Central banking explained centers on a public institution that issues currency, conducts monetary policy, serves commercial banks and government, and supplies emergency liquidity during financial panics. Its tools include policy interest rates, open-market operations, quantitative easing, forward guidance, and inflation targets.

These actions influence borrowing, lending, demand, and inflation through a transmission mechanism, while lender-of-last-resort decisions try to prevent illiquidity from becoming wider insolvency.

On the morning of September 15, 2008, Ben Bernanke woke up to learn that Lehman Brothers had filed for bankruptcy - the largest in American history. Bernanke was not primarily a central banker by temperament; he was an economist whose academic career had been built around a single question: why did the Great Depression last so long?[2]

His 1983 paper in the American Economic Review, "Nonmonetary Effects of the Financial Crisis in the Propagation of the Great Depression," had argued that the catastrophe of the 1930s was not just a story of falling demand but of the destruction of credit intermediation - the collapse of the banking system's ability to connect savers with borrowers - and that the Federal Reserve's failure to act as lender of last resort between 1930 and 1933 had turned a severe recession into a decade-long catastrophe.

He had spent his career studying this failure so that it would not be repeated.[8]

Now, on a Monday morning in September 2008, he was on the phone before sunrise. Within hours of Lehman's bankruptcy filing, the effects were cascading: the TED spread - the gap between the interest rate banks charged each other and the rate on US Treasury bills, a measure of financial system stress - spiked to levels not seen since the 1930s.

The Reserve Primary Fund, one of the largest money market funds in the United States, announced that its net asset value had fallen below one dollar per share, breaking the cardinal rule of money market funds.

Within days, a run on money market funds industry-wide was threatening the commercial paper market through which hundreds of American corporations financed their daily operations, including payroll.

What followed was the most consequential exercise of central bank power in the institution's modern history.

Within weeks, the Federal Reserve had created lending facilities with no historical precedent, deployed trillions of dollars in emergency liquidity, effectively nationalized the insurance giant AIG, and extended dollar swap lines to 14 foreign central banks.

It was Bagehot's doctrine in extremis: lend freely, at penalty rates, to stop the panic from destroying solvent institutions along with insolvent ones.

Almost nobody outside the Fed's offices on Constitution Avenue in Washington and the 12th floor of the New York Fed knew this was happening in real time. Central banking is perhaps the most consequential area of economic policy about which the public knows the least. That gap has costs.

"In the modern world, the central bank is the only institution that can create money without limit and deploy it at speed. That power - the power to be the lender of last resort - is what stands between financial panic and economic catastrophe.

Using it requires judgment about when the system is truly at risk and when letting institutions fail is necessary discipline." - Ben Bernanke, The Courage to Act (2015)

Key Definitions

Central bank: a public institution that issues a country's currency, manages monetary policy, acts as banker to commercial banks and the government, and in most cases serves as lender of last resort during financial crises.

Monetary policy: the set of actions a central bank takes to influence the money supply and interest rates in order to achieve macroeconomic objectives - typically price stability (low inflation) and, in the Federal Reserve's case explicitly, maximum employment.

Federal funds rate: the rate at which commercial banks lend their excess reserves to each other overnight.[11] The Federal Reserve sets a target for this rate as its primary monetary policy instrument; changes propagate through the financial system to affect all borrowing and lending costs.

Open market operations: the Fed's purchase and sale of government securities in the open market to adjust the supply of bank reserves and influence the federal funds rate.

Quantitative easing (QE): a policy in which a central bank creates new money to purchase long-term assets (government bonds, mortgage-backed securities) to lower long-term interest rates when the short-term policy rate is already at or near zero - the zero lower bound.

Lender of last resort: the function of providing emergency liquidity to solvent financial institutions during panics, preventing illiquidity from becoming insolvency. Articulated by Walter Bagehot in 1873: lend freely at penalty rates against good collateral.

Zero lower bound (ZLB): the constraint that nominal interest rates cannot easily go below zero, limiting conventional monetary policy when the economy requires additional stimulus.

Inflation targeting: a monetary policy framework in which the central bank announces an explicit inflation target (typically 2 percent) and adjusts policy instruments to achieve it.

Dual mandate: the Federal Reserve's statutory requirement to pursue both price stability and maximum employment - a mandate that creates potential trade-offs that most other central banks, which target only inflation, do not formally face.

Transmission mechanism: the chain of channels through which changes in monetary policy interest rates affect the broader economy and, ultimately, inflation.

Forward guidance: central bank communication about the future path of monetary policy, which can itself shape interest rate expectations and financial conditions without changing current rates.

