Understanding: In 1978, a 29-year-old man from Illinois won $400,000 in the state lottery. He quit his job at the factory the same week, bought a new house, invested in a friend's restaurant, and lent money freely to relatives who appeared with plans.

Five years later he was broke, back at the same factory, carrying debt he had not had before he won.

Researchers Philip Brickman, Dan Coates, and Ronnie Janoff-Bulman had actually predicted this: their now-classic 1978 study of lottery winners found that a year after winning, lottery recipients were no happier than a control group, and took less pleasure in everyday activities than they had before.

The windfall had recalibrated their baseline for pleasure without changing the underlying structure of their financial lives.

This is the central paradox of money: it matters enormously, and yet the relationship between money and well-being is far more psychological than most people realize. We inherit beliefs about money we have never examined.

We make financial decisions through the same fast, associative mental machinery that handles threat detection and social comparison.

We think we are acting rationally when we are mostly acting out of habit, fear, and identities formed in childhood. And we routinely make choices that seem entirely sensible in the moment, and that cost us, over decades, vast sums.

The emerging field of behavioral economics, built on the work of Daniel Kahneman, Amos Tversky, Richard Thaler, and a generation of researchers who followed them, has produced a more accurate model of how people actually make financial decisions. It is not flattering.

But understanding it is the necessary foundation for making better ones.

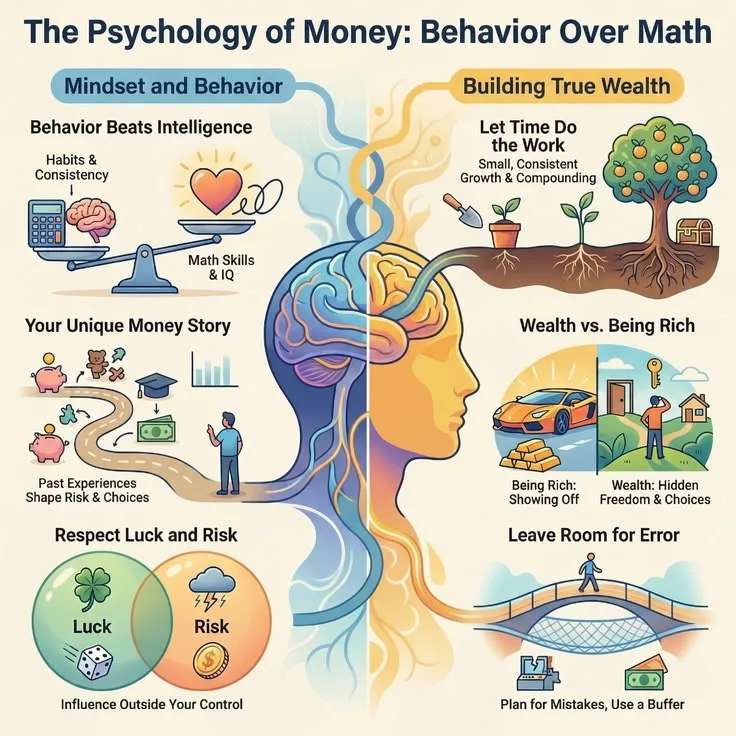

"The premise of this book is that doing well with money has a little to do with how smart you are and a lot to do with how you behave. And behavior is hard to teach, even to really smart people.", Morgan Housel, The Psychology of Money (2020)

Key Definitions

Loss aversion: The psychological tendency, documented by Tversky and Kahneman in their 1979 Prospect Theory paper, for losses to feel roughly twice as painful as equivalent gains feel pleasurable. A $500 loss generates approximately twice the emotional intensity of a $500 gain.

Mental accounting: The cognitive habit, described by economist Richard Thaler, of treating money differently depending on its source, its intended category, or the account it is held in, even though money is entirely fungible.

Treating a tax refund as "free money" while being careful about the same amount from a paycheck is a classic example.

Money scripts: The unconscious beliefs about money formed in childhood and adolescence that drive adult financial behavior. Financial psychologist Brad Klontz and colleagues identified four core patterns in their 2011 taxonomy: money avoidance, money worship, money status, and money vigilance.

Hedonic adaptation: The process by which people return to a relatively stable level of happiness after major positive or negative life events. Brickman's lottery winner research was an early empirical demonstration that the anticipated pleasure of a windfall is not sustained.

