Everyone knows the story: the stock market crashed on Black Tuesday, October 29, 1929, and the Great Depression followed. Ticker tape machines ran hot across Wall Street. Speculators who had borrowed to buy on margin watched their positions wiped out in hours.

The papers ran photographs of men in suits selling apples on street corners. It is one of the most iconic cause-and-effect stories in modern history.

But the story is wrong - or at least, it is radically incomplete. The stock market crash did not cause the Great Depression. The American economy had survived stock market panics before, including the severe financial crisis of 1907, without anything approaching a decade-long catastrophe.

What happened between 1929 and 1933 was something different: a series of policy failures so consequential that they transformed a severe recession into a structural collapse.[7]

To understand the Depression properly, the historian must look not to October 1929, but to 1931 - the year the banking panics reached their peak, the year the Federal Reserve raised interest rates to defend the gold standard while banks failed across the country, and the year that Milton Friedman and Anna Schwartz would later identify as the moment when bad policy turned a crisis into a catastrophe.

Their 1963 work, A Monetary History of the United States, stands as one of the most influential and controversial arguments in the history of economics: the Federal Reserve did not merely fail to prevent the Great Depression. It caused the worst of it.

"You're right, we did it. We're very sorry. But thanks to you, we won't do it again." - Ben Bernanke, Remarks at Milton Friedman's 90th Birthday Conference (2002), acknowledging the Federal Reserve's responsibility for the severity of the Depression

| Cause | Type | Impact |

|---|---|---|

| Stock market crash (1929) | Financial shock | Wiped out investor wealth, froze credit |

| Bank failures (1930-1933) | Financial contagion | 9,000+ banks failed; savings destroyed |

| Smoot-Hawley Tariff (1930) | Policy error | Triggered retaliatory trade barriers globally |

| Tight monetary policy | Policy error | Federal Reserve contracted money supply by one-third |

| Agricultural collapse | Structural | Deflation, farm foreclosures, rural poverty |

| Consumer debt overextension | Structural | Demand collapsed as credit dried up |

| International gold standard | Systemic | Transmitted deflation across borders |

| Hoover's fiscal tightening (1932) | Policy error | Tax increase mid-recession deepened contraction |

Key Definitions

Depression: A severe and prolonged contraction of economic activity, typically defined by GDP falling more than 10 percent and unemployment exceeding 20 percent for multiple years. Distinguished from a recession, which is shorter and less severe.

Deflation: A general decline in the price level. While it sounds beneficial, sustained deflation is economically destructive: it encourages consumers to delay purchases (prices will be lower tomorrow), increases the real burden of debt, and causes business failures and unemployment.

Money supply: The total stock of money circulating in an economy, including currency and bank deposits. When banks fail and deposits are wiped out, the money supply contracts - there is literally less money available for transactions.

Lender of last resort: The role of a central bank in providing emergency liquidity to solvent banks facing temporary bank runs, preventing sound banks from being destroyed by panic.

Gold standard: A monetary system in which currency is convertible into a fixed quantity of gold. Countries on the gold standard cannot expand their money supply freely; they are constrained by their gold reserves.

Multiplier effect: The Keynesian concept that government spending generates more than a one-for-one increase in economic activity, as each dollar spent becomes income for someone who then spends a portion of it.

Paradox of thrift: John Maynard Keynes's observation that while individual saving is prudent, when everyone saves simultaneously during a downturn, aggregate demand collapses and the economy contracts, making everyone worse off.

Debt deflation: Irving Fisher's (1933) concept describing a self-reinforcing spiral in which falling prices increase the real burden of debt, causing defaults, further asset sales, further price declines, and further defaults - a mechanism he believed was central to the Depression's severity.[5]

The Scale of the Catastrophe

Before examining causes, it is worth establishing what actually happened - the raw scale of the economic disaster that the Great Depression represented.

