Effective: A budget is a structured plan that allocates income across spending categories, savings goals, and debt repayment before the money is spent - transforming financial decisions from reactive impulses into deliberate choices.

Most budgets fail within three months, not because the people who made them lacked discipline, but because most budgeting advice ignores the behavioral science of why people spend the way they do.

This guide covers the most proven budgeting methods, why budgets break down, and what the research actually shows about making a spending plan you will stick to.

Why Budgeting Matters More Than You Think

A budget is not a punishment. It is the most direct tool you have for aligning your spending with what you actually value. Without one, spending defaults to habit, impulse, and the path of least resistance - which is rarely the same as your stated financial goals.

The data on unbudgeted households is stark. According to a 2022 survey by the National Foundation for Credit Counseling, only 37 percent of American adults maintained a detailed written budget. Among those who did, the average savings rate was nearly double that of non-budgeters.

A separate 2023 survey by Ramsey Solutions found that 74% of Americans who follow a written budget report feeling "in control" of their finances, compared to only 35% of those without one. The difference was not income - it was intentionality.

The Federal Reserve's 2023 Survey of Household Economics and Decisionmaking (SHED) found that 37% of Americans could not cover an unexpected $400 expense without borrowing or selling something.

This figure has improved only marginally since the Fed began tracking it in 2013 (when it was 50%), despite significant income growth over that period.

The persistent gap between income growth and financial resilience suggests that the problem is not primarily about earning more - it is about directing what is earned.

Budgeting is not about restricting your life. It is about directing it.

The Core Problem: Why Budgets Break Down

Before choosing a method, it helps to understand the behavioral forces working against any budget you build. These are not character flaws - they are well-documented cognitive patterns that affect virtually everyone, and understanding them is closely related to understanding the cognitive biases that shape our decisions more broadly.

Present Bias

Present bias is the documented tendency to overweight immediate rewards relative to future ones, even when the person consciously prefers the future outcome. It explains why someone can genuinely want to save for a house and still choose the weekend trip.

Nobel laureate Richard Thaler and economist Shlomo Benartzi demonstrated in their landmark 2004 research, published in the Journal of Political Economy, that present bias is the primary driver of undersaving, and that the most effective solution is removing the decision - through automation - rather than trying to overcome the bias through willpower.

The neuroscience behind present bias is well-established. Research by Samuel McClure, David Laibson, and colleagues at Princeton, published in Science (2004), found that immediate rewards activate the brain's limbic system (associated with emotional and impulsive responses), while delayed rewards primarily activate the prefrontal cortex (associated with deliberate reasoning).

The limbic system often wins the competition, especially when a person is tired, stressed, or cognitively depleted - which describes most people at the end of a workday facing spending decisions.

Optimism Bias in Expense Estimation

Most budgets fail because they are built around average months in a life that contains few average months. Car repairs, dental work, home maintenance, travel for weddings or funerals, holiday gifts - these feel like surprises, but they are predictably irregular.

Financial planner Carl Richards, author of The Behavior Gap (2012), calls this the "irregular expense problem," and research by the Consumer Financial Protection Bureau (CFPB) found that households consistently underestimate annual expenses by 20 to 30 percent when planning month-to-month.

A 2017 study by Sussman and Alter in the Journal of Marketing Research found that people systematically underestimate how much they will spend in the future, even when they have accurate records of past spending.

The researchers termed this the "expense prediction bias" and found it was strongest for categories where spending is variable and emotionally driven - precisely the categories that blow up budgets.

Tracking Fatigue

Highly granular budgets, where every transaction is categorized and reviewed, require sustained cognitive effort that most people cannot maintain across months.

A 2019 study by Olafsson and Pagel in the Journal of Marketing Research found that people who tracked spending at a high level of detail reported greater financial stress and eventually abandoned tracking entirely at higher rates than those using broader categories.

The paradox is that the people who need the most detail are the ones least able to sustain the effort.

The Unexpected Expense Demolition

A single large unexpected expense can blow up a budget so completely that the person abandons the entire system. Psychologists call this the "what the-hell effect" (formally: counterregulatory eating, but the principle extends beyond dieting).

Research by Cochran and Tesser (1996) documented that when people violate a self-imposed rule, the violation often triggers a complete abandonment of the rule rather than a proportional adjustment.

A robust budget builds in what are called sinking funds - monthly contributions to irregular expense categories so the money exists when the need arises.

