Wealth inequality is the unequal distribution of accumulated net worth - the total value of assets minus liabilities - across a population.

Unlike income inequality, which measures disparities in annual earnings, wealth inequality captures the compounding effects of savings, investment returns, inheritance, and economic advantage accumulated over lifetimes and across generations.

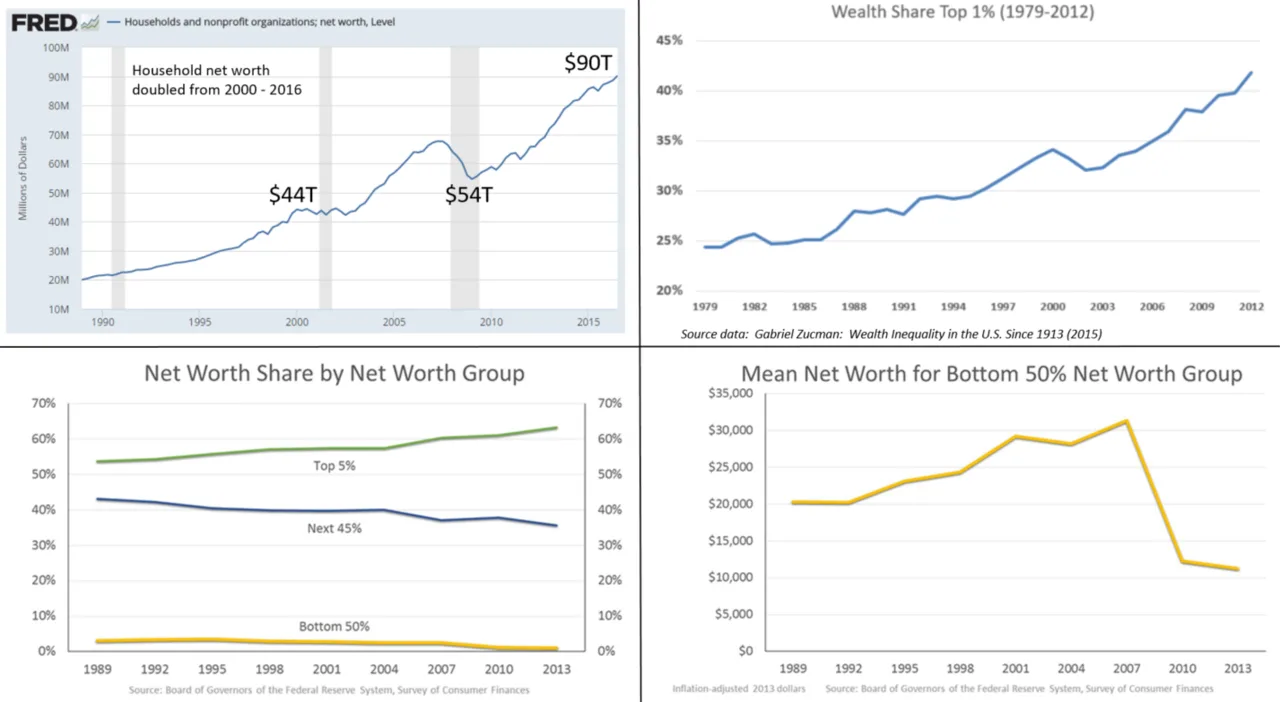

In the United States, the top 1% of households hold approximately 31% of total household wealth, while the bottom 50% - roughly 65 million families - collectively own about 2.6%, according to 2022 Federal Reserve data.

This degree of concentration has no parallel among developed democracies and has widened substantially since the 1980s.

Understanding what these numbers mean, how they are measured, what drives them, and what - if anything - should be done about them requires engaging with several distinct questions that are often collapsed together in public debate. This article separates those questions and examines each with the care the topic demands.

"When the rate of return on capital exceeds the rate of growth of output and income, capitalism automatically generates arbitrary and unsustainable inequalities that radically undermine the meritocratic values on which democratic societies are based." - Thomas Piketty, Capital in the Twenty-First Century (2013)

Defining Terms: Wealth vs. Income Inequality

A persistent confusion in public debate is the conflation of wealth inequality and income inequality. These are related but structurally distinct phenomena that require different measurement approaches and different policy responses.

Income is a flow: the money received in a period of time - wages, salaries, rental income, dividends, interest, business profits. Income inequality describes the dispersion of these annual flows across the population. When we say a CEO earns 350 times what the median worker earns, we are describing income inequality.

