In the autumn of 1929, the New York Stock Exchange collapsed, initiating a cascade of bank failures, credit contraction, and mass unemployment that left a quarter of the American labor force without work by 1933. The Great Depression did not merely produce suffering; it produced a crisis of economic theory.

The prevailing view held that market economies were fundamentally self-correcting, that recessions were temporary dislocations that would resolve themselves as prices and wages adjusted.

The Depression refused to cooperate. It persisted for years, and the elegant theoretical models that said it should not could not explain why.

John Maynard Keynes wrote 'The General Theory of Employment, Interest and Money' (1936) in direct response to this failure.

The book argued that economies could become trapped at high unemployment equilibria, that aggregate demand, the total spending in an economy, was the essential variable, and that government intervention was not only permissible but sometimes necessary to restore economic health.

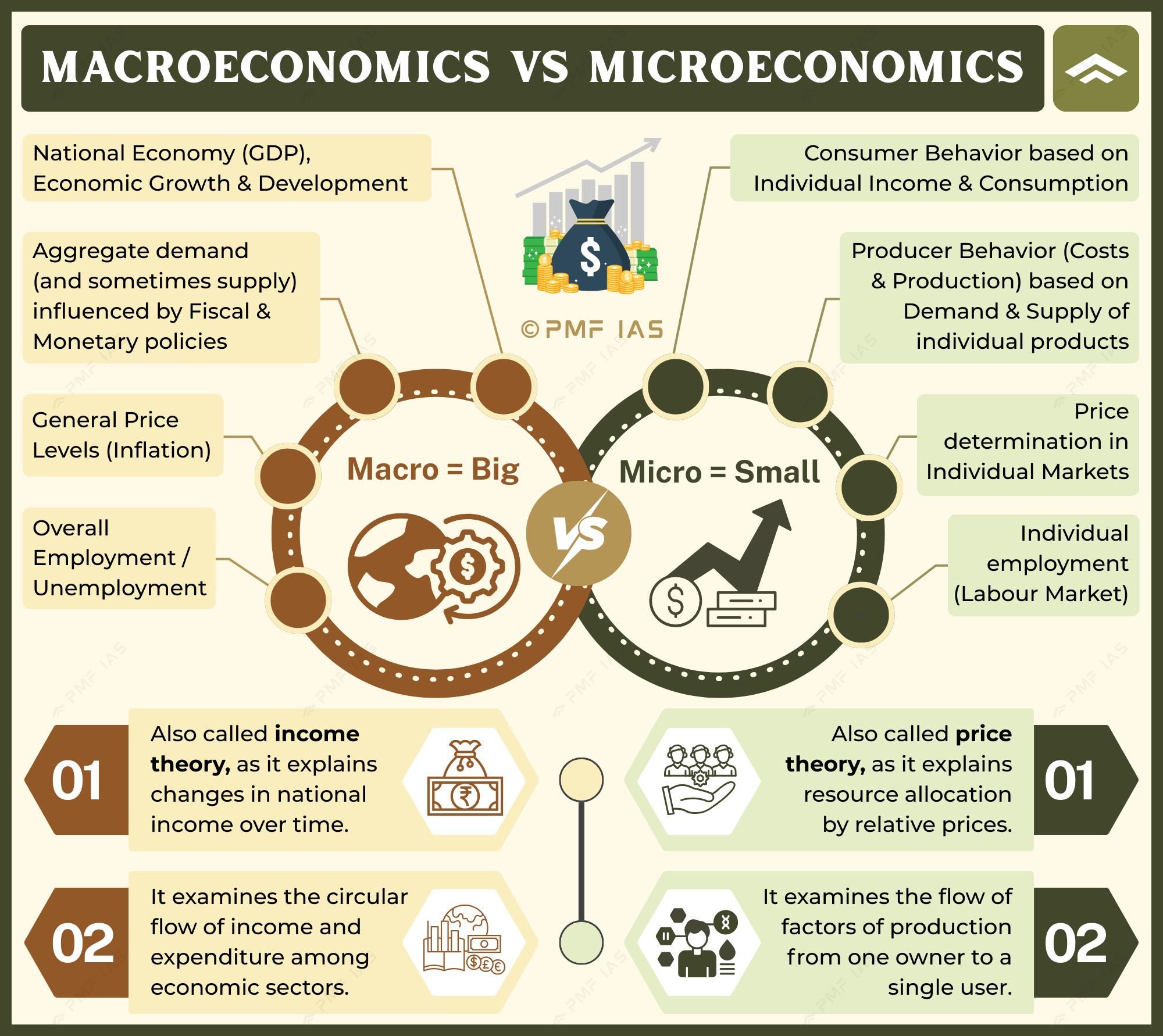

In doing so, Keynes effectively founded macroeconomics as a distinct analytical discipline, separating the study of aggregate economic behavior from the microeconomic analysis of individual markets.

Macroeconomics has grown enormously since Keynes. It encompasses the measurement of national output, the analysis of business cycles, theories of inflation, the operation of monetary and fiscal policy, and the architecture of the international monetary system.

It is also one of the most contested fields in social science, riven by disagreements that are not merely technical but reflect deep differences about how markets function, how people form expectations, and what governments can and cannot accomplish.

Understanding these debates is inseparable from understanding the economies in which we live.

"The ideas of economists and political philosophers, both when they are right and when they are wrong, are more powerful than is commonly understood. Indeed, the world is ruled by little else.", John Maynard Keynes, The General Theory, 1936

Key Definitions

Gross Domestic Product (GDP): The total monetary value of all final goods and services produced within a country's borders in a given period. The standard measurement identity is Y = C + I + G + (X-M), where C is consumption, I is investment, G is government spending, and X-M is net exports.

Recession: A significant, widespread, and prolonged decline in economic activity.

The US National Bureau of Economic Research (NBER) Business Cycle Dating Committee defines recessions holistically across multiple indicators; the popular shorthand of "two consecutive quarters of negative GDP growth" is an approximation, not the official definition.

Fiscal policy: Government decisions about taxation and public spending, used to influence aggregate demand and economic activity.