The Three Main Budgeting Methods

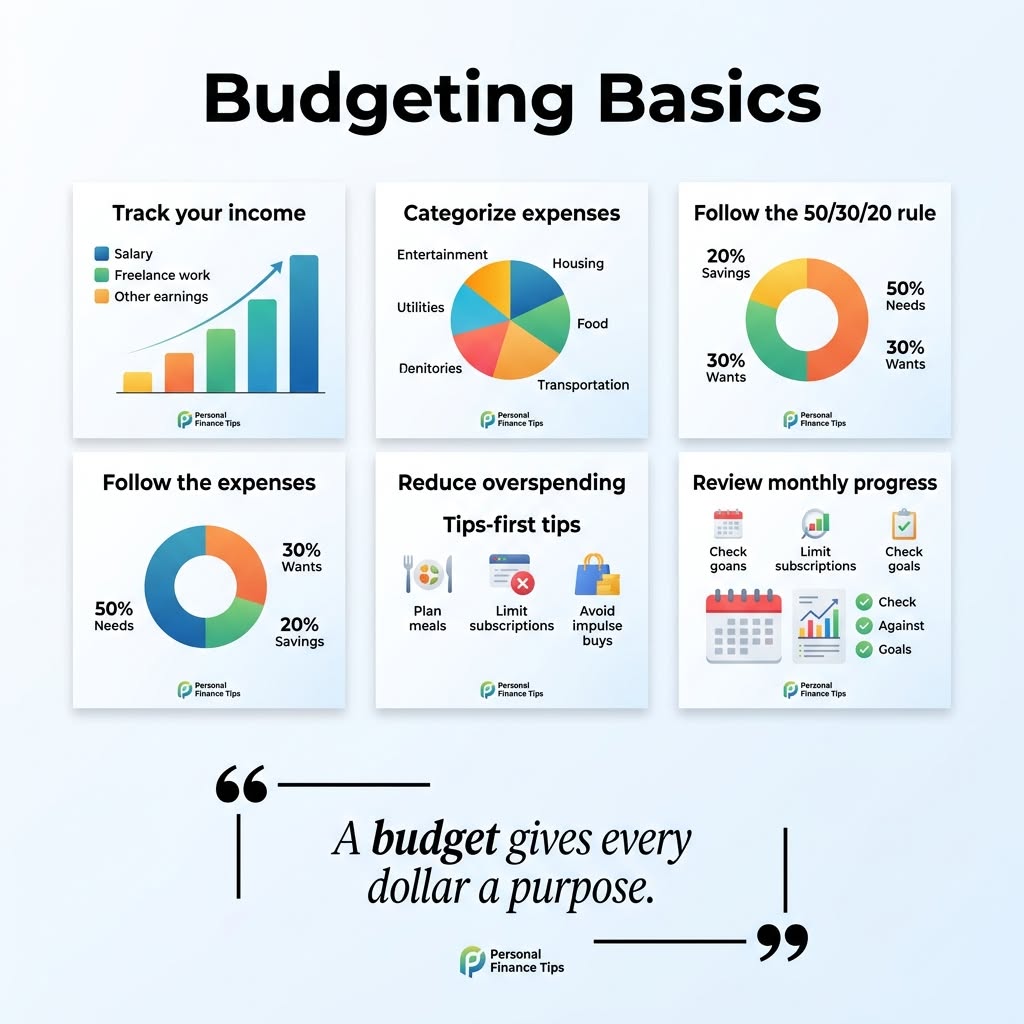

Method 1: The 50/30/20 Rule

The 50/30/20 rule was introduced by Senator Elizabeth Warren and her daughter Amelia Warren Tyagi in their 2005 book All Your Worth: The Ultimate Lifetime Money Plan.

Warren, then a Harvard bankruptcy law professor, developed it after studying over 2,000 bankruptcy filings and identifying that financially resilient households tended to allocate income across three broad categories in roughly these proportions.

| Category | Percentage | What It Covers | Warning Signs |

|---|---|---|---|

| Needs | 50% | Housing, utilities, groceries, insurance, minimum debt payments, transportation to work | Over 60% signals financial vulnerability |

| Wants | 30% | Dining out, entertainment, travel, subscriptions, clothing beyond basics | Under 10% signals unsustainably restrictive budget |

| Savings / Debt | 20% | Emergency fund, retirement, investments, extra debt repayment | Under 10% indicates inadequate wealth building |

How to implement it:

- Calculate your monthly after-tax income (take-home pay plus any side income).

