions in markets, present bias explains why they make poor decisions about savings, debt, and long-term planning.

The psychological concept, formalized in economics as hyperbolic discounting, describes the characteristic shape of human intertemporal preferences: people discount the future not at a constant rate (as standard economic models assumed) but at a steeply declining rate, with the sharpest discount applied to the near future.

This means that the difference between receiving $100 today versus $110 in a week feels very large, most people would choose the $100 now. But the difference between $100 in a year versus $110 in a year and a week feels small, most people would wait the extra week for $110.

The objective difference between the choices is identical. The psychological difference is not.

For personal finance, this produces what economists call the retirement savings gap. The benefits of saving, financial security in decades' time, are maximally discounted by a brain that evolved to prioritize immediate survival.

The costs of spending, depleting resources now, are immediate and concrete. Every act of saving requires overriding present bias. Every act of consumer spending is facilitated by it.

The research of Richard Thaler and Shlomo Benartzi on "Save More Tomorrow", a program that committed participants to automatically increase their savings rate with future pay raises, addressed this asymmetry ingeniously.

Because the savings increases were linked to future raises (not requiring any current sacrifice) and were automatic (removing the need for repeated decisions), enrollment resulted in dramatically increased savings rates without requiring participants to overcome present bias directly.

The program's success, average savings rates tripled over four years in the original cohort, demonstrated that understanding the bias enables designs that work with it rather than against it.

Mental Accounting: The Fiction of Money's Categories

Richard Thaler's concept of mental accounting, developed through a series of papers beginning in the 1980s, describes one of the most practically consequential findings in behavioral economics: people treat money as if it exists in separate, non-fungible accounts based on its source, intended purpose, or arbitrary categorization, even though money is in reality perfectly interchangeable.

The most straightforward demonstration involves windfall income. Research consistently shows that people treat unexpected income, a tax refund, a bonus, a gift, as "different" money than their regular income and are more likely to spend it on luxuries or indulgences than equivalent regular income would be.

This is economically incoherent: a dollar from a tax refund has exactly the same purchasing power and opportunity cost as a dollar from a paycheck. But it does not feel that way, and behavior follows feeling.

The consequences compound in credit card behavior. Thaler and others have documented that paying with credit cards reliably increases spending relative to paying with cash, and increases it by more than the convenience explanation would predict.

The mechanism appears to involve mental accounting: cash feels more "real" and its loss more salient, while credit card expenditure is abstracted into a future categorical expense that feels less immediately costly. Casino chips operate on the same principle.

For David from our opening, the most relevant manifestation of mental accounting may have been his treatment of retirement contributions and credit card debt as separate mental accounts, the first virtuous, the second manageable, rather than recognizing that the net financial effect of simultaneously earning 3 percent (retirement) and paying 22 percent (credit card interest) was deeply negative.

The Scarcity Trap

Sendhil Mullainathan, an economist at Harvard University, and Eldar Shafir, a psychologist at Princeton, collaborated on what may be the most important reframing of financial decision-making in recent decades: their 2013 book Scarcity: Why Having Too Little Means So Much.

Their central argument, supported by both laboratory experiments and field research in low-income contexts, is that scarcity of any resource, time, money, calories, social connection, captures cognitive bandwidth in ways that impair judgment about everything else.

When people are preoccupied with financial scarcity, making ends meet, managing overdraft fees, avoiding collection calls, that preoccupation consumes working memory and attention.

The result is not simply poor decisions about money; it is a measurable reduction in cognitive capacity available for anything requiring deliberate, System 2 reasoning, including the long-term thinking that financial planning requires.

Mullainathan and Shafir demonstrated this with a striking field experiment: poor farmers in India showed lower cognitive performance on standard IQ-style tests before their annual harvest (a time of financial anxiety and scarcity) than after, with a difference equivalent to roughly 13 IQ points.

The implication challenges a narrative common in financial advice culture: the framing of poverty and financial distress as primarily the result of poor decision-making.

Mullainathan and Shafir's data suggests the causality runs at least partly in the other direction, financial distress impairs the cognitive capacity for good decision-making, creating a feedback loop that is genuinely difficult to break without structural intervention.

Overconfidence and the Trading Trap

Overconfidence bias, the tendency to overestimate the accuracy of one's knowledge, predictions, and skills, is one of the most extensively documented biases in the psychological literature, and one of the most financially costly.