Time inconsistency: the tendency of discretionary policymakers to make commitments they will later have incentives to break - identified by Finn Kydland and Edward Prescott as the core problem that justifies rules-based over discretionary monetary policy.

Major Central Bank Tools Compared

| Tool | How it works | Primary objective | Limitations | Used most in |

|---|---|---|---|---|

| Policy interest rate (e.g., federal funds rate) | Sets overnight interbank lending rate; propagates to mortgages, business loans, consumer credit | Control inflation; stimulate or cool aggregate demand | Works slowly (12-18 month lag); ineffective at zero lower bound | Normal economic cycles |

| Open market operations | Buys or sells short-term government securities to adjust bank reserves and enforce rate target | Implement interest rate target | Effectiveness depends on reserve demand; limited when rates near zero | Routine policy implementation |

| Reserve requirements | Sets fraction of deposits banks must hold in reserve, not lend | Limit credit expansion; ensure liquidity | Rarely used as active tool in modern central banking; blunt instrument | Historical; de-emphasized post-2008 |

| Quantitative easing (QE) | Creates new money to buy long-term bonds and MBS; lowers long-term yields | Stimulate when short-term rate at zero lower bound | Diminishing returns; enriches asset holders; financial stability risks | Zero lower bound episodes (2008-2021) |

| Forward guidance | Communicates future policy intentions to shape market expectations | Lower long-term rates without asset purchases | Credibility-dependent; markets may not believe announcements | Complement to QE; zero lower bound |

| Lender of last resort | Emergency loans to solvent institutions during panics, at penalty rates against good collateral | Stop bank runs and financial contagion | Cannot rescue insolvent institutions; moral hazard risk | Financial crises (1907, 2008) |

| Dollar swap lines | Provides foreign central banks US dollars against their currency | Prevent dollar shortage from freezing global dollar-denominated funding markets | Requires bilateral agreements; political sensitivity | 2008, COVID-19 (2020) |

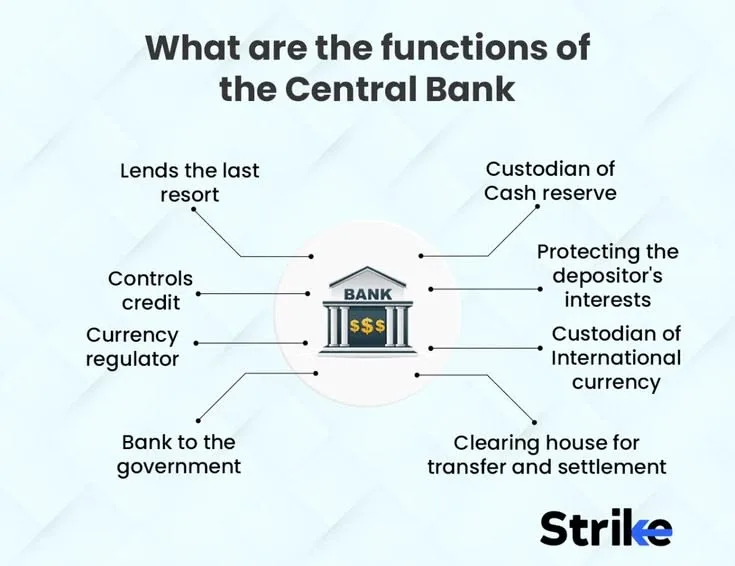

Four Functions of a Central Bank

The central bank is perhaps the most unusual institution in modern government: it has the power to create money from nothing, it operates with substantial independence from elected politicians, and its decisions set the cost of credit throughout the economy.

Understanding what it actually does requires separating its several distinct functions.

The oldest function is the monopoly on currency issuance. Before central banking, private banks issued their own notes - promises to pay in gold or silver. When banks failed, their notes became worthless. The proliferation of private currencies created confusion, fraud, and recurring crises.

Central banks consolidated currency issuance, creating a uniform national currency. The Bank of England, founded in 1694 (the Swedish Riksbank, 1668, is the world's oldest), was created partly to finance government debt and partly to provide a reliable currency.

Today, the Federal Reserve issues US dollars; the European Central Bank issues euros; both are legal tender that creditors must accept in settlement of debts.

The second function is banking for banks. Commercial banks maintain reserve accounts at the central bank. When you transfer money from your bank to a friend's bank, the settlement ultimately occurs through corresponding adjustments in each bank's reserve account at the Fed.

The central bank operates the payments infrastructure - the plumbing - of the financial system. It also holds government accounts, clearing taxes received and payments made.