Present bias: The tendency to weight immediate rewards more heavily than future ones in ways that are inconsistent with a person's own long-term preferences. The future self feels abstract; the present self's desires feel urgent. This is the primary driver of undersaving for retirement.

Time discounting: The economically rational recognition that money received sooner is worth more than money received later, but humans apply this principle far too aggressively, heavily discounting future rewards even when waiting would clearly be advantageous.

Money Script Patterns and Their Financial Effects

| Money Script | Core Belief | Common Behavior | Financial Risk |

|---|---|---|---|

| Money avoidance | Money is bad; wealthy people are greedy | Sabotage financial success; give away money impulsively | Chronic undersaving; guilt around wealth |

| Money worship | More money will solve all problems | Overwork; sacrifice relationships for income | Never-enough cycle; poor work-life balance |

| Money status | Net worth equals self-worth | Overspend to signal success | High consumer debt; little actual wealth |

| Money vigilance | Always save; never discuss money | Careful saving; extreme frugality | Anxiety; unwillingness to spend even when beneficial |

How We Actually Make Financial Decisions

Daniel Kahneman's decades of research, synthesized in his 2011 book Thinking, Fast and Slow, established the dual-process model of cognition. System 1 is fast, automatic, emotional, and associative. It runs continuously in the background, producing judgments, feelings, and impulses without deliberate effort.

System 2 is slow, deliberate, effortful, and capable of logical reasoning, but it is also cognitively expensive and easily fatigued.

Financial decisions are, in principle, exactly the kind of complex, consequential, multi-variable problems that System 2 was built for. In practice, most financial decisions are made primarily by System 1.

The investor who panic-sells during a market downturn, the consumer who buys a car slightly beyond their budget because it felt right in the showroom, the person who avoids looking at their account balance because the anxiety is too uncomfortable: all are System 1 driving the vehicle while System 2 provides post-hoc justification.

This is not a character flaw. System 1 dominates because it is fast, effortless, and correct often enough in everyday life. The problem is that financial environments, particularly modern investment markets, are precisely the kind of environments where System 1 intuitions are systematically misleading.

Market volatility does not mean danger in the way that a loud noise in the forest means danger. A stock falling in price is not in itself evidence that it should be sold.

But the emotional machinery responds as if these events carry the same threat-signal as physical danger, because that machinery was built long before financial markets existed.

The Behavioral Biases That Cost Real Money

Loss Aversion

Tversky and Kahneman's 1979 paper introducing Prospect Theory is one of the most cited papers in all of economics. Its central finding is that the subjective experience of a loss is roughly twice as intense as the subjective experience of an equivalent gain.

This asymmetry, which they called loss aversion, produces a wide range of irrational financial behaviors.

Investors hold losing positions far too long, because selling crystallizes the loss and forces psychological acknowledgment of failure. They sell winning positions too early, because the fear of giving back gains outweighs the rational expectation of continued returns.

This pattern, documented extensively by Terrance Odean and Brad Barber in their studies of retail investor behavior in the 1990s and 2000s, directly reduces investment returns.

Loss aversion also explains the disposition effect: the well-documented tendency of investors to sell winners and hold losers, exactly the opposite of what tax-efficient and return-maximizing strategies would recommend.

Investors, on average, are more likely to sell a stock that has gone up 20 percent than a stock that has gone down 20 percent, even though the rational consideration is future prospects, not past performance.

Mental Accounting

Richard Thaler, who won the Nobel Prize in Economics in 2017 partly for this work, showed that people do not treat money as the fungible commodity it actually is.

They divide money into mental accounts, entertainment budget, emergency fund, vacation money, "investment" account, and apply different standards of frugality or generosity to each, even though a dollar from any account can be used for anything.

The practical consequences are often destructive. A person maintains $10,000 in a savings account earning minimal interest while carrying $8,000 in credit card debt at 22 percent interest, because the savings account feels like "security" and the debt feels like a separate problem.

The same person receives a $2,000 tax refund and treats it as bonus money to spend freely, even though it is simply their own income returned to them. Mental accounting makes these behaviors feel reasonable. Financially, they are not.

Anchoring

The first number encountered in a financial context exerts a disproportionate influence on subsequent judgments.

Kahneman and Tversky's original anchoring experiments were seemingly absurd, spinning a wheel of fortune and then asking people to estimate the percentage of African countries in the UN, with the wheel's random number affecting their answers, but the effect is robust and very large in financial contexts.