Barber and Odean's 2001 study of individual investors, mentioned earlier, found that men traded approximately 45 percent more than women, generating higher transaction costs and earning significantly lower net returns.

Further analysis attributed much of this differential to overconfidence: men showed greater belief that their investment choices would outperform the market, which led to more frequent trading based on those convictions.

The more confident investors traded, the more their costs eroded any skill advantage they might have had.

In a 2000 study, Barber and Odean examined what happened when investors switched from phone-based trading to online trading, a shift that removed friction from the decision to trade. Trading volume increased by 67 percent post-switch. Net returns decreased. The ease of acting on overconfident judgments amplified the damage.

Social Comparison and Lifestyle Inflation

Morgan Housel, in his 2020 book The Psychology of Money, identifies what he calls the paradox of visible wealth: people buy expensive cars and designer goods to signal wealth to others, but the observers they are trying to impress are imagining themselves in those goods, not admiring the owner.

The admiration that drives conspicuous spending does not actually accrue to the spender in the way they anticipate.

Behind this observation lies a substantial literature on social comparison and its financial consequences. Relative income, how one earns compared to peers, predicts subjective financial wellbeing more strongly than absolute income in most studies.

This means that a pay raise that puts you above your reference group improves wellbeing, while a pay raise that simply keeps pace with a rising tide does not. And because the reference group shifts upward with income, higher earners compare themselves to other higher earners, the effect tends to be self-negating.

Lifestyle inflation is the behavioral consequence. As income rises, so do expenditure standards, driven partly by hedonic adaptation (the normalization of improvements) and partly by comparison with the visible consumption of peers at the new income level.

The result, documented across multiple longitudinal income studies, is that many high earners maintain savings rates that are not substantially better than lower earners relative to income, the additional earnings are absorbed by expanded consumption before they reach savings.

The Planning Fallacy

Daniel Kahneman and Amos Tversky identified the planning fallacy in 1979: the systematic tendency to underestimate the time, cost, and effort required to complete future projects, even while having accurate knowledge of how similar past projects went.

The kitchen renovation that was budgeted at $15,000 ends up costing $24,000. The emergency fund that will take "six months" to build takes two years.

In personal finance, the planning fallacy manifests most consequentially in debt accumulation.

People take on debt based on optimistic projections of future income and expense, failing to properly account for irregular costs (car repairs, medical bills, broken appliances) that are, in aggregate, entirely predictable even if individually uncertain.

The result is a structural underestimation of the cost of life that leaves people chronically short.

Kahneman's proposed remedy, the "outside view," which replaces optimistic subjective projections with base rate data about how similar situations typically resolve, is applicable to personal financial planning.

Asking "what do emergency expenses actually average for a household with this profile" rather than "what do I think my emergency expenses will be this year" generates more accurate predictions, even though most people find the question unnatural.

Practical Takeaways

Automate savings before spending. Pre-commitment devices sidestep present bias by making the decision once rather than requiring daily willpower. Automatic transfers on payday that move savings out of reach before they can be spent are among the most empirically robust financial interventions.

Create explicit selling rules before you invest. Decide in advance at what price or under what conditions you will sell an investment, both to take profits and to cut losses. This decision, made before emotion is engaged, is more likely to be rational than a decision made after you have watched a position decline for months.

Pay with cash or debit for discretionary spending. The reduced abstraction of cash payment activates loss aversion beneficially, making discretionary spending feel more costly and reducing impulse purchases relative to credit card payment.

Ignore the visible consumption of peers. Social comparison of spending is almost always comparing your reality to someone else's highlight reel, and frequently comparing yourself to people whose visible consumption is financed by debt rather than wealth.

Build financial slack. Mullainathan and Shafir's research suggests that even a modest financial buffer, enough to handle common unexpected expenses without crisis, measurably improves cognitive function for financial decision-making. The first savings goal is not retirement; it is enough slack to think clearly.

Get the outside view on major expenses. Before committing to a large financial decision, research what similar decisions have actually cost other people, not what you expect this one will cost you.

Sources & Further Reading

- Kahneman, D., & Tversky, A. (1979). Prospect theory: An analysis of decision under risk. Econometrica, 47(2), 263-292.

- Kahneman, D. (2011). Thinking, Fast and Slow. Farrar, Straus and Giroux.