The third and most visible function is monetary policy. The Federal Reserve sets the federal funds rate - the overnight rate at which banks lend reserves to each other - as its primary instrument.

Changes in the federal funds rate propagate through the financial system to mortgage rates, corporate bond yields, auto loan rates, and consumer credit costs, affecting aggregate demand across the economy.

The Fed's Federal Open Market Committee holds eight scheduled meetings per year to vote on the funds rate target and communicates extensively about its expectations for future policy.

The fourth function is the lender of last resort. Walter Bagehot's 1873 "Lombard Street: A Description of the Money Market" remains the canonical text.[1] Bagehot's insight was simple and profound: financial panics spread through contagion.

When depositors fear a bank will fail, they run to withdraw their funds. Their withdrawal makes failure more likely. The run spreads to other banks even if those banks are sound, because depositors cannot distinguish sound from unsound institutions in a panic.

The lender of last resort stops the contagion by lending freely to any solvent institution that needs liquidity - at penalty rates, to deter unnecessary borrowing, and against good collateral, to ensure the borrowing institution is genuinely solvent rather than insolvent.

The mere credible existence of a lender of last resort can prevent panics from starting.

The United States created the Federal Reserve in 1913 specifically because it had experienced severe banking panics in 1873, 1893, 1896, and 1907. The 1907 Panic, which was resolved only through the personal intervention of J.P.

Morgan - who organized a private banking consortium to stop the runs while the US government stood helplessly by - made clear that the world's largest economy could not continue to depend on the charity of private financiers.

How Monetary Policy Works

The mechanism by which interest rate changes affect inflation is called the transmission mechanism, and it involves several channels operating simultaneously over different time horizons.

When the Federal Reserve raises the federal funds rate, commercial banks' cost of borrowing reserves increases. They pass this cost through by raising the rates they charge on mortgages, auto loans, business loans, and credit cards.

Higher mortgage rates reduce housing affordability, lowering demand for homes and the construction activity that serves it. Higher business loan rates raise the hurdle rate for investment projects, reducing capital expenditure.

Higher consumer credit rates reduce spending on durable goods financed with credit. Simultaneously, higher rates strengthen the dollar as dollar-denominated assets become more attractive to foreign investors, making imports cheaper and exports less competitive - exerting additional downward pressure on domestic prices.

Through all these channels, higher interest rates reduce aggregate demand: the total spending on goods and services in the economy. With less spending chasing the same goods and services, sellers have less pricing power, wage demands moderate as labor markets loosen, and the pace of price increases decelerates.

This mechanism works, but it works slowly. The standard estimate in monetary economics is that monetary policy changes take roughly 12 to 18 months to have their full effect on inflation.

This lag creates a fundamental challenge for central bankers: they must set policy today for economic conditions that will prevail 12 to 18 months from now - conditions they can forecast only imperfectly.

Tighten too little, and inflation becomes entrenched in expectations. Tighten too much, and a recession results from policy that was calibrated to a problem that has already resolved itself.

The 1970s illustrated the danger of insufficient tightening. A combination of oil shocks from the 1973 OPEC embargo and the 1979 Iranian Revolution, expansionary fiscal policy to finance the Vietnam War and Great Society programs, and a Fed unwilling to accept the unemployment that fighting inflation required produced the highest sustained inflation in US postwar history - exceeding 13% by 1980.

Federal Reserve chairman Paul Volcker, appointed by President Carter in 1979, applied the cure: he raised the federal funds rate to nearly 20% in 1981.[9]

The result was the deepest recession since the Great Depression - unemployment reached 10.8% in late 1982. Inflation came down durably, establishing the principle that central bank credibility on inflation is worth paying for even at significant short-term economic cost.

The Case for Independence: Time Inconsistency

The political case for central bank independence rests on a theoretical foundation provided by economists Finn Kydland and Edward Prescott in a 1977 paper in the Journal of Political Economy titled "Rules Rather Than Discretion: The Inconsistency of Optimal Plans" - work for which they were awarded the Nobel Prize in Economics in 2004.

Kydland and Prescott identified what they called the time inconsistency problem in monetary policy.[4] Democratic politicians have systematic incentives to stimulate the economy before elections: lower interest rates mean lower unemployment and stronger growth in the short run, even if the consequence is higher inflation in the medium run.

A central bank subject to electoral pressure will therefore tend to produce more inflation than is optimal, because it cannot credibly commit to low inflation when those commitments will later be tempting to break.