- Multiply by 0.50, 0.30, and 0.20 to get your three category targets.

- Review your last three months of spending and assign each transaction to needs, wants, or savings.

- If any category significantly exceeds its target, identify the largest line items within it.

The 50/30/20 rule's strength is simplicity. It does not require tracking individual transactions - only periodic checks at the category level.

Research by Iyengar and Lepper at Columbia University (2000), published in the Journal of Personality and Social Psychology, demonstrated that excessive choice paralyzes decision-making - a finding that extends to budgeting. Three categories are manageable; thirty are not.

Limitations in high cost-of-living areas: In cities like San Francisco, New York, or London, housing alone often consumes 35 to 50 percent of take-home pay.

According to the National Low Income Housing Coalition's 2023 Out of Reach report, a full-time worker needs to earn $28.58 per hour to afford a modest two-bedroom rental at fair market rent in the US - meaning millions of workers cannot achieve the 50% needs target without relocation or significant income change.

Warren herself addressed this: if needs genuinely cannot be reduced below 50 percent, treat the 50/30/20 as an aspiration rather than a current constraint, and focus on incrementally improving the ratio over time.

Method 2: Zero-Based Budgeting

Zero-based budgeting (ZBB) assigns every dollar of income a specific purpose before the month begins, so that:

Income - All Allocations = $0

This does not mean spending everything. Savings, investments, and debt repayment each receive explicit allocations. The zero simply means no dollar is unaccounted for.

ZBB originated in corporate accounting - Peter Pyhrr developed it at Texas Instruments in the 1970s, and it was adopted by the Carter administration for federal budgeting in 1977.

It was adapted for personal finance by financial educators including Dave Ramsey and, more elaborately, by Jesse Mecham, who built the YNAB (You Need A Budget) software platform around it.

Mecham articulated ZBB as four rules: give every dollar a job, embrace your true expenses, roll with the punches, and age your money.

How to implement ZBB:

- Start with your total expected income for the month.

- List all fixed expenses (rent, insurance premiums, loan minimums, subscriptions).

- List variable necessities (groceries, gas, utilities - estimated based on past months).

- Allocate savings and investment goals.

- Distribute remaining income across discretionary categories with specific limits.

- If you run out of income before all categories are funded, reduce allocations to lower-priority categories.

The critical addition: sinking funds for irregular expenses. Every ZBB should include monthly contributions to sinking funds for categories like:

- Car maintenance and repairs

- Medical and dental costs

- Home maintenance (renters: replacement of appliances, furniture)

- Holiday gifts

- Annual subscriptions or memberships

A household that budgets $100 per month into a "car" sinking fund will have $1,200 available when the alternator fails. The repair does not blow up the budget. This is the budgeting equivalent of building a feedback loop into a system - creating a mechanism that absorbs shocks rather than transmitting them.

Research on ZBB users: A 2020 analysis of YNAB users, published on the company's website with data from over 100,000 accounts, found that new users paid off an average of $6,100 in debt and saved an average of $6,200 in their first year of use.

While this data comes from YNAB itself and may reflect self-selection (people who adopt ZBB may be more financially motivated to begin with), it aligns with broader research by Fernandes, Lynch, and Netemeyer (2014) showing that structured financial tools improve outcomes more than financial education alone.

Method 3: The Envelope Method

The envelope method involves physically dividing cash into labeled envelopes for each discretionary spending category. When an envelope is empty, spending in that category stops.

"The cash envelope system works because it turns an abstract digital number into a tangible, finite resource." - Dave Ramsey, The Total Money Makeover (2003)

The behavioral mechanism is the pain of paying: research by Drazen Prelec and Duncan Simester at MIT, published in Marketing Science (2001), found that people spend up to 100 percent more when paying by credit card versus cash, because the psychological cost of handing over physical bills is more immediate and salient than a future credit card charge.

The envelope method exploits this directly.

Additional research by Raghubir and Srivastava (2008) in the Journal of Experimental Psychology confirmed that the physical form of payment affects spending behavior independently of income or financial literacy.

People consistently spend less with cash, spend more with credit cards, and spend intermediate amounts with debit cards. The envelope method leverages this hierarchy.