Monetary policy: Central bank decisions about interest rates and money supply, used to influence borrowing costs, investment, and the price level.

Phillips curve: The proposed empirical relationship between unemployment and inflation, originally described by A.W. Phillips in 1958, positing that lower unemployment is associated with higher inflation. The relationship was complicated by the stagflation of the 1970s and subsequent theoretical revisions.

Major Schools of Macroeconomic Thought

| School | Key figures | Core claim | Policy prescription | Vulnerability |

|---|---|---|---|---|

| Keynesian economics | Keynes (1936); Hicks; Samuelson | Economies can get stuck at high unemployment equilibria; aggregate demand is the key variable | Fiscal stimulus in recessions; government as spender of last resort | May crowd out private investment; political difficulty of deficit reduction in good times |

| Monetarism | Milton Friedman; Phelps | Money supply growth determines inflation in the long run; government fiscal intervention has limited real effects | Steady, predictable money supply growth; rule-based rather than discretionary policy | Controlling money supply technically difficult; financial innovation destabilizes money demand |

| New Classical / RBC | Lucas; Kydland; Prescott | Agents form rational expectations; markets clear continuously; business cycles reflect real supply shocks | Minimal intervention; stabilization policy is counterproductive or ineffective | Cannot explain deep recessions, unemployment persistence, or financial crisis dynamics |

| New Keynesian | Mankiw; Romer; Woodford | Sticky prices and wages justify stabilization policy; rational expectations incorporated | Inflation targeting; countercyclical monetary policy; fiscal multipliers in deep recessions | Model of household and firm behavior may miss financial frictions |

| Post-Keynesian / Minsky | Minsky; Godley; Lavoie | Financial fragility is endogenous; stability breeds instability; effective demand drives output | Financial regulation; functional finance; automatic stabilizers | Less formal modeling; policy prescriptions sometimes unclear |

| MMT | Mosler; Wray; Kelton | Currency-issuing governments cannot run out of money; fiscal constraint is inflation, not solvency | Deficit spending to full employment; taxes to control inflation, not fund spending | Contested empirically; critics argue it underestimates inflation risk; 2021–22 inflation used as challenge |

The Birth of Macroeconomics

Keynes and Aggregate Demand

Before Keynes, the dominant framework in economics was what he termed "classical economics", broadly, the view that flexible prices and wages would ensure that supply creates its own demand (Say's Law) and that full employment would prevail in the long run.