In salary negotiations, the first number stated typically anchors the entire negotiation, whether it was stated by the employer or the candidate. In real estate, listing prices anchor buyer perceptions of value even when buyers consciously know the listing price is strategic.

In investing, the price at which a stock was purchased becomes an anchor that influences whether the investor thinks it is currently over- or undervalued, even though the purchase price is irrelevant to future performance.

The Sunk Cost Fallacy

Economists define a sunk cost as a cost already incurred that cannot be recovered. Rational decision theory says sunk costs should be ignored when making forward-looking decisions, because they cannot affect future outcomes. In practice, people are powerfully influenced by sunk costs.

The classic example is the couple who have paid for non-refundable concert tickets and then learn the concert is going to be unpleasant, but attend anyway because they "already paid." The money is gone regardless of whether they attend. Attending to avoid "wasting" the ticket serves only to waste their time as well.

In financial contexts, sunk cost thinking causes investors to hold declining positions because of what they paid for them, causes businesses to continue failed projects because of prior investment, and causes individuals to continue expensive subscriptions or memberships long past the point of value.

The research consistently shows that explicit awareness of the fallacy does not reliably eliminate it.

Money Scripts: What Childhood Teaches Us About Finance

Financial psychologist Brad Klontz and colleagues published a 2011 study in the Journal of Financial Therapy identifying four patterns of money beliefs, which they called money scripts, that form in childhood and adolescence and continue to drive adult financial behavior, typically outside conscious awareness.

Money avoidance encompasses beliefs that money is bad, that wealthy people are greedy or corrupt, that virtue requires not caring about money, and that having money creates problems.

People with strong money avoidance scripts often self-sabotage financially: unconsciously spending down savings, undercharging for their work, or avoiding financial planning because thinking about money feels uncomfortable or morally compromised.

Money worship encompasses beliefs that more money will solve any problem, that happiness is always just a raise or promotion away, that financial success is the primary measure of worth.

Money worshippers often find that reaching financial goals brings temporary satisfaction followed by the setting of new, higher targets rather than contentment. The goal line moves faster than they can run.

Money status conflates financial worth with personal worth. People operating from this script tie self-esteem to net worth and visible wealth, which produces overspending on status signals (cars, houses, clothes) beyond what brings genuine satisfaction, and deep shame around financial setbacks.

Money vigilance involves excessive caution, secrecy, and anxiety around money. Vigilant individuals are often good savers but may be unable to spend money on their own pleasure even when they can genuinely afford to, and may carry chronic financial anxiety even during periods of objective security.

Klontz's research found these scripts predict specific financial behaviors across large samples, and that they tend to be transmitted intergenerationally, learned more from observation and atmosphere than from explicit teaching.

The family that never discussed money, the parent who expressed contempt for wealthy neighbors, the household that lived in constant financial anxiety: all transmit money scripts that shape the next generation's financial behavior in ways the children never consciously chose.

The Hedonic Treadmill and What Money Cannot Buy

Brickman and Campbell introduced the concept of the hedonic treadmill in 1971 to describe the psychological mechanism by which people rapidly return to a baseline level of well-being after positive or negative life events. Major gains and losses move the baseline temporarily, but people adapt and return to their previous set point.

The lottery winner study Brickman conducted with Coates and Janoff-Bulman in 1978, which surveyed Illinois lottery winners and paraplegic accident victims, found results that were startling at the time: lottery winners were not significantly happier than controls, and paraplegic accident victims were not as unhappy as observers expected them to be.

Both groups had adapted.

This research spawned decades of work on the Easterlin Paradox, named for economist Richard Easterlin who observed in 1974 that as wealthy nations got richer, average self-reported happiness did not reliably increase.

At the individual level, richer people within a society are generally happier than poorer people. But as average incomes rise across the whole society over decades, happiness levels do not track.

More recent work has complicated the picture. Angus Deaton and Kahneman's influential 2010 paper, based on Gallup data from 450,000 Americans, found that day-to-day emotional well-being (positive affect, absence of stress) plateaued around $75,000 annual income, while life evaluation (how satisfied people are with their lives overall) continued rising with income without a clear ceiling.