How to implement it:

- Identify 4 to 8 discretionary categories where you tend to overspend (groceries, dining, entertainment, clothing, personal care, etc.).

- On payday, withdraw cash for each category and place it in labeled envelopes.

- When paying in that category, take money only from the envelope.

- When the envelope is empty, stop spending in that category until next payday.

Digital alternatives: Apps like Goodbudget, Mvelopes, and the envelope allocation system within YNAB replicate the envelope logic without requiring physical cash, making them compatible with a mostly cashless lifestyle.

The digital version is less behaviorally potent than physical cash but still meaningfully better than no categorical limits.

Best for: People who have a specific problematic category (grocery overspending, dining out, impulse online shopping) and want a simple constraint without rebuilding their entire financial system.

How to Choose the Right Method

| If You... | Try This Method | Why It Fits |

|---|---|---|

| Want simplicity and hate tracking | 50/30/20 rule | Only 3 categories to monitor |

| Want total control over every dollar | Zero-based budgeting | Every dollar has a named purpose |

| Overspend in 1-3 specific categories | Envelope method | Physical/digital constraints on problem areas |

| Have variable income (freelance, commission) | Zero-based budgeting with income floors | Budget against minimum, allocate surplus |

| Are paying off significant debt | Zero-based budgeting or envelope method | Forces explicit debt allocation decisions |

| Are a couple with different spending styles | 50/30/20 macro + envelopes for conflict categories | Simplicity at the macro level, control where needed |

There is no rule against combining methods. Many effective budgeters use the 50/30/20 framework at the macro level while applying envelope limits to their two or three historically problematic categories.

The key insight from decision-making research is that the best system is one you actually use, not the theoretically optimal one you abandon.

The Automation Imperative

The single most evidence-backed intervention in personal finance is automation. Richard Thaler and Shlomo Benartzi's Save More Tomorrow (SMarT) program, published in the Journal of Political Economy in 2004, is the landmark study.

By automatically enrolling employees in a retirement savings program that incrementally increased contributions at each pay raise, the program raised average savings rates from 3.5 percent to 11.6 percent - without requiring any active decisions after initial enrollment.

The mechanism: automation removes the decision entirely, bypassing present bias rather than fighting it.

The effectiveness of automation has been confirmed repeatedly. Chetty et al. (2014), in a study of Danish tax records covering 4.1 million observations published in the Quarterly Journal of Economics, found that automatic contributions to retirement accounts increased total savings by almost exactly the amount of the automatic contribution, with minimal offsetting reduction in voluntary savings.

In other words, automation creates genuinely new savings rather than simply shifting money between accounts.

Practical automation steps:

- Set up a direct deposit split so savings go directly to a separate account before you see the money. Most employers and banks support this. The money you never see is money you never miss.

- Schedule automatic transfers to retirement accounts, emergency funds, and investment accounts on the day after payday. Not the day of - the one-day delay provides a buffer for deposit timing.

- Pay fixed bills automatically to avoid late fees and the cognitive overhead of manual payments. The CFPB estimates that Americans pay over $12 billion annually in late fees on credit cards alone.

- Review automation settings quarterly, not monthly. Monthly reviews of automated systems create the temptation to intervene, which defeats the purpose.

Ramit Sethi, author of I Will Teach You to Be Rich (2009, revised 2019), calls this "paying yourself first" and argues it is more powerful than any spending restriction, because it makes saving the default rather than the deliberate choice.

Behavioral economists call this leveraging the default effect - the well-documented finding that people disproportionately stick with whatever option is the default, a principle explained in depth in Thaler and Sunstein's Nudge (2008).

Building Your Budget Step by Step

Step 1: Know Your Numbers

You cannot budget without accurate income and expense data. For one full month before starting any method, track every transaction. Most banking apps and tools like Monarch Money, Copilot, or YNAB automatically categorize spending. The goal is not to change behavior yet - only to see reality clearly.

Research by Kast, Meier, and Pomeranz (2018) found that the simple act of tracking spending - without any other intervention - reduced discretionary spending by 4 percent, suggesting that awareness itself has behavioral effects.

Step 2: Calculate Real Monthly Income

For salaried employees, this is take-home pay after taxes and benefits deductions. For variable income earners - freelancers, commission-based workers, seasonal employees - use the lowest typical monthly income from the past 12 months, not the average.