Keynes's critical insight was that this long-run story was inadequate: in his memorable phrase, "in the long run we are all dead." In the short run, nominal wages are often sticky downward, workers resist wage cuts, and coordinating across an entire economy to achieve simultaneous wage reductions is practically impossible.

When demand collapses, the result is unemployment, not the rapid wage adjustment that classical theory predicted.

Keynes introduced the concept of aggregate demand, the total spending in an economy on final goods and services, as the proximate determinant of output and employment.

The fundamental components of aggregate demand, which he analyzed in detail, were consumption (driven by the "propensity to consume"), investment (driven by the "marginal efficiency of capital" and, crucially, by "animal spirits", the irreducible uncertainty and sentiment that governs investment decisions), and government spending.

If private demand collapsed, government could substitute for it directly.

The IS-LM model, developed by John Hicks in 1937 to formalize Keynes's framework, became the workhorse of Keynesian macroeconomics.

The IS curve represents combinations of interest rates and income at which the goods market is in equilibrium (investment equals saving); the LM curve represents combinations at which the money market is in equilibrium.

Together they determine the equilibrium interest rate and income level. The model provided a rigorous framework for analyzing fiscal and monetary policy and remained central to macroeconomic teaching for decades.

Measuring the Economy: The Development of GDP

Aggregate demand analysis required aggregate measurement. Simon Kuznets, a Ukrainian-American economist working at the National Bureau of Economic Research, developed the system of national income accounts in the 1930s at the request of the US Congress, which needed to understand the scale of the Depression.

Kuznets estimated national income from 1929 to 1932, providing the first systematic picture of the US economy's collapse. He received the Nobel Prize in Economic Sciences in 1971 for this work.

GDP, as refined subsequently, measures the total value of final production, goods and services sold to end users, within a country's borders during a period. Intermediate goods are excluded to avoid double-counting.

The three approaches, expenditure, income, and production, yield the same result in principle because every dollar of spending is someone's income and represents value added.

Nominal GDP reflects both real output and price changes; real GDP removes price changes through a deflator, enabling genuine comparisons of output over time. GDP per capita, dividing by population, provides a rough measure of average living standards.

The Business Cycle: Expansion, Contraction, and Crisis

Anatomy of the Cycle

Economic activity oscillates. Periods of expansion, rising employment, output, and incomes, are followed by downturns, and recovery eventually follows contraction. This recurring pattern, the business cycle, has been studied systematically since the nineteenth century.

The NBER identifies four phases: expansion (rising from trough), peak (the turning point before contraction), contraction or recession (declining activity), and trough (the turning point before recovery).

The Great Moderation, a period running roughly from 1984 to 2007 during which output volatility declined markedly in the United States and other advanced economies, appeared to some observers to signal that policymakers had learned to manage the business cycle effectively.

Federal Reserve Chairman Ben Bernanke gave a celebrated lecture in 2004 attributing the moderation to improved monetary policy, better inventory management, and favorable supply shocks. The 2008 crisis abruptly terminated this narrative.

Minsky and Financial Fragility

Hyman Minsky, an economist at Washington University in St. Louis who spent his career working outside the mainstream, offered a theory of why financial crises were endogenous to capitalism rather than external accidents.

In 'Stabilizing an Unstable Economy' (1986) and earlier papers, Minsky argued that extended periods of economic stability encourage increasing financial risk-taking. Firms and households begin with "hedge" financing, where cash flows cover all obligations.

As confidence grows, they shift toward "speculative" financing, where cash flows cover interest but not principal, requiring continuous refinancing. Finally, in a boom, "Ponzi" financing prevails, where cash flows cannot cover even interest payments and rising asset prices alone sustain debt service.

At this point, any disruption to asset prices triggers cascading defaults, forced asset sales, and financial collapse. The economy's very stability breeds the conditions for its eventual instability, what Paul McCulley, a PIMCO fund manager, labeled a "Minsky moment" in 1998, a phrase widely applied to the 2008 crisis.