- Thaler, R. H. (1999). Mental accounting matters. Journal of Behavioral Decision Making, 12(3), 183-206.

- Barber, B. M., & Odean, T. (2001). Boys will be boys: Gender, overconfidence, and common stock investment. Quarterly Journal of Economics, 116(1), 261-292.

- Barber, B. M., & Odean, T. (2000). Trading is hazardous to your wealth: The common stock investment performance of individual investors. Journal of Finance, 55(2), 773-806.

- Mullainathan, S., & Shafir, E. (2013). Scarcity: Why Having Too Little Means So Much. Times Books.

- Thaler, R. H., & Benartzi, S. (2004). Save More Tomorrow: Using behavioral economics to increase employee saving. Journal of Political Economy, 112(S1), S164-S187.

- Housel, M. (2020). The Psychology of Money. Harriman House.

- Kahneman, D., & Tversky, A. (1979). Intuitive prediction: Biases and corrective procedures. Management Science, 12, 313-327.

- Loewenstein, G., & Prelec, D. (1992). Anomalies in intertemporal choice: Evidence and an interpretation. Quarterly Journal of Economics, 107(2), 573-597.

- Frank, R. H., Levine, A. S., & Dijk, O. (2014). Expenditure cascades. Review of Behavioral Economics, 1(1-2), 55-73.

- Shefrin, H., & Statman, M. (1985). The disposition to sell winners too early and ride losers too long: Theory and evidence. Journal of Finance, 40(3), 777-790.

Related reading: Why People Procrastinate: The Psychology Behind Putting Things Off | Why Relationships Fail: What Research Actually Says

Frequently Asked Questions

Why do people spend money they don't have?

Several mechanisms converge. Present bias makes immediate gratification feel vastly more valuable than future security. Social comparison pressures drive spending to match peers whose income or assets may be invisible. Mental accounting allows people to treat credit card money as ‘different’ from cash. And scarcity mindset, documented by Mullainathan and Shafir, can narrow cognitive bandwidth in ways that impair long-term financial reasoning.

What is loss aversion and how does it affect financial decisions?

Loss aversion, established by Daniel Kahneman and Amos Tversky in their 1979 prospect theory research, describes the finding that losses feel approximately twice as painful as equivalent gains feel pleasurable. In financial terms, losing \(100 generates roughly the same emotional intensity as gaining \)200. This asymmetry leads people to hold losing investments too long, avoid selling at a loss even when rational, and make overly conservative decisions to prevent any loss at all.

Why do people stay in bad investments too long?

The sunk cost fallacy drives continued investment in failing positions because the losses already incurred feel like they must be ‘recovered.’ Loss aversion makes selling at a loss emotionally very costly. And overconfidence, documented extensively by Barber and Odean in their 2001 study of 35,000 brokerage accounts, leads investors to believe their judgment is correct even when the market is delivering contrary evidence.

How does stress and scarcity affect financial decision-making?

Sendhil Mullainathan and Eldar Shafir’s 2013 book ‘Scarcity’ documents how the experience of financial scarcity captures cognitive bandwidth, leaving less mental capacity for long-term planning and impulse control. People under financial stress are not simply making poor choices due to bad values; their cognitive capacity for resisting short-term temptations is demonstrably reduced by the preoccupation with meeting immediate needs.

Why do high earners still feel broke?

Lifestyle inflation is the primary mechanism: spending tends to expand to match income, driven by hedonic adaptation (the rapid normalization of improvements in living standards) and social comparison (spending to match the visible consumption of peers at the new income level). Morgan Housel also identifies the trap of conflating visible wealth with actual wealth, the person driving the expensive car may have very little net worth.

What cognitive biases most damage personal finances?

The most consequential are: present bias (overweighting immediate costs and benefits), loss aversion (refusing to cut losses on bad investments), overconfidence (excessive trading, underestimating costs), mental accounting (treating money differently based on its source or category), and the planning fallacy (systematically underestimating how much things will cost and how long they will take).

How can you make better financial decisions?

Pre-commitment devices, automating savings so the decision is made once rather than daily, sidestep present bias. Investment rules that specify when you will sell before buying sidestep loss aversion and sunk cost reasoning at the moment of decision. Exposure to actual financial data about peer wealth (not just consumption) reduces social comparison distortions. And building basic financial literacy reduces the information gaps that make System 1 thinking fill the void with biases.