Matthew Killingsworth's 2021 reanalysis, using experience-sampling data rather than retrospective self-report, found that well-being continued rising steadily with income even above $75,000 for most participants, with a subgroup of unhappy high earners pulling down the average in Deaton and Kahneman's original analysis.

The best current synthesis is probably this: money matters substantially up to the point where material security and life options are established; beyond that, the effect of additional income depends heavily on how it is spent and on whether it reduces the negative experiences (financial stress, time pressure, lack of options) rather than simply increasing consumption.

What Research Shows About How to Spend

Harvard psychology professor Michael Norton, with colleagues including Elizabeth Dunn at the University of British Columbia, has produced a sustained program of research on the relationship between how people spend money and their reported well-being.

Their main findings, summarized in their 2013 book Happy Money, challenge many intuitions.

Spending on experiences, rather than material goods, produces more durable satisfaction for most people. Experiences are harder to adapt to, more strongly tied to social connection and meaning, and better as sources of shared memory and identity.

The new couch becomes background furniture within months; the trip produces stories and connections that persist.

Spending on others, including charitable giving, produces measurably more well-being than spending on oneself in controlled experiments. Norton and colleagues found this effect across income levels and across cultures in a 2008 study published in Science.

Buying time, meaning paying for services that eliminate disliked tasks, produces well-being gains that people systematically underestimate before they do it.

In a 2017 PNAS study, Whillans, Dunn, Smeets, Bekkers, and Norton found that people who used money to buy time reported greater life satisfaction than those who did not, even after controlling for income.

The Knowledge-Behavior Gap

One of the most important findings in the financial literacy literature comes from a 2014 meta-analysis by Fernandes, Lynch, and Netemeyer published in Management Science.

They reviewed 201 prior studies and found that interventions designed to improve financial literacy had only a small effect on financial behaviors, and that the effect decayed substantially over time.

Financial literacy education, in the forms most commonly implemented, explained approximately 0.1 percent of the variance in financial behaviors.

This finding is counterintuitive and important. The instinct behind most personal finance education is that people make poor financial decisions because they lack knowledge.

The evidence suggests the actual drivers of financial behavior are psychological, not informational: unconscious beliefs, emotional responses to money, behavioral habits, and the social environments that reinforce particular patterns of spending and saving.

Morgan Housel's argument in The Psychology of Money (2020) is a popular synthesis of this insight: that financial success is less about spreadsheet competence and more about controlling behavior under pressure, specifically the behavior of not panicking when markets fall, not increasing lifestyle costs in proportion to income, and saving consistently even when it is uncomfortable.

Compound Interest and the Intuition Failure

Albert Einstein reportedly called compound interest "the eighth wonder of the world," and whether or not the attribution is accurate, the sentiment captures a genuine insight about human cognition. The mathematics of exponential growth systematically defeats intuition.

The Rule of 72 is the standard corrective: divide 72 by an annual interest rate to get the approximate number of years required to double a sum. At 7 percent annual return (roughly the historical real return of the US stock market), money doubles every 10 years.

That means $10,000 invested at age 25 becomes approximately $160,000 by age 65, without any additional contributions. $10,000 invested at age 35 becomes $80,000 by 65. The 10-year delay costs $80,000.

These numbers are easy to calculate and essentially impossible to feel. Research consistently shows that people dramatically underestimate the effects of compound growth and, as a consequence, consistently undervalue early saving relative to later saving.

This is partly a cognitive limitation (exponential thinking is not natural) and partly present bias (the future self is abstract).

Time Discounting and the Retirement Problem

The decision to save for retirement is one of the best-studied examples of the gap between what people rationally intend and what they behaviorally do. The future self who will need retirement income feels like a stranger.

The present self can find many compelling reasons to defer saving: pay off debt first, wait until earning more, start properly next year.

Shlomo Benartzi and Richard Thaler, in their 2004 paper "Save More Tomorrow," designed an intervention that addressed this directly.

Rather than asking workers to reduce their current income by increasing retirement contributions, the program committed workers to directing future raises toward increased contributions, phased in automatically.

The result was dramatic: participants in Save More Tomorrow programs increased their savings rates substantially over time with very little conscious effort, because the program worked with present bias rather than against it. A version of this program has since been implemented for millions of workers in the United States.

The lesson is not purely about retirement. It is about the broader principle that financial behavior change is more achievable when it is structural, default-based, and requires minimal active effort, rather than requiring continuous acts of will against the grain of psychological tendencies.