Keynesian Economics: Fiscal Policy and Its Critics

The Multiplier and the Paradox of Thrift

A central Keynesian concept is the fiscal multiplier: the proposition that a dollar of government spending produces more than a dollar increase in total output, because the initial recipients of government spending use part of their additional income to spend again, generating further rounds of economic activity.

The size of the multiplier depends on the marginal propensity to consume and on whether the economy has spare capacity. At full employment, additional spending crowds out private investment; in a demand-constrained recession with a zero lower bound on interest rates, the multiplier may be considerably above one.

The paradox of thrift illustrates the fallacy of composition that lies at the heart of macroeconomics: while any individual household is prudent to save more during hard times, if all households simultaneously attempt to save more, aggregate spending falls, income falls, and actual saving may not increase because income has declined.

What is rational individually is destructive collectively. This paradox, which Keynes formalized, explains why market economies can remain stuck in recessions without active demand management.

New Keynesian Economics

From the 1980s, a new synthesis emerged that incorporated Keynesian insights, particularly the non-neutrality of money in the short run and the importance of aggregate demand, into models with explicit microeconomic foundations.

New Keynesian economics, associated with economists including Gregory Mankiw, Olivier Blanchard, Lawrence Ball, and Michael Woodford, emphasizes price and wage stickiness as the fundamental friction that gives monetary policy real effects.

Prices are not continuously re-optimized; firms update their prices infrequently (Calvo pricing, named after Guillermo Calvo, is a common formalization). This stickiness means that monetary policy can affect real variables, not just nominal ones, in the short run.

Michael Woodford's 'Interest and Prices: Foundations of a Theory of Monetary Policy' (2003) provided the theoretical foundations for the New Keynesian approach that underlies inflation targeting at most major central banks.

The book's core message was that the central bank's primary instrument is the short-term nominal interest rate, and that its credibility in maintaining a given inflation target was itself a powerful tool, expectations management, not just the current interest rate, determines macroeconomic outcomes.

Monetarism, the Phillips Curve, and Supply-Side Economics

Friedman, Schwartz, and the Money Supply

Milton Friedman spent his career arguing that monetary policy was more powerful and discretionary fiscal policy less reliable than the Keynesian consensus held.

His most influential empirical contribution, co-authored with Anna Schwartz, was 'A Monetary History of the United States, 1867-1960' (1963), which traced the relationship between the money supply and economic activity over nearly a century.

The book's central argument was that the Great Depression was primarily a monetary phenomenon: the Federal Reserve's failure to prevent a one-third contraction of the money supply between 1929 and 1933, through bank failures and a failure to act as lender of last resort, turned a severe recession into an economic catastrophe.

The appropriate policy response was to maintain stable money growth, not to engage in activist discretionary policy, which Friedman argued was likely to be destabilizing due to policy lags.

Friedman's 1968 presidential address to the American Economic Association introduced the concept of the natural rate of unemployment, the rate consistent with stable inflation once inflationary expectations have fully adjusted, and argued that policymakers could not exploit the Phillips curve trade-off permanently.

Any attempt to hold unemployment below the natural rate would result in accelerating inflation as workers' inflationary expectations rose.

Edmund Phelps, working independently, published the same argument simultaneously in 1968. The stagflation of the 1970s, simultaneous high inflation and high unemployment, appeared to vindicate this analysis and severely damaged the credibility of the simple Keynesian Phillips curve.

Supply-Side Economics

The 1970s economic crisis generated both the monetarist revival and supply-side economics, which emphasized reducing marginal tax rates to stimulate work, saving, and investment.

The Laffer curve, associated with economist Arthur Laffer, who reportedly drew it on a napkin in 1974, depicted the relationship between tax rates and tax revenues, arguing that at sufficiently high rates, tax cuts could increase revenue by expanding the tax base.

This proposition underpinned the Reagan administration's 1981 tax cuts.

The subsequent record was mixed: while the economy recovered from the 1981-82 recession, budget deficits expanded substantially, calling into question the revenue-enhancing claims.

Supply-side economics remains a contested field, with advocates emphasizing growth effects and critics emphasizing distributional consequences and the problematic empirical record.

Modern Macroeconomics and Its Critics

DSGE Models and the Lucas Critique

From the 1980s, macroeconomic modeling was transformed by the rational expectations revolution. Robert Lucas Jr.

argued in his celebrated 1976 critique that historical econometric relationships between policy instruments and outcomes could not be relied upon to predict the effects of policy changes, because rational economic agents would adjust their behavior in response to anticipated policy shifts.