Wealth is a stock: accumulated net worth at a point in time - the value of all assets (real estate, financial investments, business equity, retirement accounts, physical possessions) minus all liabilities (mortgages, student loans, credit card debt, other obligations).

Wealth inequality describes the dispersion of this accumulated net worth. When we say the top 1% holds more wealth than the bottom 50%, we are describing wealth inequality.

Wealth is always more unequally distributed than income, for a structural reason: wealth accumulates over time. Each year's income that is not consumed adds to wealth. Returns on existing wealth generate more wealth. Initial advantages compound.

The longer a family has been wealthy, the more wealth it tends to accumulate, absent taxation, shocks, or redistribution. This compounding dynamic is why understanding compound interest matters not just for personal investing but for understanding how inequality grows.

The distinction matters enormously for policy. Policies that address income inequality (minimum wage increases, earned income tax credits, progressive income taxes) do not directly address wealth concentration.

Wealth transfers persist across generations through inheritance, networks, educational advantages, and the returns on existing assets, even when current income flows are equalized.

Measuring Inequality: The Gini Coefficient and Beyond

How the Gini Works

The most widely used summary statistic for inequality is the Gini coefficient, developed by Italian statistician Corrado Gini in 1912. It remains the standard measure used by the World Bank, OECD, and most national statistical agencies.

The Gini is calculated from the Lorenz curve, which plots the cumulative percentage of income (or wealth) received by the bottom X% of the population.

On a perfectly equal distribution, the bottom 20% would have 20% of the income, the bottom 50% would have 50%, and so on - forming a straight diagonal line. On any real distribution, the curve falls below this diagonal, bowing downward.

The Gini coefficient is the area between the Lorenz curve and the diagonal of perfect equality, expressed as a fraction of the total area under the diagonal. It ranges from 0 (perfect equality, everyone has the same) to 1 (perfect inequality, one person has everything).

Gini Values in Context

| Country / Measure | Gini Coefficient | Interpretation |

|---|---|---|

| US income (2022) | ~0.49 | Among the highest in the developed world |

| Germany income (2022) | ~0.31 | Moderate, reflecting strong redistribution |

| Sweden income (2022) | ~0.29 | Low, high taxation and social transfers |

| US wealth (2022) | ~0.85 | Extreme concentration |

| Global wealth (2023) | ~0.89 | Near-maximum concentration |

| Perfect equality | 0.00 | Theoretical benchmark |

These numbers reveal a critical pattern: US income inequality is high by developed-country standards, but US wealth inequality is extreme even by global standards. Income can be redistributed relatively quickly through tax and transfer policy; wealth redistribution is structurally harder, slower, and more politically contested.

Limitations of the Gini

The Gini is useful but imperfect. It collapses an entire distribution into one number, losing information about where in the distribution inequality is concentrated.

Two societies with the same Gini can look very different - one might have a compressed middle with extreme wealth at the top, while another might have deep poverty at the bottom with a relatively prosperous middle.

Researchers supplement the Gini with percentile ratios (the P90/P10 ratio compares income at the 90th percentile to the 10th), share measures (the fraction of total income or wealth going to the top 1%, 10%, or 0.1%), and Palma ratios (the ratio of income captured by the top 10% to income captured by the bottom 40%).

Each reveals different dimensions of the same inequality.

The Data: What Wealth Concentration Actually Looks Like

The most comprehensive ongoing data on US wealth distribution comes from the Federal Reserve's Survey of Consumer Finances (published every three years) and the Federal Reserve's Distributional Financial Accounts (updated quarterly). As of the most recent available data:

- The top 1% of households hold approximately 31-32% of total household wealth

- The top 10% hold approximately 67-68%

- The bottom 50% hold approximately 2.6%

- The bottom 25% have near-zero or negative net worth (debts exceed assets)

For historical perspective: in the mid-1970s, the top 1% held roughly 22% of wealth and the bottom 50% held closer to 5-6%. The distribution was still highly unequal, but significantly less concentrated than today. The turning point, visible in virtually every dataset, came in the early 1980s.