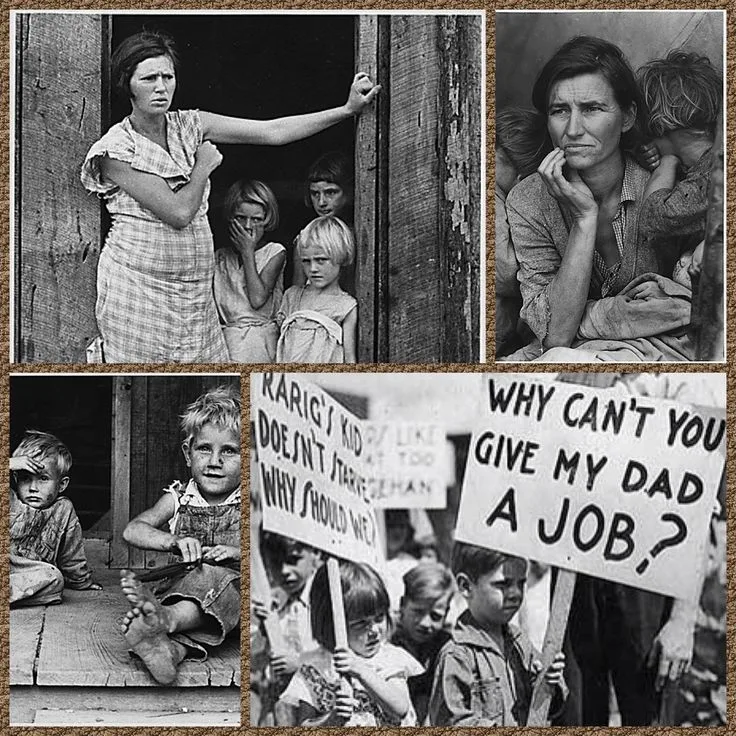

Between 1929 and 1933, US gross domestic product fell by approximately 30 percent in real terms. Industrial production fell by nearly half. The unemployment rate rose from approximately 3 percent in 1929 to nearly 25 percent in 1933 - meaning one in four American workers could not find a job.

At the Depression's trough, approximately 15 million Americans were unemployed. Farm income fell by more than 50 percent. Residential construction collapsed by 80 percent.

Over 9,000 banks failed, wiping out the savings of millions of ordinary depositors who had done nothing wrong.

The human suffering behind these statistics was immense: breadlines in American cities stretching for blocks; families losing farms held for generations; the migration of the Dust Bowl's "Okies" immortalized by John Steinbeck in The Grapes of Wrath (1939).[12]

The Depression was not merely an American event. It spread globally through trade, capital flows, and the gold standard mechanism. In Germany, unemployment reached approximately 30 percent by 1932. In France, industrial production fell by 25 percent.

The global trading system, already weakened by wartime disruption and post-war protectionism, collapsed. World trade volumes fell by roughly 66 percent between 1929 and 1932.

The Initial Shock: What the Crash Did and Did Not Do

The stock market boom of the 1920s was built on speculation and leverage. Stock prices had risen dramatically - the Dow Jones Industrial Average increased more than tenfold between 1920 and 1929 - but much of this rise was fueled by margin buying, with investors borrowing as much as 90 percent of the purchase price.

When prices began falling in late October 1929, margin calls forced liquidation, which drove prices lower still, which triggered more margin calls. By November 1929, the market had lost nearly half its value.

This destroyed wealth - real wealth, held by real people and institutions. Consumer confidence plummeted. Businesses cut investment. The initial shock was severe.

But consider what the crash did not do, at least directly. It did not cause banks to fail in large numbers - that came a year later. It did not contract the money supply - that contraction happened over the following three years.

It did not cause unemployment to reach 25 percent immediately - that figure was reached by 1932-1933. The crash was the starting pistol, but the race to catastrophe was run by subsequent policy failures.

The underlying speculative excess the crash revealed was real. The 1920s had seen overproduction in agriculture, a real estate bubble in Florida, and the kind of financial engineering that always precedes a reckoning.

The recession that followed the 1929 crash would have been serious under any circumstances. What made it the Great Depression was what happened next.

Irving Fisher, one of the most eminent American economists of the era, had been publicly confident about stock prices in the weeks before the crash.

In his influential 1933 paper "The Debt-Deflation Theory of Great Depressions," he revisited the disaster and developed the debt-deflation concept: as prices fell, the real value of debts rose, forcing debtors to sell assets to service obligations; this selling drove prices lower still, increasing real debt burdens further in a self-reinforcing spiral.

Fisher's framework anticipated later explanations of why ordinary recessions sometimes turn into catastrophic depressions.

Smoot-Hawley and the Collapse of Global Trade

In June 1930, President Hoover signed the Smoot-Hawley Tariff Act over the protests of more than 1,000 economists who signed a petition urging him to veto it.