Models needed explicit microfoundations, to derive aggregate behavior from the optimizing choices of households and firms.

This led to Dynamic Stochastic General Equilibrium (DSGE) models, which became the standard tool at central banks and academic macroeconomics departments.

Finn Kydland and Edward Prescott developed real business cycle theory in their 1982 paper 'Time to Build and Aggregate Fluctuations,' arguing that business cycles were optimal responses to technological shocks rather than market failures requiring policy correction.

This approach, combined with Lucas's framework, pushed the mainstream away from Keynesian activism and toward an emphasis on credible rules-based policy. Kydland and Prescott received the Nobel Prize in 2004.

The 2008 Crisis and Heterodox Challenges

The 2008 financial crisis exposed major limitations of the mainstream framework. DSGE models, which largely abstracted from financial sectors and the possibility of systemic collapse, failed to anticipate or adequately analyze the crisis.

Paul Krugman's 2009 essay 'How Did Economists Get It So Wrong?' argued that the profession had been seduced by mathematical elegance into building models that assumed away the most important problems.

The Great Moderation had encouraged complacency; finance had been treated as a veil rather than a potentially catastrophic source of instability.

In the post-crisis environment, several heterodox perspectives gained renewed attention. Modern Monetary Theory, associated with L.

Randall Wray, Stephanie Kelton, and Warren Mosler, argued that sovereign currency issuers face no financial constraint analogous to household budget constraints, and that deficits are appropriate whenever private saving exceeds private investment.

The binding constraint on government spending is inflation, not the availability of financing.

Kelton's 'The Deficit Myth' (2020) brought these arguments to a broad audience.

Larry Summers, in a widely noted 2013 speech, revived Alvin Hansen's 1938 concept of secular stagnation, the argument that advanced economies might face a chronic deficiency of demand driven by demographic change, declining investment opportunities, and rising inequality, keeping equilibrium real interest rates persistently low or negative.

International Macroeconomics

Balance of Payments and Exchange Rates

Open economies are connected to the rest of the world through trade and capital flows, captured in the balance of payments accounts. The current account records trade in goods and services, primary income (investment income), and secondary income (transfers).

The capital and financial accounts record cross-border investment and lending. By accounting identity, a current account deficit must be matched by a capital account surplus: countries that import more than they export must borrow from abroad or sell assets to foreigners.

Exchange rates, the prices at which currencies trade against each other, play a central role in international macroeconomic adjustment.

Flexible exchange rates allow relative prices to adjust without requiring changes in domestic wage and price levels; fixed exchange rates, by contrast, force adjustment through internal price deflation or inflation, which is typically slower and more painful.

The Mundell-Fleming model, extending the IS-LM framework to an open economy, showed that under free capital mobility, fiscal policy has large effects under fixed exchange rates (because the exchange rate is held constant) but limited effects under flexible exchange rates (because currency appreciation crowds out net exports).

Monetary policy has the reverse pattern.

The Impossible Trinity and Global Imbalances

The impossible trinity, that a country cannot simultaneously maintain a fixed exchange rate, free capital mobility, and independent monetary policy, has been a central organizing principle of international monetary economics since Robert Mundell's work in the 1960s.

Countries in the Eurozone accepted loss of monetary autonomy to achieve a common currency. Countries like China long maintained capital controls to preserve both exchange rate management and domestic monetary policy.

The United States floats its exchange rate and maintains open capital markets, allowing independent monetary policy at the cost of exchange rate volatility.

The United States has run persistent current account deficits since the 1980s, financed by capital inflows from countries, particularly China and East Asian economies, that run corresponding surpluses.

This pattern of global imbalances, analyzed extensively by economists including Ben Bernanke, who coined the term "global saving glut" in a 2005 speech, has been both a source of cheap financing for American borrowers and a potential source of vulnerability.

The Triffin dilemma, articulated by Belgian-American economist Robert Triffin in 1960, identified the structural contradiction in the dollar's reserve currency role: the United States must supply dollars to the world economy by running deficits, but persistent deficits eventually undermine confidence in the dollar's stability, creating long-run pressure for reform of the international monetary system.