Workers and firms, knowing this, will set wages and prices anticipating higher inflation, creating a self-fulfilling inflation bias.

The solution Kydland and Prescott identified is institutional commitment: a central bank operating under rules rather than discretion, or insulated from political pressure by legal independence, can credibly commit to keeping inflation low.

That credibility is self-reinforcing: if workers and firms believe the central bank will maintain 2% inflation, they will negotiate wages and set prices accordingly, making 2% inflation easier to achieve without sacrificing employment.

Cross-country empirical studies in the late 1980s and 1990s found that countries with more legally independent central banks - measured by the degree to which the central bank charter insulated the institution from executive instruction - produced lower average inflation, though the causal interpretation was disputed.

More independent central banks and lower inflation may both reflect underlying institutional quality rather than independence causing lower inflation.

But the logic of time inconsistency remains the strongest economic case for insulating monetary policy from day-to-day democratic control.

The 2008 Crisis: Lehman and After

The 2008 financial crisis was substantially the product of deregulation. The Gramm-Leach-Bliley Act of 1999 repealed Glass-Steagall provisions separating commercial and investment banking.

The Commodity Futures Modernization Act of 2000 excluded over-the-counter derivatives - including the credit default swaps that would prove fatal - from regulatory oversight.

Under Basel II capital rules, banks held complex mortgage securities with minimal capital buffers on the theory that diversification made them low-risk.

By 2006 the US housing market had produced a massive bubble of mortgages sold to borrowers who could not afford them, securitized into instruments whose risks were obscured by complexity, and sold to investors worldwide at every step with minimal retention of risk.[10]

When Bear Stearns approached collapse in March 2008, the Fed arranged an emergency merger with JPMorgan, providing a $29 billion loan. This established the precedent that the Fed would rescue systemically important institutions.

When Lehman Brothers faced the same fate six months later, Paulson and Bernanke concluded that the Fed lacked sufficient legal authority to rescue it and that creditors needed to absorb losses to restore market discipline.[3]

The decision remains contested. Within days of Lehman's September 15 bankruptcy, the commercial paper market had frozen, the TED spread had spiked to levels not seen since the 1930s, and AIG - whose $440 billion in credit default swaps threaded obligations through virtually every major financial institution - was next.

The Fed's response was sweeping: the Commercial Paper Funding Facility, dollar swap lines to 14 foreign central banks, and an $85 billion emergency loan to AIG - effectively a government takeover. The Fed's balance sheet rose from approximately $900 billion to $2.3 trillion by early 2009.

Congress passed the $700 billion TARP in October 2008. The public reaction was politically transformative: billions of public dollars rescued the institutions whose recklessness had caused the crisis, while homeowners who had lost their houses received no comparable relief.

This asymmetry generated a decade of populist anger on both right and left.

Quantitative Easing: The Unconventional Tool

By late 2008, the Fed had cut the federal funds rate to its zero lower bound - effectively 0 to 0.25 percent. But the economy remained in deep recession. Conventional monetary policy had run out of room. The Fed needed a new tool.

The solution was quantitative easing: creating new money and using it to purchase long-term assets.

By buying Treasury bonds and mortgage-backed securities in large quantities, the Fed would drive up their prices and drive down their yields, transmitting monetary stimulus through the long-term interest rates that govern mortgages and corporate borrowing when short-term rates could go no lower.

The Fed's first QE program (QE1) ran from late 2008 through March 2010, purchasing $1.75 trillion in assets and expanding the Fed's balance sheet to $2.1 trillion. QE2 (November 2010 to June 2011) and QE3 (September 2012 to October 2014) extended the balance sheet to approximately $4.5 trillion.

The European Central Bank, Bank of Japan, and Bank of England implemented comparable programs; the Bank of Japan's was the most extreme, at times owning more than half of the outstanding Japanese government bond market.

The evidence on QE's effectiveness is positive but bounded. Joseph Gagnon and colleagues, in a 2011 study published in the International Journal of Central Banking titled "Large-Scale Asset Purchases by the Federal Reserve: Did They Work?", estimated that QE1 reduced 10-year Treasury yields by between 50 and 100 basis points - a meaningful reduction that plausibly supported the housing market recovery and refinancing activity.[5]

Studies of subsequent rounds found smaller effects, consistent with diminishing returns.

Mario Draghi's July 2012 announcement that the ECB would do "whatever it takes" to preserve the euro - backed by a new QE-style facility - stabilized euro-area sovereign debt markets at a moment of existential crisis for the eurozone, with apparently large effects from the commitment alone before significant asset purchases began.