The Act raised tariffs on more than 20,000 imported goods to historically high levels - average tariff rates on dutiable imports reached approximately 45 percent. It was intended to protect American farmers and manufacturers from foreign competition during the downturn.

The result was catastrophic. Trading partners retaliated. Canada, Britain, France, Germany, and dozens of other countries imposed their own tariffs on American goods. Global trade, which had already been weakening, collapsed.

Between 1929 and 1932, world trade fell by roughly 65 percent in value. American exports, which had stood at over five billion dollars in 1929, fell to just over two billion by 1932.

The damage was not merely economic abstraction. American farmers, who had hoped the tariff would protect them from foreign competition, found that retaliatory tariffs closed their export markets. Manufacturers that depended on imported components or exported finished goods were squeezed from both sides.

Douglas Irwin's Peddling Protectionism: Smoot-Hawley and the Great Depression (2011) provides the most comprehensive modern analysis, concluding that while Smoot-Hawley did not initiate the Depression, it significantly deepened and prolonged it by dismantling the trade networks that had sustained economic activity.[9]

The lesson was absorbed - at least temporarily. The post-war architecture of the General Agreement on Tariffs and Trade (GATT) and eventually the World Trade Organization was explicitly designed to prevent a repeat of the 1930s trade war spiral.

Whether that institutional memory persists against political pressures for protection is a recurring anxiety in international economic policy.

The Banking Panics: The Heart of the Catastrophe

Between 1930 and 1933, more than 9,000 American banks failed. Depositors who had done nothing wrong - who had simply kept their savings in what they assumed were sound institutions - lost everything. There was no deposit insurance.

A bank run, once started, could destroy a solvent bank: if enough depositors demanded their money simultaneously, no bank holding long-term loans could meet the demand.

The contagion spread. A bank failure in one town caused depositors in neighboring towns to worry about their banks, causing runs that caused further failures. The money supply fell by approximately one third between 1929 and 1933 - the most severe monetary contraction in American history.

With less money in circulation, prices fell, demand fell, businesses closed, workers were laid off, and demand fell further.

Ben Bernanke's influential 1983 paper, "Nonmonetary Effects of the Financial Crisis in the Propagation of the Great Depression," extended the monetary explanation by demonstrating that the banking collapse imposed additional costs beyond money supply contraction.[4]

Banks serve as information intermediaries: they have developed relationships with borrowers and have the specialized knowledge to assess creditworthiness. When thousands of banks failed, this accumulated information capital was destroyed.

New bank formation took years; the credit channels through which businesses funded operations and expansion were disrupted for a sustained period even after the money supply stabilized.

Milton Friedman and Anna Schwartz's analysis in A Monetary History of the United States (1963) placed the Federal Reserve at the center of this catastrophe.[1] The Fed had been created precisely to prevent bank panics. It had the tools to act as a lender of last resort, providing liquidity to solvent banks facing runs.

It did not do so, at least not adequately or consistently. When the banking system needed monetary expansion, it got contraction.

The most damning episode came in the fall of 1931. Britain had abandoned the gold standard in September, causing international investors to worry about whether the United States would follow. Gold began leaving the country as investors converted dollars to gold.

The Federal Reserve's response was to raise interest rates - making borrowing more expensive, tightening credit - in order to make dollar assets more attractive to foreign holders and stem the gold outflow.

This made economic sense from a narrow gold-standard perspective. From the perspective of an economy already in a severe depression, it was a catastrophic pro-cyclical tightening that accelerated the collapse.

The Gold Standard Trap

Barry Eichengreen's 1992 work Golden Fetters provides the international dimension of this story.[2] The gold standard was not merely a background condition of the Depression; it was an international transmission mechanism for deflation.

Under the gold standard, currencies were pegged to gold at fixed prices. A country experiencing capital outflows had to raise interest rates to attract gold, regardless of its domestic economic conditions.

This meant that once the United States began deflating, the gold standard compelled other countries to adopt contractionary policies to maintain their gold pegs - spreading the depression internationally.

The evidence for Eichengreen's thesis is striking: the date of a country's departure from the gold standard correlates almost perfectly with the date of its recovery from the Depression. Britain left gold in September 1931 and began recovering in 1932.