The Racial Wealth Gap

Wealth inequality in the United States is deeply entangled with racial history. The Federal Reserve's data consistently shows:

- White households' median wealth (

$285,000 in 2022) is approximately 7-8 times the median wealth of Black households ($44,000) - Hispanic households' median wealth falls between these figures (~$61,000)

- Asian American households show higher median wealth (~$536,000 in 2022) but with enormous internal variation by national origin

The racial wealth gap reflects the compounding effects of centuries of exclusion from wealth-building opportunities: redlining (the systematic denial of mortgages and insurance to Black neighborhoods, documented by Richard Rothstein in The Color of Law, 2017), exclusion from GI Bill benefits that built white middle-class wealth after World War II, discriminatory lending practices, and the intergenerational transmission of both wealth and its absence.

Research by economists Darrick Hamilton and William Darity Jr. (2010) at The New School demonstrated that the racial wealth gap persists even after controlling for income, education, and savings rates - evidence that the gap is driven primarily by differences in initial wealth endowments and inherited advantage rather than by differences in financial behavior.

Piketty's r > g: The Central Theoretical Framework

The most influential theoretical framework for understanding rising wealth inequality in recent decades is Thomas Piketty's r > g thesis, developed in Capital in the Twenty-First Century (2013).

Originally published in French, the English translation became an unexpected global bestseller, reaching audiences far beyond academic economics.

The Core Argument

Piketty's framework rests on a deceptively simple inequality:

r = the rate of return on capital (the annual percentage return earned by wealth: dividends, rent, interest, capital gains, profits)

g = the rate of economic growth (the growth rate of GDP and national income)

When r > g: Capital owners receive returns that exceed the growth rate of the overall economy. This means wealth grows faster than incomes. Over time, the share of total national income going to capital increases relative to the share going to labor. Wealth becomes more concentrated in fewer hands.

The historical evidence: Piketty and his collaborators - notably Emmanuel Saez and Gabriel Zucman at the University of California, Berkeley - assembled the most comprehensive historical data series ever compiled on wealth and income distribution for France, Britain, the United States, and other countries, spanning centuries.

Their findings:

- Before World War I, r substantially exceeded g in most rich countries, and wealth was highly concentrated - the Gilded Age was not an aberration but the historical norm

- The period from roughly 1914 to 1970 saw unusual compression of wealth inequality, driven primarily by the physical destruction of capital in two World Wars, depression-era collapse of asset values, high progressive taxation, strong unions, and unusually strong post-war economic growth

- Since the early 1980s, with slower growth rates and rising returns to capital, the historical pattern of r > g has reasserted itself, and wealth concentration has risen toward pre-World War I levels

Critiques and Counterarguments

Piketty's thesis generated the most extensive academic debate in economics since Milton Friedman's monetarism. Key criticisms include:

Data questions: Economist Lawrence Summers (2014) challenged specific aspects of Piketty's capital measurements, arguing that his concept of capital conflates productive capital (factories, equipment, intellectual property) with land and real estate in ways that muddle the analysis.

Matthew Rognlie (2015) at MIT showed that much of the rising capital share Piketty documented was attributable to housing - specifically, rising land values in cities with restricted supply - rather than to productive capital accumulation.

Returns are not uniform: Average capital returns appear high partly because some investments have exceptional returns while many others fail. Diversified, risk-adjusted returns on wealth are lower than headline figures suggest.

Greg Mankiw (2015) at Harvard argued that much of the measured return to capital reflects compensation for bearing risk rather than the passive accumulation Piketty describes.

Policy proposals questioned: Piketty's proposed solution - a global wealth tax - was widely criticized as politically impractical and administratively challenging. Capital is mobile; wealth is harder to value than income; and international coordination at the required level has no historical precedent.

The critics do not generally dispute that inequality has risen or that capital returns matter. The debate is about the mechanisms driving the trend and the severity of the self-reinforcing feedback loop.

What Actually Drives Wealth Inequality

The academic literature identifies several interacting drivers of rising wealth concentration. No single factor explains the trend; the causes are multiple, reinforcing, and vary in relative importance across countries and time periods.

Technology and the Skill Premium

Since the 1980s, technological change has increased the relative productivity and earnings of high-skill workers faster than low-skill workers.

Economists Claudia Goldin and Lawrence Katz at Harvard documented this in The Race Between Education and Technology (2008), showing that when education systems fail to keep pace with technological demands, the earnings gap between skilled and unskilled workers widens dramatically.