Sources & Further Reading

Keynes, J.M. (1936). The General Theory of Employment, Interest and Money. Macmillan.

Friedman, M., & Schwartz, A.J. (1963). A Monetary History of the United States, 1867-1960. Princeton University Press.

Hicks, J.R. (1937). Mr. Keynes and the 'Classics': A suggested interpretation. Econometrica, 5(2), 147-159.

Minsky, H.P. (1986). Stabilizing an Unstable Economy. Yale University Press.

Lucas, R.E. (1976). Econometric policy evaluation: A critique. Carnegie-Rochester Conference Series on Public Policy, 1, 19-46.

Kydland, F.E., & Prescott, E.C. (1982). Time to build and aggregate fluctuations. Econometrica, 50(6), 1345-1370.

Woodford, M. (2003). Interest and Prices: Foundations of a Theory of Monetary Policy. Princeton University Press.

Phillips, A.W. (1958). The relation between unemployment and the rate of change of money wage rates in the United Kingdom, 1861-1957. Economica, 25(100), 283-299.

Stiglitz, J.E., Sen, A., & Fitoussi, J.P. (2009). Report by the Commission on the Measurement of Economic Performance and Social Progress. Commission on the Measurement of Economic Performance and Social Progress.

Mundell, R.A. (1963). Capital mobility and stabilization policy under fixed and flexible exchange rates. Canadian Journal of Economics and Political Science, 29(4), 475-485.

Summers, L.H. (2014). U.S. economic prospects: Secular stagnation, hysteresis, and the zero lower bound. Business Economics, 49(2), 65-73.

Krugman, P. (2009, September 6). How did economists get it so wrong? The New York Times Magazine.

Frequently Asked Questions

What is macroeconomics and how is it different from microeconomics?

Macroeconomics is the branch of economics that studies the behavior and performance of an economy as a whole, its aggregate output, employment, price level, and growth over time. Where microeconomics analyzes the decisions of individual households and firms, and how prices in specific markets are determined, macroeconomics asks questions about the economy as a national or global system: Why does output sometimes collapse in recessions? What determines the overall price level and why does it rise? How do government spending and central bank policy affect aggregate employment and income? The distinction is not merely one of scale; the economy in aggregate can behave very differently from the sum of its individual parts. John Maynard Keynes established this with particular force during the Great Depression: the paradox of thrift shows that individual households acting rationally by saving more during hard times collectively reduce demand and make the downturn worse, a fallacy of composition that only macroeconomic analysis can diagnose. Modern macroeconomics originated substantially with Keynes’s ‘The General Theory of Employment, Interest and Money’ (1936), which argued that market economies were not self-correcting and could become trapped at high unemployment equilibria, requiring government intervention to restore aggregate demand. Since Keynes, the field has developed a rich set of analytical frameworks, national income accounting, monetary models, open-economy models, dynamic stochastic general equilibrium models, each designed to illuminate different aspects of aggregate economic behavior. The field remains deeply contested, with major schools disagreeing on questions ranging from the size of fiscal multipliers to the fundamental causes of the 2008 financial crisis.

How is GDP measured and what are its limitations?

Gross Domestic Product (GDP) is the monetary value of all final goods and services produced within a country’s borders in a given period, typically one year or one quarter. The expenditure approach, most commonly used, sums four components: consumer spending ©, investment (I), government expenditure (G), and net exports, which is exports minus imports (X-M), giving the identity Y = C + I + G + (X-M). The income approach sums all incomes earned in production, wages, profits, rents, interest. The production (or value-added) approach sums the value added at each stage of production. In principle, all three approaches yield the same figure. Real GDP adjusts for inflation using a price deflator, allowing genuine output comparisons over time; nominal GDP reflects both output changes and price changes. Simon Kuznets, who developed the national income accounting framework in the 1930s at the request of the US Congress (receiving the Nobel Prize in Economics in 1971), warned from the outset that welfare could not be inferred from national income figures. GDP has numerous well-documented limitations. It excludes unpaid work, domestic labor, caregiving, volunteering, which is substantial in any economy and disproportionately performed by women. It includes activity that represents social costs rather than benefits: military expenditure, pollution cleanup, incarceration. It is insensitive to distribution; a country with GDP identical to another may have dramatically more or less equality. Senator Robert Kennedy articulated this eloquently in a 1968 speech, noting that GDP measured nearly everything except what makes life worthwhile. Alternatives and supplements have been proposed: the Human Development Index (HDI), developed by Amartya Sen and Mahbub ul Haq; Bhutan’s Gross National Happiness framework; and the Stiglitz-Sen-Fitoussi Commission report of 2009, commissioned by French President Sarkozy, which recommended a dashboard of indicators to complement GDP.