The United States effectively abandoned the gold standard domestically in 1933 and began recovering immediately. France stayed on gold until 1936 and suffered the longest and deepest depression of any major economy.

| Country | Left Gold Standard | GDP Recovery Began |

|---|---|---|

| United Kingdom | September 1931 | 1932 |

| Sweden | September 1931 | 1932 |

| United States | April 1933 | 1933 |

| Belgium | March 1935 | 1935 |

| France | September 1936 | 1937 |

| Netherlands | September 1936 | 1937 |

The gold standard had been designed to provide monetary stability and prevent inflationary excess. In the conditions of the 1930s, it became a straitjacket preventing the monetary expansion that recovery required.

This lesson was directly incorporated into the Bretton Woods system created after World War II, which sought exchange rate stability while preserving some capacity for monetary response - and its abandonment in the 1970s replaced it with floating exchange rates that give central banks full discretion over monetary conditions.

Keynes and the Economics of Depression

John Maynard Keynes provided the theoretical framework for understanding the Depression and the policy response to it.[3]

His 1936 masterwork, The General Theory of Employment, Interest and Money, was written in direct response to the Depression and challenged the orthodox assumption that markets would automatically return to full employment.

The orthodox view - sometimes called "Treasury view" or classical economics - held that government budget deficits were harmful because they crowded out private investment and that the right response to a recession was to cut spending, balance the budget, and let the economy self-correct.

This was Herbert Hoover's approach, and it was economically disastrous.

Keynes argued that in severe recessions, the economy could get stuck in a low-activity equilibrium. When demand collapses, businesses cut production and lay off workers, reducing income, which reduces demand further.

The paradox of thrift captures the key insight: it is rational for any individual household to save more when facing economic uncertainty, but when every household does this simultaneously, aggregate demand collapses, incomes fall, and everyone ends up with less - including less saving.

Individual rationality produces collective self-defeat.

The policy implication was that only government could break the spiral: by spending when the private sector would not, the government could restore aggregate demand and break the deflationary loop.

Keynes also identified the liquidity trap - a condition in which interest rates fall so low that monetary policy loses its traction, as individuals and institutions hoard cash rather than invest regardless of the interest rate.

In such conditions, fiscal policy (government spending) must substitute for monetary policy. The New Deal was the imperfect, inconsistent attempt to implement this logic.

Hoover's Response and Its Failures

Herbert Hoover is unfairly caricatured as having done nothing in response to the Depression. In fact, he signed the Reconstruction Finance Corporation into existence, he attempted some public works, and he was more activist than his predecessors would have been.

But his responses were inadequate, and one of them - Smoot-Hawley - actively made things worse.

Hoover's fundamental failure was his commitment to balanced budgets. His orthodox economics told him that government borrowing would crowd out private investment and undermine confidence.

As the Depression deepened and tax revenues fell, Hoover raised taxes in 1932 in an attempt to balance the budget - exactly the wrong fiscal policy for a contracting economy. Government spending was contractionary when it needed to be expansionary.

Hoover also believed, with some justification, that much of the financial sector's problem was structural rather than cyclical - that liquidating bad debts was necessary before recovery could begin.

Andrew Mellon, his Treasury Secretary, reportedly advised him to "liquidate labor, liquidate stocks, liquidate the farmers, liquidate real estate.

It will purge the rottenness out of the system." This liquidationist view, while intellectually coherent in a narrow sense, ignored the difference between a controlled deleveraging and a self-reinforcing deflationary spiral.

The liquidationist perspective had been developed by economists in the Austrian tradition, including Friedrich Hayek, who argued that the boom of the 1920s had created malinvestments that needed to be cleared before genuine growth could resume.

Hayek and Keynes conducted one of the most famous debates in the history of economics through the pages of academic journals in the early 1930s, with Keynes arguing for intervention and Hayek warning that it would merely perpetuate the distortions.

The historical evidence of the 1930s has generally been read as vindicating Keynes, but the Austrian critique of easy money creating boom-bust cycles has never disappeared from economic debate.

The New Deal: What It Did and Did Not Accomplish

Franklin Roosevelt's New Deal, begun after his inauguration in March 1933, was transformative - but not as uniformly effective as popular memory suggests.

Its clearest success was stopping the banking panics. Roosevelt's banking holiday, declared on his first day in office, halted the cascade of failures.

The Federal Deposit Insurance Corporation (FDIC), created in 1933, eliminated bank runs at the depositor level by guaranteeing deposits - giving ordinary people no reason to panic-withdraw their savings.