This effect operates through two channels: income (high-earners save more and accumulate wealth faster) and direct returns on technology investments that benefit capital owners. The explosion of wealth in the technology sector since the 1990s - producing more billionaires than any other industry - illustrates both channels simultaneously.

Winner-Take-Most Market Structures

Globalization and digitization have created markets where top performers capture a disproportionate share of rewards. In markets with strong network effects (social media, operating systems, search), the leading player can achieve near-monopoly positions.

In superstar labor markets (sports, entertainment, technology, finance), small differences in skill produce enormous differences in compensation.

Economist Sherwin Rosen described this phenomenon in his seminal 1981 paper "The Economics of Superstars": when the best performer can reach a global audience at minimal marginal cost (through recordings, software, broadcasting, or digital platforms), the market concentrates rewards at the top.

This dynamic has intensified with every expansion of digital reach.

Declining Labor Bargaining Power

Union membership in the US fell from roughly 35% of private-sector workers in the mid-1950s to approximately 6% by the early 2020s, according to Bureau of Labor Statistics data.

Research by economists Henry Farber, Daniel Herbst, Ilyana Kuziemko, and Suresh Naidu (2021) at Princeton found that this decline explains a substantial portion of the growth in income inequality since the 1970s.

The mechanism is direct: unions compress the wage distribution by raising wages for workers at the middle and lower end while limiting executive compensation growth.

Their decline shifted bargaining power from employees to employers and shareholders, redirecting a larger share of economic output toward capital owners. Understanding labor economics helps clarify why this structural shift matters so much.

Tax Policy Changes

Top marginal income tax rates in the US fell from 91% in the early 1960s to 70% in the late 1970s to 28% under Reagan's 1986 tax reform. Long-term capital gains rates have generally been lower than ordinary income rates, benefiting wealthy asset owners disproportionately.

Estate tax exemptions rose from roughly $600,000 in 1997 to over $13 million per individual by 2024.

Research by Thomas Piketty, Emmanuel Saez, and Stefanie Stantcheva (2014) published in the American Economic Journal: Economic Policy found that reductions in top tax rates were associated with higher pre-tax income concentration - suggesting that lower rates did not merely change after-tax distributions but altered the incentive structure for rent-seeking behavior at the top.

Assortative Mating

High earners increasingly marry high earners. The expansion of higher education created shared social environments for high-earning professionals.

Research by economists Jeremy Greenwood, Nezih Guner, and others (2014) at the University of Pennsylvania estimated that if the patterns of assortative mating observed in 1960 had persisted (when cross-class marriages were more common), household income inequality would be measurably lower today.

When two high-earning professionals combine household wealth, the result accelerates concentration at the top.

Compounding and Inheritance

Wealth generates returns that generate more wealth. The longer and larger the initial advantage, the larger the compounded advantage over time. Inheritance transfers these advantages across generations.

Research by Piketty, Saez, and Zucman estimates that inherited wealth accounts for a substantial and growing share of total wealth concentration - rising from roughly 50% of total wealth in the 1970s toward 60-65% in recent decades.

This dynamic means that understanding how the stock market works is not just a matter of personal finance - it is essential context for understanding how wealth concentrates through differential access to financial markets.

Wealth Inequality vs. Economic Mobility

A common response to concerns about inequality is to argue that mobility matters more than the snapshot picture of inequality. If people can move through the distribution - if today's poor can become tomorrow's middle class, and vice versa - then a high Gini coefficient overstates the problem.

This is a serious argument. The United States has historically told itself a story of exceptional upward mobility - the American Dream - that posits wide access to economic advancement regardless of starting conditions.

The research from Raj Chetty and his colleagues at the Opportunity Insights project at Harvard has substantially revised this story. Their work, tracking millions of Americans across generations using anonymized tax data, produces findings that are difficult to dismiss:

- Absolute mobility (the share of children who earn more than their parents at the same age) has fallen from approximately 90% for children born in 1940 to approximately 50% for children born in 1984

- Relative mobility (how much a child's economic outcome is predicted by their parents' economic position) is lower in the US than in most European countries - the "Great Gatsby curve" documented by Canadian economist Miles Corak (2013) shows that countries with higher inequality tend to have lower intergenerational mobility

- Geographic variation within the US is enormous: children born poor in Salt Lake City or San Jose have mobility rates comparable to Denmark, while children born poor in Atlanta, Charlotte, or Milwaukee have mobility rates closer to developing countries

- Key factors associated with higher mobility include: mixed-income neighborhoods, low residential segregation, lower local inequality, stronger social capital, better schools, and two-parent household prevalence

The relationship between inequality and mobility is not merely coincidental. Chetty's work suggests they are causally linked: high inequality widens the gaps between rungs of the economic ladder, making each step harder to climb.