John Bogle and the Question of "Enough"

John Bogle, the founder of Vanguard and inventor of the index fund, wrote a short book in 2008 titled Enough: True Measures of Money, Business, and Life.

The book opens with an anecdote: at a party, Kurt Vonnegut tells Joseph Heller that their wealthy host, a hedge fund manager, made more money in a single day than Heller earned from Catch-22 in its entire history. Heller replies: "Yes, but I have something he will never have: enough."

Bogle's argument is that much of the dysfunction in financial behavior, individual and institutional, stems from the absence of any concept of sufficiency. Without a clear, examined sense of how much is enough, the pursuit of more is self-perpetuating and never arrives anywhere satisfying.

Materialism research by Russell Belk, developing his materialism scale through the 1980s, found that higher materialism (valuing possessions, prioritizing acquisition) consistently correlates with lower life satisfaction, more anxiety, and worse relationships, not because money itself is corrosive but because a person organized around its pursuit typically subordinates other sources of meaning in the process.

The practical question "how much is enough for me?" is one that most people have genuinely never answered. Answering it, with specificity, is one of the most valuable financial planning exercises available, and it is almost entirely psychological rather than mathematical.

Practical Takeaways

Examine your money scripts. The financial behaviors that feel most automatic and most irrational are usually driven by childhood-formed beliefs that have never been examined. Identifying which of Klontz's four patterns resonates most strongly is the starting point.

Financial therapy, distinct from financial planning, exists specifically to address these patterns.

Automate the high-value behaviors. Because present bias, inertia, and cognitive fatigue all work against consistent financial discipline, automating saving, investing, and debt repayment removes the decision from the realm of willpower. What happens automatically tends to happen.

Separate the mental accounts. If you are carrying high-interest debt while also maintaining a large cash "emergency fund," the mental accounting feels protective but the mathematics is destructive. Examine each financial decision as if all your money were in one pool.

Plan for loss aversion. Before investing, write down explicitly what you will do if the investment drops 20, 30, or 40 percent. Then commit to it. The investors who outperform consistently are largely distinguished by not panicking and selling during downturns, which requires having decided in advance not to.

Spend on experiences, others, and time. The research on well-being and spending is more consistent than most people realize. A vacation, a gift, or paying to avoid a task you hate reliably produces more lasting satisfaction than an equivalent material purchase.

Define "enough." Specifically, in writing, for your own circumstances. A number. A lifestyle description. A clear image of what financial sufficiency looks like for you. Without that anchor, the pursuit of more has no natural stopping point.

Sources & Further Reading

- Kahneman, D. (2011). Thinking, Fast and Slow. Farrar, Straus and Giroux.

- Tversky, A., & Kahneman, D. (1979). "Prospect theory: An analysis of decision under risk". Econometrica, 47(2), 263–291.

- Thaler, R. H. (1999). Mental accounting matters. Journal of Behavioral Decision Making, 12(3), 183–206.

- Klontz, B., Britt, S. L., Mentzer, J., & Klontz, T. (2011). Money beliefs and financial behaviors: Development of the Klontz Money Script Inventory. Journal of Financial Therapy, 2(1), 1–22.

- Brickman, P., Coates, D., & Janoff-Bulman, R. (1978). Lottery winners and accident victims: Is happiness relative? Journal of Personality and Social Psychology, 36(8), 917–927.

- Housel, M. (2020). The Psychology of Money. Harriman House.

- Fernandes, D., Lynch, J. G., & Netemeyer, R. G. (2014). Financial literacy, financial education, and downstream financial behaviors. Management Science, 60(8), 1861–1883.

- Kahneman, D., & Deaton, A. (2010). "High income improves evaluation of life but not emotional well-being". Proceedings of the National Academy of Sciences, 107(38), 16489–16493.

- Benartzi, S., & Thaler, R. H. (2004). Save More Tomorrow: Using behavioral economics to increase employee saving. Journal of Political Economy, 112(S1), S164–S187.

- Dunn, E. W., Aknin, L. B., & Norton, M. I. (2008). "Spending money on others promotes happiness". Science, 319(5870), 1687–1688.

- Bogle, J. C. (2008). Enough: True Measures of Money, Business, and Life. Wiley.