This was probably the single most consequential institutional change of the New Deal era, and its effects persist today.

Abandoning the gold standard domestically in 1933 - allowing the dollar to depreciate and ending deflationary constraints on monetary policy - also had immediate positive effects. Industrial production, which had been in freefall, began recovering almost immediately after FDR took office and departed from gold.

The public works programs - the Civilian Conservation Corps, the Works Progress Administration, the Public Works Administration - put millions of Americans to work and injected demand into the economy.

They also built lasting infrastructure: roads, bridges, schools, parks, and public buildings that remain in use today. The WPA alone employed approximately 8.5 million workers between 1935 and 1943.

But the New Deal's limitations became starkly visible in 1937. Convinced the recovery was secure, Roosevelt moved toward fiscal austerity - cutting spending and allowing tax increases to take effect. The economy collapsed immediately.

The "Roosevelt Recession" of 1937-1938 sent unemployment back toward 20 percent, erasing four years of recovery.

The episode is the most direct empirical demonstration of Keynesian economics in the historical record: fiscal contraction during an incomplete recovery reverses the recovery.

The New Deal was also a political coalition, not an economic program - it contained programs that worked against each other, cartelizing industries in ways that may have actually prolonged the Depression.

Economic historian Robert Higgs has argued that "regime uncertainty" - the unpredictable regulatory and tax environment of the New Deal - discouraged private investment throughout the 1930s.[8]

Higgs's data on private investment, which remained below pre-Depression levels until 1941, is the most compelling evidence for this view.

The Human Geography of the Depression

Any account of the Depression that concentrates solely on macroeconomic mechanisms risks losing sight of the uneven human experience of the catastrophe. The Depression's impact was heavily differentiated by race, region, and occupation in ways that policy largely failed to address.

African Americans experienced the Depression with particular severity. Already concentrated in the most vulnerable sectors - agricultural labor, domestic service, unskilled industrial work - Black workers faced discriminatory displacement as white workers took jobs previously considered "Black work." Unemployment rates in Black communities reached 40 to 50 percent in some cities.

New Deal programs, administered largely through Southern Democratic political structures, routinely excluded or shortchanged Black recipients: the Agricultural Adjustment Administration's crop reduction payments went to white landowners, not Black tenant farmers; the National Recovery Administration's industry codes frequently set lower minimum wages for occupations dominated by Black workers.

Ira Katznelson's Fear Itself (2013) documents how the New Deal's racial exclusions shaped both the Depression's impact and its remedies.[10]

The Dust Bowl added environmental catastrophe to economic disaster in the Southern Plains.

Years of unsustainable dry-land wheat farming had stripped the native prairie grass, and when drought struck in the early 1930s, massive dust storms - "black blizzards" - stripped the topsoil across parts of Oklahoma, Texas, Kansas, and Colorado.

An estimated 2.5 million people left the Dust Bowl region during the 1930s. The Okies who made their way to California's agricultural valleys - described by Steinbeck with unflinching accuracy - found exploitation and hostility rather than the promised land.

Their experience made visible the structural vulnerability of agricultural workers in a capitalist labor market.

What Actually Ended the Depression

The Great Depression is conventionally dated as ending with World War II - or rather, with the massive defense mobilization that preceded and accompanied American entry. Government spending rose from roughly 10 percent of GDP in 1940 to more than 40 percent by 1944. Unemployment fell to near zero.

Industrial production expanded dramatically.

This fact has been interpreted in opposite ways. Keynesians argue it proves the case for fiscal stimulus: the New Deal was not large enough, but when government spending finally reached sufficient scale, full employment was restored.

Critics argue that wartime mobilization is categorically different from peacetime fiscal stimulus - the government was not merely spending, it was commandeering resources, drafting labor, and compelling production in ways that cannot be replicated in peacetime.

Christina Romer's influential research (Journal of Economic History, 1992) suggests that monetary factors deserve more credit for the recovery than fiscal policy, at least through the late 1930s.[6]

Her analysis attributes a significant portion of the pre-war recovery to the monetary expansion made possible by departing the gold standard and by the gold inflows from a destabilizing Europe that enabled the money supply to grow.

The fiscal stimulus of the New Deal, while real, was too small relative to the size of the output gap to achieve full recovery on its own.