A society where the distance between the 25th and 75th percentile of income is vast requires more resources, more luck, and more exceptional effort to traverse.

The Policy Debate

The debate about what to do about wealth inequality involves both empirical disputes (what would actually reduce inequality, and at what cost?) and normative disputes (how much inequality is problematic, and why?).

The Case for Active Intervention

Arguments for addressing wealth inequality include:

- Political power concentration: Concentrated wealth translates into concentrated political influence through campaign contributions, lobbying, media ownership, and the revolving door between government and the private sector. Political scientists Martin Gilens and Benjamin Page (2014) at Princeton found that the policy preferences of economic elites are substantially more likely to become law than the preferences of average citizens

- Diminishing marginal utility: An additional $10,000 matters enormously to a family earning $30,000 and is negligible to a billionaire. Extreme concentration therefore reduces aggregate welfare even if total wealth is unchanged

- Social cohesion erosion: Cross-country research by epidemiologists Richard Wilkinson and Kate Pickett, published in The Spirit Level (2009), found that more unequal societies have worse outcomes on virtually every measure of social health - mental illness, drug abuse, obesity, educational performance, imprisonment, social trust - even after controlling for absolute income levels

- Mobility impairment: As Chetty's work demonstrates, high inequality appears to impede the fluidity of economic movement, hardwiring initial advantages and disadvantages across generations

Policy Instruments Under Debate

Progressive income taxation redistributes income flows. Evidence from the post-World War II era suggests that higher top marginal rates (which exceeded 70% in the US from 1936 to 1980) coincided with strong economic growth and lower inequality, though causation is debated.

Wealth taxes directly target accumulated net worth rather than income flows. Elizabeth Warren's proposed 2% annual tax on wealth above $50 million generated enormous academic debate.

France's wealth tax (ISF) was abolished in 2017 after evidence of capital flight, though economists Gabriel Zucman and Emmanuel Saez have argued that a well-designed wealth tax with robust enforcement could be effective.

The policy question of whether wealth taxes can be practically administered without excessive evasion remains unresolved.

Estate and inheritance taxes address intergenerational wealth transmission. The US estate tax currently has a high exemption (~$13.6 million per individual in 2024, scheduled to drop to ~$7 million in 2026). European countries generally have lower exemptions and higher rates.

Housing and urban policy addresses a specific driver: in high-cost metropolitan areas, rising land and housing values have generated enormous wealth for existing homeowners while pricing out renters.

Economists like Edward Glaeser at Harvard argue that zoning reform and housing supply expansion address one of the largest drivers of wealth inequality in metropolitan areas.

The Case for Restraint

Economists skeptical of aggressive redistribution argue that high inequality may partly reflect high returns to innovation and productive entrepreneurship; that redistribution creates efficiency losses and incentive distortions; that the focus should be on expanding opportunity through education, infrastructure, and mobility rather than compressing outcomes; and that aggregate economic growth matters more than distributional outcomes for long-term welfare improvements.

The efficiency-equity tradeoff is genuine and well-studied. Most economists accept that some redistribution is welfare-improving; they disagree about the magnitude, the instruments, and the tradeoffs at specific policy margins. Understanding fiscal policy provides the context needed to evaluate these competing claims.

What the Evidence Supports

Setting aside the normative debates about what should be done, the empirical picture is relatively clear on several points:

- Wealth inequality in the US and most rich countries has risen substantially since the early 1980s, after a historically anomalous period of compression

- Wealth is substantially more concentrated than income, and the gap between wealth concentration and income concentration has widened

- The causes are multiple and interacting: technology, market structure, declining labor bargaining power, tax policy changes, compounding dynamics, assortative mating, and inheritance

- Economic mobility has declined in the United States, and high inequality appears to impede rather than coexist comfortably with mobility

- Policy tools exist to address inequality; their effectiveness, costs, and political feasibility are genuinely contested

- The racial wealth gap reflects structural historical causes that persist independently of current income differences

The debate about how much inequality is too much, and what tradeoffs are worth making to address it, is genuinely political - it involves value judgments about fairness, freedom, and the purpose of economic systems that empirical research alone cannot resolve.