Budget against the floor; treat above-floor income as bonus allocations. This approach is what financial planners call "income smoothing" and it prevents the most common budgeting failure for variable-income households: building plans around peak months and then failing during troughs.

Step 3: List Fixed and Variable Expenses

Separate expenses into:

- Fixed expenses: Same amount every month (rent/mortgage, loan payments, insurance premiums, subscriptions with annual billing divided by 12)

- Variable necessities: Fluctuate but are required (groceries, utilities, transportation fuel, medications)

- Discretionary spending: Choices about lifestyle (dining, entertainment, clothing, hobbies)

The Bureau of Labor Statistics' 2023 Consumer Expenditure Survey provides useful benchmarks for how the average American household allocates spending: housing 33%, transportation 16%, food 13%, insurance/pensions 12%, healthcare 8%, entertainment 5%, and all other categories 13%.

If your allocation in any category differs dramatically from these benchmarks, that difference should be a conscious choice, not an unnoticed drift.

Step 4: Build in Sinking Funds

Before allocating to discretionary spending, estimate annual irregular expenses and divide by 12. Common sinking fund categories:

| Category | Typical Annual Cost (US, 2024) | Monthly Contribution | Source |

|---|---|---|---|

| Car maintenance | $500-$1,500 | $42-$125 | AAA 2024 driving cost study |

| Medical/dental | $500-$2,000 | $42-$167 | Kaiser Family Foundation |

| Home/renter maintenance | $500-$3,000 | $42-$250 | HomeAdvisor annual data |

| Holiday gifts | $300-$1,500 | $25-$125 | National Retail Federation |

| Travel | $1,000-$5,000 | $83-$417 | Bureau of Labor Statistics |

| Annual subscriptions | $200-$800 | $17-$67 | Your own subscription audit |

Step 5: Check the Math

Total all allocations. If they exceed income, cut discretionary spending first, then sinking fund contributions temporarily. If income exceeds allocations, assign the surplus explicitly - to debt payoff, savings, or a specific goal - rather than leaving it as a vague surplus that typically evaporates.

Research by Cheema and Soman (2008), published in the Journal of Consumer Research, found that earmarking money for specific purposes significantly reduces the likelihood of it being spent on unrelated impulse purchases.

Step 6: Review Monthly, Adjust Quarterly

A budget is a living document, not a one-time exercise. Monthly reviews should take 20 to 30 minutes: compare actual spending to allocations, identify variance, and ask whether the variance was one-off or systematic.

Systematic variances (grocery spending consistently over budget by $80 per month) indicate the allocation needs adjusting, not that willpower must be increased.

This iterative adjustment process is a form of feedback loop - the same mechanism that makes complex systems adaptive rather than rigid.

Quarterly reviews should be more substantive: reassess income changes, life changes (new child, new job, move), and whether the overall framework still fits. The goal is a budget that evolves with your life rather than one that becomes increasingly disconnected from reality until it is abandoned.

Common Budgeting Mistakes

Budgeting net income instead of gross: Some expenses (retirement contributions, health insurance premiums) come out of gross pay before you see it. Build the budget on take-home pay and note that pre-tax contributions already count toward savings goals.

Forgetting annual expenses: A $600 annual car insurance payment becomes a crisis if not planned for. Divide all annual or semi-annual expenses by the number of months and include them as sinking fund contributions.

Making the budget too optimistic: Allocating $200 per month for groceries when your actual average is $400 creates guaranteed failure. Base the budget on real spending from the past three months, then aim to reduce specific categories intentionally.

The USDA's food plan cost reports (updated monthly) provide useful reality checks for grocery budgets by household size.

Not including "fun money": Budgets with zero discretionary allocation fail because they are unsustainable. Even during aggressive debt paydown, allocating a small but explicit amount for guilt-free spending reduces the psychological deprivation that causes people to abandon budgets entirely.

Dave Ramsey calls this "blow money" - money you can spend on anything without guilt, because it was planned for.

Ignoring the partner gap: For couples, misaligned budgets are a leading source of financial conflict. Research by Britt and Huston (2012) in the Journal of Financial Therapy found that financial disagreements were the strongest predictor of divorce, stronger than disagreements about household tasks, sex, or in-laws.

Building a budget together, with explicit "personal spending" allocations for each partner, reduces this friction.