The debate is not merely academic. It defines the policy toolkit for fighting severe recessions and the theoretical frameworks used by central bankers and treasury officials when the next crisis arrives.

The Depression in Germany and Its Global Consequences

The Great Depression's political consequences were not confined to the United States. In Germany, the Depression's impact was catastrophic and, ultimately, world-historical.

The Weimar Republic, already politically fragile, was overwhelmed by the economic collapse. Unemployment reached approximately 30 percent by 1932. The middle classes, devastated by the hyperinflation of the early 1920s and now facing depression, provided mass support for the National Socialist movement.[11]

Hitler was appointed Chancellor in January 1933 - weeks before Roosevelt's inauguration in March - in large part because the mainstream parties had no convincing response to economic catastrophe. The Nazi vote share rose from 2.6 percent in 1928 to 37.4 percent in July 1932 as economic conditions deteriorated.

This is not to say that the Depression caused Hitler - the causes of National Socialism are far more complex. But the Depression destroyed the economic and political conditions under which Weimar democracy might have survived.

The connections between the Great Depression, the collapse of democratic institutions under economic stress, and the path to World War II are among the most consequential chains of causation in modern history.

The 2008 Echo and the Lessons Applied

When the financial crisis of 2008 threatened to replicate the banking collapse of the early 1930s, the policy response was explicitly informed by Depression history. Ben Bernanke, then Federal Reserve Chairman and the leading academic expert on the Depression, made good on his 2002 promise to Friedman.

The Fed flooded the financial system with liquidity through emergency lending facilities, asset purchases, and near-zero interest rates. The Treasury and Federal Deposit Insurance Corporation guaranteed bank deposits and money market funds.

Congress passed a fiscal stimulus package in 2009 worth approximately $787 billion. The policy response was imperfect and insufficient by many economists' reckoning - the recovery was slow and incomplete - but it prevented the banking collapse and deflationary spiral that defined the Depression.

The contrast is instructive. In 1930-1933, the money supply fell 33 percent. In 2008-2009, the Fed expanded its balance sheet by trillions of dollars. In the early 1930s, the government tightened fiscal policy during contraction. In 2009, it expanded it.

The Great Depression had served as an enormous, terrible natural experiment in what not to do, and in 2008, the lesson was at least partially absorbed.

The COVID-19 recession of 2020 provided a second test. The fiscal response - trillions of dollars in direct transfers, expanded unemployment insurance, and business support across most developed economies - was by far the largest peacetime fiscal expansion in history, explicitly designed to prevent a deflationary spiral of the 1930s type.

The speed of the recovery, at least in employment terms, was without historical precedent for a shock of comparable initial magnitude.

Whether this represents the permanent absorption of the Depression's lessons or a temporary departure from austerity norms that will reassert themselves remains to be seen.

For related reading, see how recessions happen, what is central banking, and what caused World War Two.

Sources & Further Reading

- Friedman, M., & Schwartz, A. J. (1963). A Monetary History of the United States, 1867-1960. Princeton University Press.

- Eichengreen, B. (1992). Golden Fetters: The Gold Standard and the Great Depression, 1919-1939. Oxford University Press.

- Keynes, J. M. (1936). The General Theory of Employment, Interest and Money. Macmillan.

- Bernanke, B. S. (1983). Nonmonetary effects of the financial crisis in the propagation of the Great Depression. American Economic Review, 73(3), 257-276.

- Fisher, I. (1933). The debt-deflation theory of great depressions. Econometrica, 1(4), 337-357. DOI: 10.2307/1907327

- Romer, C. D. (1992). What ended the Great Depression? Journal of Economic History, 52(4), 757-784. DOI: 10.1017/S002205070001189X

- Temin, P. (1989). Lessons from the Great Depression. MIT Press.

- Higgs, R. (1997). Regime uncertainty: Why the Great Depression lasted so long and why prosperity resumed after the war. The Independent Review, 1(4), 561-590.

- Irwin, D. A. (2011). Peddling Protectionism: Smoot-Hawley and the Great Depression. Princeton University Press.

- Katznelson, I. (2013). Fear Itself: The New Deal and the Origins of Our Time. Liveright.

- Tooze, A. (2006). The Wages of Destruction: The Making and Breaking of the Nazi Economy. Allen Lane.

- Steinbeck, J. (1939). The Grapes of Wrath. Viking Press.