But the empirical case that inequality has risen, that it has measurable consequences for social welfare and democratic governance, and that it is not simply a reflection of individual merit, is substantially stronger than the public debate often acknowledges.

Sources & Further Reading

- Piketty, T. (2014). Capital in the Twenty-First Century. Harvard University Press.

- Saez, E., & Zucman, G. (2019). The Triumph of Injustice: How the Rich Dodge Taxes and How to Make Them Pay. W. W. Norton.

- Chetty, R., Hendren, N., Kline, P., & Saez, E. (2014). Where Is the Land of Opportunity? The Geography of Intergenerational Mobility in the United States. Quarterly Journal of Economics, 129(4), 1553-1623.

- Rothstein, R. (2017). The Color of Law: A Forgotten History of How Our Government Segregated America. Liveright.

- Wilkinson, R., & Pickett, K. (2009). The Spirit Level: Why More Equal Societies Almost Always Do Better. Allen Lane.

- Goldin, C., & Katz, L. F. (2008). The Race Between Education and Technology. Harvard University Press.

- Gilens, M., & Page, B. I. (2014). Testing Theories of American Politics: Elites, Interest Groups, and Average Citizens. Perspectives on Politics, 12(3), 564-581.

- Corak, M. (2013). Income Inequality, Equality of Opportunity, and Intergenerational Mobility. Journal of Economic Perspectives, 27(3), 79-102.

- Rosen, S. (1981). The Economics of Superstars. American Economic Review, 71(5), 845-858.

- Federal Reserve Board. (2023). Survey of Consumer Finances. View source

- Federal Reserve Board. (2024). Distributional Financial Accounts. View source

- Opportunity Insights. (2024). Data and Research on Economic Mobility. View source

Frequently Asked Questions

What is the Gini coefficient and how is it used to measure inequality?

The Gini coefficient is a summary statistic of inequality ranging from 0 (perfect equality, everyone has the same) to 1 (perfect inequality, one person has everything). It is calculated from the Lorenz curve, which plots cumulative share of income or wealth against the cumulative share of the population. A Gini coefficient of 0.4 for income, for instance, means the income distribution falls notably short of perfect equality. The US wealth Gini is approximately 0.85 - indicating extreme concentration - compared to roughly 0.4-0.5 for income. Wealth is always more concentrated than income.

What is Piketty's r > g thesis?

In Capital in the Twenty-First Century (2013), economist Thomas Piketty argues that when the rate of return on capital ® exceeds the rate of economic growth (g), wealth inequality tends to increase over time. The logic: if capital grows faster than the economy, owners of capital capture a rising share of total income. Piketty argued this was the historical norm, that the mid-20th century period of relatively low inequality was an exception caused by the destruction of capital in two World Wars, and that absent intervention, inequality will continue to rise. Critics dispute aspects of the thesis but it has been highly influential.

What is the difference between wealth inequality and income inequality?

Income inequality refers to the dispersion of annual earnings and other income flows (wages, interest, dividends). Wealth inequality refers to the dispersion of accumulated assets minus liabilities (net worth: real estate, financial assets, retirement accounts, business ownership). Wealth is always more unequally distributed than income because wealth accumulates over time, and returns on existing wealth generate more wealth. In the US, the top 10% of households hold roughly 65-70% of total wealth, while the bottom 50% hold under 3%.

What are the main causes of rising wealth inequality?

Key drivers identified in the research include: rising returns to capital relative to labor (consistent with Piketty’s thesis), growing skill premiums (technology has raised returns to high-skill work faster than low-skill work), the winner-take-most structure of some markets (where top performers capture disproportionate rewards), declines in labor bargaining power (union membership decline, globalization), tax policy changes that reduced top marginal rates and capital gains taxes, and the compounding of initial advantages (wealthy families pass on both financial and social capital). Different researchers emphasize different factors.

Is economic mobility more important to measure than inequality?

Many economists argue that what matters most is not the level of inequality at a point in time but the degree to which individuals and families can move through the distribution over time - economic mobility. A society with high inequality but high mobility might be more fair than one with low inequality but rigid class boundaries. However, research by Raj Chetty and colleagues has found that in the US, economic mobility has declined over recent decades and that high inequality itself impedes mobility, because the gap between rungs of the economic ladder becomes wider and harder to climb.