What causes recessions and how are they officially measured?

A recession is a significant, widespread, and prolonged downturn in economic activity. The popular definition, two consecutive quarters of negative real GDP growth, is a useful heuristic but is not the official standard in the United States, where the National Bureau of Economic Research (NBER) Business Cycle Dating Committee makes formal determinations. The NBER uses a holistic approach, examining a range of monthly indicators including employment, real personal income, industrial production, and real wholesale-retail sales, placing more weight on depth and breadth of decline than on strict quarterly GDP figures. The 2020 US recession, for example, was officially dated from February to April 2020, just two months, because the decline was so severe, even though it did not meet the two-quarter criterion. Recessions have multiple potential causes. Demand shocks, sudden falls in consumer or investment spending, reduce aggregate output and employment; the canonical Keynesian story emphasizes coordination failures and self-reinforcing demand collapses. Supply shocks, sharp increases in input costs, particularly energy, reduce productive capacity; the oil price shocks of 1973 and 1979 triggered recessions across advanced economies. Financial crises, in which credit channels collapse, are particularly severe because they simultaneously reduce both investment demand and the capacity to finance consumption. Hyman Minsky, in ‘Stabilizing an Unstable Economy’ (1986), argued that financial stability itself breeds fragility: extended periods of prosperity encourage increasing risk-taking and leverage, until a moment of credit stress triggers cascading deleveraging, what Paul McCulley later termed a ‘Minsky moment,’ a phrase that gained wide currency after the 2008 financial crisis.

What is Keynesian economics and does the fiscal multiplier work?

Keynesian economics, derived from the theoretical framework of John Maynard Keynes’s ‘The General Theory’ (1936), holds that aggregate demand, the total spending in an economy, is the primary determinant of output and employment in the short run, and that markets left to themselves can settle at equilibria with high unemployment. The core Keynesian policy prescription is fiscal stimulus: in a recession, governments should increase spending or cut taxes to boost aggregate demand directly, filling the gap left by collapsed private spending. The multiplier concept holds that each dollar of government spending generates more than one dollar of economic activity, because the initial recipients spend a fraction of the additional income, creating further rounds of spending. The size of this multiplier has been intensely debated. Christina Romer and David Romer, examining historical US fiscal episodes, estimated multipliers above 3; Roberto Perotti and Alberto Alesina, examining fiscal consolidations, found smaller or negative multipliers in open economies. The IMF, in a landmark 2012 World Economic Outlook admission, acknowledged it had substantially underestimated fiscal multipliers during the post-2010 austerity period in advanced economies, contributing to forecasting errors. The liquidity trap, a situation in which monetary policy becomes ineffective because nominal interest rates cannot fall below zero (zero lower bound) and expectations of deflation prevail, is central to Keynesian analysis of episodes like the Great Depression and the post-2008 environment. New Keynesian economics, developed from the 1980s onward by economists including Gregory Mankiw, Olivier Blanchard, and Michael Woodford, incorporates price and wage rigidities into microfounded dynamic models, producing frameworks widely used at central banks. Woodford’s ‘Interest and Prices’ (2003) is a foundational New Keynesian text.

What is monetarism and what did Milton Friedman argue about the Great Depression?