Frequently Asked Questions

What caused the Great Depression?

The Great Depression had multiple interlocking causes, none of which alone would have been sufficient to produce a decade-long catastrophe. The stock market crash of October 1929 is the most famous trigger, but most economic historians now agree it was not the primary cause. The crash exposed the speculative excess of the 1920s and wiped out wealth, but it was the subsequent policy failures that transformed a severe recession into the Great Depression.The most consequential cause was the collapse of the banking system between 1930 and 1933. Over 9,000 banks failed in the United States, and the money supply fell by approximately one third. Milton Friedman and Anna Schwartz, in their landmark 1963 work ‘A Monetary History of the United States,’ argued that the Federal Reserve bore primary responsibility: it failed to act as a lender of last resort, allowed deflationary bank runs to cascade, and even raised interest rates in 1931 to defend the gold standard while the economy was collapsing.The gold standard compounded the problem by preventing governments from expanding their money supplies in response to deflation. Countries that abandoned gold earlier, Britain in 1931, recovered faster. The Smoot-Hawley Tariff of 1930 triggered retaliatory trade barriers worldwide, collapsing global trade by roughly 65 percent. And Hoover’s insistence on balanced budgets meant fiscal policy worked against recovery rather than for it. The result was a self-reinforcing deflationary spiral: falling prices led consumers to delay purchases, which caused more business failures, which caused more unemployment, which caused further falls in demand.

Was the stock market crash the main cause of the Great Depression?

The stock market crash of October 1929, Black Thursday on October 24 and Black Tuesday on October 29, is the iconic starting point of the Great Depression, but modern economic historians are emphatic that it was not the primary cause. The crash was real, damaging, and revealing, but the Depression did not become the Depression because of the crash alone.The stock market collapse exposed the speculative excesses of the 1920s. Stock prices had been driven upward by easy credit and margin buying, investors borrowing to speculate, sometimes putting up only 10 percent of the purchase price in cash. When prices fell, margin calls forced sales, which drove prices lower still. Wealth was destroyed. Consumer confidence collapsed.But here is the key point: the American economy had survived stock market panics before, including the severe panic of 1907, without anything resembling the Depression. What was different this time was what happened afterward. The banking panics of 1930-1933, the Federal Reserve’s failure to provide liquidity, the deflationary collapse of the money supply, the gold standard constraints, and the protectionist trade policies, these were what turned a serious recession into a decade-long catastrophe.By 1932, industrial production had fallen by nearly half, unemployment had reached 25 percent, and thousands of banks had closed. The stock market crash started the chain reaction, but it was the institutional and policy failures that made the Depression great. Ben Bernanke, who studied the Depression extensively before becoming Federal Reserve chairman, said when the 2008 crisis hit: ‘We won’t do it again’, referring explicitly to the Fed’s failures of the 1930s.

What role did the Federal Reserve play in the Great Depression?

The Federal Reserve’s role in the Great Depression is one of the most debated and consequential questions in economic history. Milton Friedman and Anna Schwartz, in ‘A Monetary History of the United States’ (1963), made the provocative and influential argument that the Federal Reserve did not merely fail to prevent the Depression, it actively caused the worst of it through a series of catastrophic policy decisions.The Fed was created in 1913 precisely to prevent the kind of bank panics that had plagued the American economy throughout the 19th century. Its job was to act as a lender of last resort, providing liquidity to solvent banks facing temporary runs. In 1930-1933, it failed to do this. When banks began failing in waves, the Fed stood by as the money supply contracted by a third. Bank deposits were wiped out. People who had saved their lives away lost everything. Businesses could not get credit. Investment collapsed.Worse, in the fall of 1931, as the Depression deepened, the Federal Reserve actually raised interest rates, not to fight inflation, which was nowhere in sight, but to defend the United States’ commitment to the gold standard after Britain’s departure from it sparked capital outflows. This pro-cyclical tightening during a contraction was, in Friedman and Schwartz’s view, the single most damaging policy decision in the Depression.The argument is not universally accepted, some economists emphasize demand-side factors and structural problems, but it has been enormously influential. When Ben Bernanke spoke at Friedman’s 90th birthday in 2002, he said directly: ‘You’re right, we did it. We’re very sorry. But thanks to you, we won’t do it again.’ In 2008, Bernanke made good on that pledge, flooding the financial system with liquidity when the banking system threatened to seize up.