Budgeting Tools

| Tool | Method | Best For | Cost |

|---|---|---|---|

| YNAB (You Need A Budget) | Zero-based | Committed budgeters, debt paydown | $14.99/mo or $99/yr |

| Copilot | Automatic tracking | Mac/iOS users wanting AI categorization | $9.99/mo or $79.99/yr |

| Goodbudget | Envelope | Envelope method users, couples | Free (basic) or $10/mo |

| Monarch Money | Flexible | Households with investment accounts | $9.99/mo or $99.99/yr |

| Spreadsheet (manual) | Any method | People who want full customization | Free |

| Pen and paper | Any method | Behavioral research suggests physical tracking increases engagement | Free |

What Research Says Actually Changes Spending Behavior

A 2018 review by Fernbach and Kan in the Journal of Consumer Psychology synthesized findings from 60 studies on personal finance interventions. The interventions with the strongest evidence were:

- Automation of savings - reduces reliance on willpower, highest impact per unit of effort. Effect size: automatic enrollment increases retirement savings participation from approximately 40% to 90% (Madrian and Shea, 2001, Quarterly Journal of Economics).

- Mental accounting and goal labeling - naming a savings account "emergency fund" or "house deposit" increases contributions versus a generic "savings" label. Research by Soman and Cheema (2011) found that labeled accounts received 31% higher contributions.

- Implementation intentions - specifying exactly when, where, and how you will perform a financial behavior dramatically increases follow-through versus general goals. Peter Gollwitzer's research (1999) found implementation intentions roughly doubled goal achievement rates across domains.

- Social accountability - sharing goals with a partner, friend, or financial advisor increases adherence. A Dominican University study by Matthews (2015) found that people who wrote down goals and shared weekly progress with a friend achieved 76% of their goals, versus 43% for those who merely thought about goals.

- Regular review - scheduled monthly budget reviews outperform ad-hoc reviews. Consistency of review matters more than depth.

What the research does not support: financial education alone (Fernandes, Lynch, and Netemeyer, 2014, found that financial literacy interventions explained only 0.1% of variance in financial behavior), willpower-based approaches, and highly complex systems that require sustained effort to maintain.

The Behavioral Insight That Changes Everything

Perhaps the most counterintuitive finding in behavioral personal finance is that restrictions feel less restrictive when they are self-imposed and explicit. A person who deliberately allocates $150 for dining out and spends $148 feels satisfaction.

A person with no dining budget who spends $148 feels vague guilt. The number is identical; the psychological experience is entirely different.

This phenomenon, studied by Kivetz and Simonson (2002) in the Journal of Marketing Research, is related to the concept of precommitment - the Odysseus strategy of binding yourself to a future course of action before the temptation arises. Odysseus had his crew tie him to the mast before passing the Sirens.

A budget is a financial mast. The constraint is the freedom. Understanding how the mind actually works in these situations - where structure creates autonomy rather than limiting it - is the key insight that separates effective budgeting from doomed willpower exercises.

This is why budgeting, at its core, is not about cutting spending. It is about making spending choices consciously rather than by default - and discovering that conscious choices often align much better with what you actually value.

Getting Started: A Minimal First Budget

If all of this feels overwhelming, start here:

- Calculate last month's take-home pay.

- Look at your bank and credit card statements and add up total spending.

- Subtract spending from income. If it is negative (you spent more than you earned), you need a budget urgently. If it is positive, identify where the surplus went - if you cannot find it, you have a tracking gap.

- Pick one category where you overspent and set a specific monthly limit for it.

- Automate a fixed savings transfer, even $25, to a separate account on payday.

That is a budget. Not a sophisticated one, but a real one. Build on it as the habit forms.

The goal is not a perfect budget in month one. The goal is a functioning system that you will still be using in month twelve. As with exponential growth, the power is in the compounding: small, consistent financial improvements accumulate into transformative results over time.

Sources & Further Reading

- Thaler, R. H., & Benartzi, S. (2004). Save More Tomorrow: Using behavioral economics to increase employee saving. Journal of Political Economy, 112(S1), S164-S187.

- Warren, E., & Tyagi, A. W. (2005). All Your Worth: The Ultimate Lifetime Money Plan. Free Press.

- Prelec, D., & Simester, D. (2001). Always leave home without it: A further investigation of the credit-card effect on willingness to pay. Marketing Science, 20(1), 5-12.

- Ramsey, D. (2003). The Total Money Makeover. Thomas Nelson.