The distributional critique of QE has grown as its scale has expanded. By raising the prices of stocks, bonds, and real estate, QE transferred wealth to those who hold these assets - who are disproportionately wealthy.

Federal Reserve governor Jeremy Stein, in a 2013 speech that attracted significant attention from academic economists, argued that QE also encouraged excessive risk-taking by financial institutions searching for yield in a low-rate environment, creating financial stability risks that were difficult to measure but potentially large.[6]

Whether QE's economic benefits - supporting aggregate demand and preventing deflation - were worth its distributional costs and financial stability risks remains a genuinely contested question, and one with significant political implications given that it is the wealthiest households that benefited most.

The 2021-2023 Inflation Surge

The COVID-19 pandemic produced the fastest and deepest economic contraction since the Great Depression. The Federal Reserve cut rates to zero in March 2020, restarted QE, and created emergency facilities drawing on 2008 institutional memory.

Its balance sheet grew from $4.5 trillion to approximately $9 trillion by 2022. Congress provided roughly $5 trillion in fiscal stimulus - direct payments to households, enhanced unemployment benefits, forgivable business loans, and state and local government support.

The combination produced the fastest postwar recovery - and, beginning in mid-2021, sharply rising inflation. Supply chains disrupted by pandemic closures and a shift in consumer demand from services to goods produced shortages of semiconductors, automobiles, and consumer electronics.

Energy prices spiked further after Russia's February 2022 invasion of Ukraine. The combination of supply constraint and demand stimulus drove inflation to 9.1% in June 2022 - the highest since 1981.

Fed chairman Jerome Powell, along with Treasury Secretary Janet Yellen and most private-sector forecasters, characterized the emerging inflation as "transitory" through much of 2021. The Fed did not begin raising rates until March 2022, when inflation was already above 7%.

Whether earlier action was warranted, or would have needlessly slowed an economy still recovering from its deepest peacetime shock, is a genuine empirical uncertainty.

Once tightening began, it was rapid: eleven rate increases in approximately 12 months brought the federal funds rate to 5.25-5.50% by July 2023 - the fastest sustained tightening cycle since Volcker. Inflation did decline substantially, reaching roughly 3% by mid-2023, and the feared deep recession did not materialize.

The relative contributions of monetary tightening versus supply chain normalization remain debated, but the outcome generated qualified descriptions of a "soft landing."

Central Bank Independence Under Pressure

Central bank independence is under political stress in multiple countries simultaneously. The economic case for independence - grounded in Kydland and Prescott's time inconsistency analysis - faces a political argument: that monetary policy has large distributional consequences that should not be made by unaccountable technocrats.

The distributional argument has empirical force. QE enriched asset holders. High interest rates impose costs disproportionately on mortgage holders and businesses with floating-rate debt.

The March 2023 failures of Silicon Valley Bank and Signature Bank were consequences of the 2022-2023 rate increases materializing as interest rate risk in long-dated bond portfolios.

These effects were not accidental byproducts of neutral policy; they were the mechanism of monetary transmission, with predictable winners and losers.

Critics including political economists Daniela Gabor and others have argued that distributional decisions of this magnitude should require democratic authorization, not just technocratic judgment.

Political pressure on central banks has taken direct forms. Donald Trump publicly and repeatedly criticized Federal Reserve Chair Jerome Powell throughout his first and second terms, calling for lower rates, questioning Powell's tenure, and reportedly exploring whether the Fed chair could be legally removed.

Turkish President Recep Erdogan's insistence that high interest rates cause inflation - the inverse of conventional economics - led him to fire or pressure out multiple central bank governors; the result was a Turkish lira crisis and inflation reaching 85% in 2022 before orthodox policy was reluctantly restored.

Hungary's government has taken steps to increase political influence over the Magyar Nemzeti Bank. These cases illustrate what the time inconsistency argument predicted: when politicians control monetary policy, inflation tends to follow.

Modern Monetary Theory (MMT), developed by economists Warren Mosler, Randall Wray, and popularized by Stephanie Kelton's 2020 book "The Deficit Myth," offers a heterodox framework that challenges several conventional premises.[7]

MMT's central descriptive claim is that a government which issues its own currency - like the United States issuing dollars, or the United Kingdom issuing pounds, but unlike Greece, which issues euros it does not control - cannot run out of money in the way a household or firm can.

The government creates money by spending it and destroys money by taxing it; the fiscal constraint on a currency-issuing government is not financing but inflation: whether the economy has the productive capacity to absorb additional spending without triggering price increases.