- Killingsworth, M. A. (2021). Experienced well-being rises with income, even above $75,000 per year. Proceedings of the National Academy of Sciences, 118(4), e2016976118.

Related reading: how to make better decisions, common decision traps, how to think more critically

Frequently Asked Questions

Why don't people make rational financial decisions?

Because financial decisions are not made by the rational calculator economists once assumed. They are made by human beings whose cognitive systems evolved for a very different environment, and who bring emotional histories, social comparisons, unconscious scripts, and systematic biases to every money choice they make. Daniel Kahneman’s research on System 1 and System 2 thinking shows that most financial decisions are made quickly and automatically by the same emotional, associative processes that handle pattern recognition, not by the deliberate reasoning system we assume is in charge. Loss aversion, anchoring, the availability heuristic, and mental accounting all distort financial behavior in predictable ways that have nothing to do with intelligence.

What are money scripts and how do they affect behavior?

Money scripts are the often unconscious beliefs about money that were formed in childhood and adolescence and that continue to drive financial behavior in adulthood. Financial psychologist Brad Klontz and colleagues identified four core money script patterns in a 2011 study: money avoidance (money is bad or corrupting), money worship (more money will solve my problems), money status (my net worth equals my self-worth), and money vigilance (financial caution is always virtuous). Each pattern produces distinct financial behaviors, some adaptive and some deeply destructive, and most people are unaware of which pattern drives them until they examine it directly.

Does more money make you happier?

The relationship is real but complicated. Richard Easterlin’s paradox, first identified in 1974, showed that within wealthy nations, increases in national income do not reliably increase average happiness, even though richer individuals within a society tend to be happier than poorer ones. A widely cited 2010 study by Kahneman and Deaton found emotional well-being plateaus around $75,000 annual income in the United States, though a 2021 reanalysis by Matthew Killingsworth found continued gains at higher incomes for most people. The picture that emerges is that money matters substantially up to the point where basic needs and security are met, that relative income and social comparison play a large role, and that how you spend money matters as much as how much you have.

Why is compound interest so hard to intuitively grasp?

Human brains are wired to think about change linearly, not exponentially. We can easily picture a quantity growing by the same amount each year, but exponential growth, where the rate of increase itself increases over time, consistently defeats intuition. This is why the Rule of 72 (dividing 72 by an interest rate gives the approximate years to double) is such a useful corrective: it translates exponential math into a concrete, graspable number. The practical consequence of this cognitive limitation is that people systematically underestimate how much early savings matter and overestimate how much they can catch up through saving more later.

What financial behaviors have the biggest impact on long-term wealth?

Morgan Housel’s central argument in The Psychology of Money is that behavior matters more than financial knowledge. Specifically: saving rate (how much you save relative to income, consistently over time) is the most powerful variable, because it drives how long compound growth has to work. Avoiding catastrophic decisions, particularly selling assets during market downturns due to panic, preserves the gains that patience builds. Starting early matters enormously because of compound growth’s exponential nature. And avoiding lifestyle inflation, where spending rises automatically with income, is one of the hardest behavioral challenges. Financial literacy has a disappointingly small direct effect on outcomes, as Fernandes and colleagues’ 2014 meta-analysis showed.

How do emotions affect investment decisions?

Substantially and mostly negatively. Loss aversion, identified by Amos Tversky and Daniel Kahneman in their 1979 Prospect Theory paper, means that losses feel roughly twice as painful as equivalent gains feel pleasurable. This asymmetry produces irrational risk-aversion in investment contexts: investors hold losing positions too long (to avoid realizing a loss) and sell winning positions too early (to lock in a gain before it disappears). Anxiety during market volatility activates the same threat-response system that evolved for physical danger, which produces powerful urges to act, specifically to sell, at precisely the moments when doing nothing is usually the correct strategy.

What does behavioral economics say about saving for retirement?

Research shows that automatic enrollment in retirement plans dramatically increases participation compared to opt-in systems, a finding that drove the Pension Protection Act of 2006 in the United States and that Thaler and Sunstein used as a central example in Nudge. The present bias, where the future self feels abstract and the present self’s desires feel urgent, makes voluntary long-term saving psychologically difficult. Shlomo Benartzi and Thaler’s Save More Tomorrow program, which commits workers to directing future pay raises toward retirement savings rather than reducing current take-home pay, produced large increases in savings rates precisely because it worked with present bias rather than against it.