- Sethi, R. (2019). I Will Teach You to Be Rich. 2nd ed. Workman Publishing.

- Fernandes, D., Lynch, J. G., & Netemeyer, R. G. (2014). Financial literacy, financial education, and downstream financial behaviors. Management Science, 60(8), 1861-1883.

- Chetty, R., Friedman, J. N., Leth-Petersen, S., Nielsen, T. H., & Olsen, T. (2014). Active vs. passive decisions and crowd-out in retirement savings accounts. Quarterly Journal of Economics, 129(3), 1141-1219.

- McClure, S. M., Laibson, D. I., Loewenstein, G., & Cohen, J. D. (2004). Separate neural systems value immediate and delayed monetary rewards. Science, 306(5695), 503-507.

- Madrian, B. C., & Shea, D. F. (2001). The power of suggestion: Inertia in 401(k) participation and savings behavior. Quarterly Journal of Economics, 116(4), 1149-1187.

- Richards, C. (2012). The Behavior Gap: Simple Ways to Stop Doing Dumb Things with Money. Portfolio/Penguin.

- Thaler, R. H., & Sunstein, C. R. (2008). Nudge: Improving Decisions About Health, Wealth, and Happiness. Yale University Press.

- Federal Reserve Board. (2023). Survey of Household Economics and Decisionmaking (SHED). View source

- National Low Income Housing Coalition. (2023). Out of Reach: The High Cost of Housing. View source

- Bureau of Labor Statistics. (2023). Consumer Expenditure Survey. View source

Frequently Asked Questions

What is the best budgeting method for most people?

No single method is universally best, because the best budget is the one you will actually maintain. Research on financial behavior consistently shows that adherence matters far more than precision. The 50/30/20 rule works well for people who want a simple framework without tracking every transaction. Zero-based budgeting suits people who want total control over every dollar. The envelope method works particularly well for those who overspend on specific discretionary categories. Most financial planners recommend starting with whichever method creates the least friction, then adding detail as the habit solidifies.

What is the 50/30/20 budgeting rule?

The 50/30/20 rule divides after-tax income into three broad categories: 50 percent for needs (housing, utilities, groceries, insurance, minimum debt payments), 30 percent for wants (dining out, entertainment, travel, subscriptions), and 20 percent for savings and debt repayment beyond minimums. The framework was popularized by Senator Elizabeth Warren and her daughter Amelia Warren Tyagi in their 2005 book ‘All Your Worth.’ Its main virtue is that it requires only category-level awareness, not transaction-by-transaction tracking. In high cost-of-living cities where housing alone can consume 40 to 50 percent of income, the ratios serve better as long-term targets than rigid current constraints.

What is zero-based budgeting?

Zero-based budgeting (ZBB) is a method in which every dollar of income is assigned a specific purpose before the month begins, so that income minus all allocations equals zero. This does not mean spending everything: savings, investments, and debt paydown each receive explicit dollar amounts rather than being treated as whatever is left over. The method was adapted for personal use from corporate accounting practices and forms the philosophical backbone of the YNAB (You Need A Budget) app. Research on ZBB users shows higher savings rates and lower debt compared to users of other budgeting approaches, largely because it forces a conscious decision about every dollar.

What is the envelope budgeting method?

The envelope method involves dividing cash into physical envelopes labeled for each spending category (groceries, dining, entertainment, clothing, etc.). When an envelope is empty, spending in that category stops for the month. The system exploits a well-documented behavioral phenomenon: people spend less with physical cash than with cards because the ‘pain of paying’ is more salient when handing over bills. Popularized by Dave Ramsey, the envelope method is especially effective for people who consistently overspend in a few specific categories. Digital equivalents exist through apps like Goodbudget, which replicate the envelope logic without requiring physical cash.

Why do most budgets fail?

Behavioral research identifies several consistent failure modes. Present bias causes people to prioritize immediate spending over future savings even when they consciously value saving. Optimism bias leads to underestimating irregular expenses like car repairs, medical costs, and home maintenance, which are predictably unpredictable. Budgets built around average months fail when a non-average month arrives. A third failure mode is tracking fatigue: overly granular budgets require sustained effort that most people cannot maintain. The highest-evidence solution to all three is automation, directing savings before discretionary spending is accessible, which bypasses willpower entirely and removes the cognitive burden of repeated decisions.