What did the gold standard have to do with the Great Depression?

The gold standard was not just a background condition of the Great Depression, it was, according to many economic historians, one of its central mechanisms. Barry Eichengreen’s 1992 book ‘Golden Fetters’ argues that the gold standard was the primary reason the Depression spread internationally and lasted as long as it did.Under the gold standard, currencies were pegged to gold at fixed prices. Countries had to maintain gold reserves to back their currencies, which meant they could not simply print money in response to deflation. When one country experienced capital outflows, investors moving money abroad, it had to raise interest rates to attract gold back, even if raising rates was the last thing a contracting economy needed. This is exactly what the Federal Reserve did in 1931, and what other gold standard countries did as well.The result was a transmission mechanism for depression: deflation in one country spread to others through the gold standard’s constraints. Countries that left the gold standard earliest recovered earliest. Britain left in September 1931, its economy stabilized. The Scandinavian countries left shortly after and avoided the worst. The United States effectively left the gold standard for domestic purposes in 1933 when FDR took office and suspended gold convertibility, and the economy began to recover almost immediately. France stayed on gold until 1936 and suffered through the Depression longer than almost any other major economy.The evidence is striking: the date of recovery from the Great Depression correlates very strongly with the date of departure from gold. The gold standard, designed to provide stability, had become a straightjacket preventing the monetary expansion that recovery required.

Did the New Deal end the Great Depression?

Whether the New Deal ended the Great Depression is one of the most contested questions in American economic history, and the honest answer is: it helped, but it was not sufficient, and the question of what finally ended the Depression remains genuinely debated.Franklin Roosevelt’s New Deal, launched after his inauguration in March 1933, had several components. The banking holiday and establishment of deposit insurance (FDIC) stopped the banking panics and restored confidence in the financial system, this was probably its most consequential achievement. Abandoning the gold standard for domestic purposes allowed monetary expansion. Public works programs, the Civilian Conservation Corps, the Works Progress Administration, the Public Works Administration, employed millions and injected demand into the economy.But the New Deal also had failures. Roosevelt was not a Keynesian in any systematic sense. In 1937, convinced that the recovery was secure, he moved toward budget balance, cutting spending and raising taxes. The economy promptly collapsed again, the ‘Roosevelt Recession’ of 1937-1938 sent unemployment back toward 20 percent. This episode actually proved the Keynesian argument: fiscal contraction during recovery aborts the recovery.The Depression is generally considered to have ended only with World War II mobilization. Defense spending from 1940 onward was massive, unemployment fell to near zero, and the economy expanded dramatically. Whether this proves the Keynesian case for government spending or simply reflects the unique conditions of total war mobilization is still debated. What is clearer is that the New Deal alone was not large enough to fully end a contraction of that magnitude, and that the Fed’s failures had made the hole very, very deep.

What lessons did the Great Depression teach economists?

The Great Depression transformed economics. Before it, the dominant view was roughly that markets self-corrected: recessions would resolve as prices fell until demand revived. The Depression made this view untenable. Prices fell dramatically, and the economy got worse, not better. John Maynard Keynes’s ‘General Theory of Employment, Interest and Money’ (1936) provided the theoretical explanation: in a severe contraction, individual rational behavior, saving, cutting costs, waiting, becomes collectively self-defeating. The ‘paradox of thrift’ holds that when everyone saves simultaneously, aggregate demand collapses and the economy contracts further. Only government spending can break the spiral.Friedman and Schwartz added the monetary lesson: central banks must act as lenders of last resort and prevent banking panics from contracting the money supply. This lesson was dramatically applied in 2008 when the Federal Reserve, led by Bernanke, provided unprecedented liquidity to financial markets to prevent a repeat of the 1930s banking collapse.The gold standard lesson was also absorbed: rigid exchange rate commitments that prevent monetary response to deflationary shocks are dangerous. The post-war Bretton Woods system tried to combine exchange rate stability with some flexibility, and its eventual successor, floating exchange rates, gives central banks the freedom to respond to crises that gold standard countries lacked.The Smoot-Hawley lesson, that protectionism in a crisis becomes mutually destructive as retaliations compound, underpinned the post-war drive toward trade liberalization through GATT and later the WTO. Whether these institutional lessons will hold against future political pressures remains to be seen, but the Great Depression’s shadow still shapes every major economic policy crisis response.