Monetarism is the school of economic thought, most closely associated with Milton Friedman, that emphasizes the primacy of the money supply in determining nominal income and, over longer periods, the price level. Friedman’s central policy prescription was simple: the central bank should grow the money supply at a stable, moderate rate, rather than attempting to fine-tune the economy through discretionary policy. In ‘A Monetary History of the United States, 1867-1960’ (1963), co-authored with Anna Schwartz, Friedman and Schwartz argued that the Great Depression was not, as the prevailing Keynesian narrative held, a spontaneous collapse of private demand but rather a catastrophic policy failure: the Federal Reserve allowed the money supply to contract by roughly one-third between 1929 and 1933, turning what might have been an ordinary recession into a catastrophe. The argument had profound implications for how the Depression was understood and for how policy was conducted subsequently; Ben Bernanke, upon Friedman’s ninetieth birthday in 2002, said on behalf of the Fed: ‘We won’t do it again.’ Friedman also challenged the Phillips curve, the supposed trade-off between inflation and unemployment posited by A.W. Phillips in 1958, arguing in his 1968 American Economic Association presidential address that the trade-off was illusory in the long run. Any attempt to hold unemployment below its ‘natural rate’ would simply result in accelerating inflation as workers revised their inflationary expectations upward. Edmund Phelps independently arrived at the same argument, and the stagflation of the 1970s, simultaneously high inflation and high unemployment, appeared to confirm it, substantially discrediting simple Keynesian demand management and elevating monetarism and rational expectations approaches.

How did the 2008 financial crisis challenge mainstream macroeconomics?

The 2008 global financial crisis represented a severe failure not only of financial regulation but of mainstream macroeconomic theory. The dominant framework in central banks and academic departments in the years preceding the crisis was the Dynamic Stochastic General Equilibrium (DSGE) model, incorporating rational expectations and microfounded behavior. These models largely abstracted from the financial sector and from the possibility of systemic financial collapse, treating credit market disruptions as second-order. Robert Lucas Jr. had argued in his 1976 ‘Lucas critique’ that historical econometric relationships break down when policies change, because rational agents adjust their behavior in response to anticipated policy changes; this led to the construction of theory-grounded models that also, paradoxically, had limited capacity to model financial crises. Paul Krugman, in a widely read 2009 New York Times Magazine essay ‘How Did Economists Get It So Wrong?’, argued that the economics profession had mistaken mathematical elegance for insight, and had allowed the stability of the Great Moderation, the period from roughly 1984 to 2007 characterized by declining output volatility in advanced economies, to induce complacency about systemic risk. In the aftermath, several heterodox perspectives received renewed attention. Minsky’s financial instability hypothesis gained wide citation. Modern Monetary Theory (MMT), associated with Stephanie Kelton, Warren Mosler, and Randall Wray, argued that currency-issuing governments face no financial constraint in the same sense that households do, and that the relevant constraint on spending is inflation rather than deficit levels. Larry Summers revived Alvin Hansen’s 1938 concept of secular stagnation in 2013, arguing that advanced economies faced a chronic shortfall of demand that could keep interest rates near zero for extended periods, limiting the effectiveness of conventional monetary policy.

What is the impossible trinity in international macroeconomics?

The impossible trinity, also called the trilemma, is a foundational principle of international macroeconomics, developed by Robert Mundell and Marcus Fleming in the 1960s. It holds that a country cannot simultaneously maintain all three of: a fixed exchange rate, free movement of capital across borders, and independent monetary policy (the ability to set domestic interest rates to manage the domestic economy). Only two of the three are achievable at once. The logic is straightforward: if a country fixes its exchange rate and allows free capital flows, then any attempt to set an interest rate different from the international rate will trigger capital flows that undermine the exchange rate peg. To maintain the peg, the central bank must accept the interest rate dictated by international markets, sacrificing monetary autonomy. Different countries have made different choices along this trilemma: the Eurozone countries gave up monetary autonomy in exchange for fixed exchange rates (a common currency) and open capital markets; China maintained significant capital controls for many years to preserve both a managed exchange rate and domestic monetary policy independence; countries like the United Kingdom and the United States float their exchange rates, allowing independent monetary policy with free capital flows. The trilemma helps explain several international financial crises, including the 1997 Asian financial crisis, in which several countries had attempted to maintain fixed exchange rates against the dollar while liberalizing capital accounts, leaving them vulnerable to speculative attack. The related Triffin dilemma, articulated by economist Robert Triffin in 1960, identifies a structural tension in having the US dollar serve as the world’s reserve currency: the US must run persistent current account deficits to supply enough dollars to the rest of the world, but doing so eventually undermines confidence in the dollar’s value.