MMT's policy implication was that federal deficits per se are not a problem for a currency-issuing government; the real limit is inflation.

Paul Krugman, Lawrence Summers, and other mainstream economists argued that MMT underestimated how quickly inflation emerges from monetary financing of fiscal deficits and that the 2021-2022 inflation surge - occurring in the context of massive deficit-financed COVID stimulus and a Federal Reserve balance sheet that had grown to $9 trillion - was at least partially consistent with their concerns.

MMT proponents responded that the inflation was primarily supply-chain driven rather than monetary, noting that countries with similar stimulus programs but different supply exposures experienced different inflation levels.

The debate is, at bottom, a question about how close advanced economies are to their productive capacity limits and how precisely fiscal policy can be calibrated to avoid crossing them.

Connections

For the mechanics of how interest rates and money creation interact with inflation, see how inflation works. For a broader account of how financial markets allocate capital and create systemic risk, see how financial markets work.

For the dynamics of how recessions begin, deepen, and end, see how recessions happen.

Sources & Further Reading

- Bagehot, W. (1873). Lombard Street: A Description of the Money Market. Henry S. King.

- Bernanke, B. S. (1983). Nonmonetary effects of the financial crisis in the propagation of the Great Depression. American Economic Review, 73(3), 257-276.

- Bernanke, B. S. (2015). The Courage to Act: A Memoir of a Crisis and Its Aftermath. W.W. Norton.

- Kydland, F. E., & Prescott, E. C. (1977). Rules rather than discretion: The inconsistency of optimal plans. Journal of Political Economy, 85(3), 473-491. DOI: 10.1086/260580

- Gagnon, J., Raskin, M., Remache, J., & Sack, B. (2011). Large-scale asset purchases by the Federal Reserve: Did they work? International Journal of Central Banking, 7(1), 3-43.

- Stein, J. (2013). Overheating in credit markets: Origins, measurement, and policy responses. Speech at a research symposium sponsored by the Federal Reserve Bank of St. Louis, February 7, 2013.

- Kelton, S. (2020). The Deficit Myth: Modern Monetary Theory and the Birth of the People's Economy. PublicAffairs.

- Friedman, M., & Schwartz, A. J. (1963). A Monetary History of the United States, 1867-1960. Princeton University Press.

- Blinder, A. S. (2022). A Monetary and Fiscal History of the United States, 1961-2021. Princeton University Press.

- Gorton, G. (2010). Slapped by the Invisible Hand: The Panic of 2007. Oxford University Press.

- Federal Reserve Bank of St. Louis. FRED Economic Data.

Frequently Asked Questions

What does a central bank actually do?

A central bank has four primary functions, though not all central banks perform all four. First, it is the monopoly issuer of a country’s currency: the Federal Reserve issues US dollars; the European Central Bank issues euros. Central bank money is legal tender that must be accepted in settlement of debts. Second, it acts as banker to the government and to commercial banks: banks hold reserve accounts at the central bank, and the central bank clears payments between banks through this infrastructure. Third, it conducts monetary policy: it sets interest rates and controls the money supply to pursue macroeconomic objectives, typically price stability (low inflation) and, in the Federal Reserve’s case explicitly, maximum employment. Fourth, it acts as lender of last resort: when financial panics cause banks to face sudden withdrawals they cannot meet, the central bank lends to them to prevent contagion from turning illiquidity into insolvency. The lender of last resort function, articulated by Walter Bagehot in ‘Lombard Street’ in 1873, is perhaps the most important: Bagehot’s prescription was to lend freely at penalty rates against good collateral, stopping panics from spreading before they destroy solvent institutions. Many central banks also supervise banks, set capital requirements, and operate the payment system. The Federal Reserve was created in 1913 specifically because the United States had experienced severe banking panics roughly every decade in the 19th and early 20th centuries, panics that devastated the real economy, and financial leaders concluded that a central bank capable of acting as lender of last resort was essential.

How does raising interest rates reduce inflation?

The mechanism by which central banks use interest rates to control inflation is called the transmission mechanism, and it involves several interconnected channels that collectively slow economic activity when rates rise. The Federal Reserve’s primary tool is the federal funds rate, the rate at which banks lend reserves to each other overnight. When the Fed raises the federal funds rate, it becomes more expensive for banks to borrow reserves, which raises their own cost of funds. Banks respond by raising the interest rates they charge on loans to businesses and consumers. Higher mortgage rates make homes more expensive to finance, reducing housing demand and construction activity. Higher business loan rates make investment in new equipment and expansion more costly, reducing capital expenditure. Higher consumer credit rates reduce spending on durable goods financed with credit. All of these effects reduce aggregate demand, the total spending in the economy. With less spending chasing goods and services, sellers have less pricing power, wage demands moderate as labor markets loosen, and the pace of price increases slows. The mechanism works with significant time lags: most economists estimate 12 to 18 months for monetary policy to have its full effect on inflation. This lag creates a fundamental challenge: the Fed must make decisions based on forecasts of future inflation and employment, which are uncertain, and must be willing to raise rates before inflation clearly peaks, accepting the risk of raising too far or too fast. The 2022-2023 tightening cycle illustrated this vividly: the Fed raised rates from near zero to 5.25 percent in 18 months, the fastest tightening cycle since Paul Volcker in the early 1980s, and inflation did decline from its peak of over 9 percent, though the relative contributions of monetary tightening versus supply chain normalization remain debated.

What happened to the financial system in September 2008, and how did the Fed respond?

The collapse of Lehman Brothers on September 15, 2008, at the time the largest bankruptcy filing in US history, triggered the most acute financial panic since the Great Depression. Lehman was deeply enmeshed in the global financial system through complex derivative contracts, commercial paper borrowing, and securities lending. Its failure created immediate uncertainty about who was exposed to Lehman’s debts and how large those exposures were. Credit markets froze almost immediately: the interest rate spread on interbank lending (the TED spread) spiked to levels not seen since the 1930s. The Reserve Primary Fund, a money market fund with heavy exposure to Lehman’s commercial paper, ‘broke the buck’, its net asset value fell below one dollar per share, triggering a run on money market funds industry-wide and threatening the commercial paper market through which many corporations financed their day-to-day operations. The Federal Reserve’s response was unprecedented in scale and speed. Fed chairman Ben Bernanke, himself a scholar of the Great Depression who had argued that the Fed’s failure to act as lender of last resort in 1930-1933 turned a recession into a catastrophe, was determined not to repeat that error. The Fed created a series of emergency lending facilities that had no precedent: the Commercial Paper Funding Facility, the Money Market Investor Funding Facility, the Term Asset-Backed Securities Loan Facility. It extended swap lines to foreign central banks so they could provide dollar liquidity to their own financial systems. In coordination with the Treasury, it effectively nationalized AIG, the insurance giant whose credit default swap exposure threatened to detonate the entire financial system, with an \(85 billion loan. The Fed's balance sheet expanded from roughly \)900 billion before the crisis to over \(2 trillion within months. Congress passed the \)700 billion Troubled Asset Relief Program. The system did not collapse, but the question of whether the response was appropriate, and who bore the cost, shaped a decade of political conflict.

What is quantitative easing and does it actually work?

Quantitative easing (QE) is an unconventional monetary policy tool that central banks use when they have lowered their main policy interest rate to zero (or near zero) and need to provide additional stimulus. The conventional tool, cutting short-term interest rates, cannot be used further when rates are already at zero (the ‘zero lower bound’). QE involves the central bank creating new money and using it to buy long-term financial assets, typically government bonds and, in the Federal Reserve’s case, mortgage-backed securities. By purchasing these assets, the central bank drives up their price, which means their yield (interest rate) falls. Lower long-term interest rates stimulate borrowing and investment in ways that lower short-term rates cannot. The Fed’s first QE program (QE1) ran from late 2008 through 2010, expanding its balance sheet to roughly \(2 trillion. QE2 and QE3 followed in subsequent years, eventually growing the Fed's balance sheet to around \)4.5 trillion by 2015. The ECB, Bank of Japan, and Bank of England all implemented similar programs. Does it work? The evidence is mixed but generally positive for the limited goal of reducing long-term interest rates. A 2011 study by Joseph Gagnon and colleagues in the International Journal of Central Banking found that QE1 reduced 10-year Treasury yields by approximately 50-100 basis points, a meaningful effect. Other studies found that QE supported asset prices more broadly. The controversial aspect is distributional: QE inflated the prices of stocks, bonds, and real estate, which are predominantly owned by wealthier households. Critics, including former Fed governor Jeremy Stein, argued that QE also encouraged excessive risk-taking by financial institutions searching for yield. Whether QE’s economic benefits were worth these distributional and financial stability costs remains a contested question.

What caused the 2021-2023 inflation surge and how well did the Fed handle it?

The inflation surge of 2021-2023 was caused by an unusual combination of factors that converged in the aftermath of the COVID-19 pandemic. Supply chain disruptions, caused by factory closures, port congestion, and a shift in consumer demand from services to goods, created shortages of semiconductors, automobiles, and consumer electronics that drove their prices sharply higher. The energy price shock triggered by Russia’s February 2022 invasion of Ukraine added to inflation globally. Simultaneously, the economy was being supported by massive fiscal stimulus: the US government had injected approximately $5 trillion in COVID relief spending, including direct payments to households, enhanced unemployment benefits, and business loans. The Federal Reserve had kept its policy rate near zero and was still expanding its balance sheet through QE as late as February 2022. This combination of supply-side disruptions and demand-side stimulus produced inflation that peaked at 9.1 percent in June 2022, the highest since 1981. The Fed’s record on this episode is contested. Fed officials, along with Treasury Secretary Janet Yellen and many private-sector economists, characterized the inflation as ‘transitory’ through 2021, a temporary spike driven by supply disruptions that would resolve itself. The Fed did not begin raising rates until March 2022, by which point inflation was already well above its 2 percent target. Whether earlier action would have been warranted, or whether it would have needlessly slowed an economy still recovering from the pandemic, is genuinely uncertain. Once the Fed began tightening, it moved quickly: 11 rate increases in 12 months brought the federal funds rate from near zero to 5.25-5.50 percent by mid-2023. Inflation did come down significantly, and the feared deep recession did not materialize, leading many economists to describe the outcome as a ‘soft landing.’

What is the debate about central bank independence?

Central bank independence, the principle that monetary policy decisions should be made by technocratic experts insulated from day-to-day political pressure, is both economically influential and politically contested. The economic case for independence rests on the ‘time inconsistency’ problem, formalized by economists Finn Kydland and Edward Prescott in a 1977 paper that won them the Nobel Prize. Democratic politicians have an incentive to stimulate the economy before elections (lowering unemployment and boosting growth in the short term) even if this produces higher inflation in the medium term. A central bank insulated from political pressure can credibly commit to keeping inflation low, and this credibility itself reduces inflation: if workers and firms believe the central bank will keep inflation at 2 percent, they will set wages and prices accordingly, making 2 percent easier to achieve. Cross-country empirical studies through the 1980s and 1990s found that more independent central banks produced lower average inflation without sacrificing output. Against independence, critics argue that monetary policy has significant distributional consequences, QE inflated asset prices, benefiting the wealthy; high interest rates disproportionately harm borrowers, and that decisions with large distributional effects should be made by accountable democratic institutions, not technocratic ones. Political pressure on central banks has intensified recently. Donald Trump publicly criticized Federal Reserve Chair Jerome Powell repeatedly, calling for lower rates, and reportedly explored firing him. Turkish President Recep Erdogan fired multiple central bank governors when they raised rates against his wishes, with inflationary consequences. India and Hungary have taken steps to increase political influence over their central banks. Whether central bank independence is a durable institutional arrangement or a postwar liberal consensus that is eroding under populist pressure is an open question.

What is Modern Monetary Theory and is it correct?

Modern Monetary Theory (MMT) is a heterodox macroeconomic framework associated with economists Warren Mosler, Randall Wray, Stephanie Kelton (whose 2020 book ‘The Deficit Myth’ brought the ideas to wide attention), and others. MMT’s central claim is that a government that issues its own currency, like the United States, which issues dollars, or the United Kingdom, which issues pounds, but unlike Greece, which issues euros it does not control, can never run out of money in the way a household or firm can. The government creates money by spending it and destroys money by taxing it. The fiscal constraint on a currency-issuing government is not the ability to finance spending (it can always create money) but inflation: the real constraint is whether the economy has the productive capacity to absorb additional spending without price increases. In this framework, the purpose of taxation is not primarily to raise revenue to fund spending but to manage aggregate demand and prevent inflation. The policy implication that attracted both the most attention and the most controversy was: the federal government should spend until it reaches the inflation constraint, and deficits per se are not a problem for a currency-issuing government. MMT’s descriptive claims about how government money creation works are largely accepted by mainstream economists as technically accurate. Its policy prescriptions are more controversial. Critics, including Paul Krugman and Lawrence Summers, argued that MMT underestimates how quickly inflation emerges when monetary financing of fiscal deficits increases money supply growth, and that the 2021-2022 inflation surge was at least partially consistent with these concerns. MMT proponents respond that the inflation was supply-side driven rather than demand-driven. The debate about MMT is, at bottom, a debate about how close advanced economies are to their real productive capacity constraints and about the political feasibility of using fiscal policy with sufficient precision and speed to prevent inflation.