Commerce: When Amazon launched in 1995 as an online bookstore, it processed its first sale, Douglas Hofstadter's 'Fluid Concepts and Creative Analogies', in the founding team's garage.

Three decades later, global e-commerce generates approximately $6.9 trillion in annual sales, represents 22% of all retail spending worldwide, and has fundamentally restructured the supply chains, real estate portfolios, labor markets, and consumer expectations of every major economy.

The market did not merely grow, it transformed the architecture of commerce itself.

The data in 2026 shows an industry that has matured from pandemic-era hysteria (27% growth in 2020 is not a sustainable trajectory, and the industry knew it) into something more durable: a structural component of global retail that continues to gain share year after year, even as the explosive growth rates normalize.

Mobile has taken over, accounting for nearly three-quarters of all e-commerce transactions globally. Social commerce, buying directly through TikTok, Instagram, and WeChat, is the fastest-growing segment by far, with global social commerce sales projected to exceed $1.3 trillion in 2026.

This article compiles the most current, authoritative statistics on market size, platform shares, consumer behavior, conversion benchmarks, and the structural trends reshaping the industry. The numbers draw primarily from eMarketer, Statista, the US Census Bureau, Baymard Institute, and Shopify's merchant data.

"We have moved from a world where e-commerce was a channel to a world where commerce is increasingly digital by default.

The question for retailers is no longer 'do we need to be online?' It is 'what role does physical presence play in a primarily digital purchase journey?'", Harley Finkelstein, President of Shopify, 2025

Key Definitions

E-Commerce: The buying and selling of goods and services over the internet. Includes business-to-consumer (B2C), business-to-business (B2B), consumer-to-consumer (C2C), and direct-to-consumer (DTC) transactions. Statistics in this article primarily reference B2C retail unless otherwise noted.

Mobile Commerce (M-Commerce): E-commerce transactions conducted via smartphone or tablet. Typically measured separately from desktop/laptop commerce due to significant behavioral and conversion rate differences.

Social Commerce: E-commerce transactions initiated and often completed entirely within social media platforms, without navigating to a separate retailer website. Distinct from social media advertising, which drives traffic to external sites.

Gross Merchandise Value (GMV): The total value of goods sold through a marketplace or platform, including the seller's revenue. Used by Amazon, eBay, Shopify, and most marketplace platforms to report business scale. Distinct from a platform's own revenue, which reflects only fees and commissions.

Conversion Rate: The percentage of website visitors who complete a desired action, typically a purchase. The single most scrutinized metric in e-commerce optimization. Small changes in conversion rate have outsized revenue impact at scale.

Global Market Size and Regional Breakdown

Global e-commerce retail sales are projected to reach approximately $6.9 trillion in 2026, per eMarketer's forecast model. This represents a compound annual growth rate of approximately 9% since 2022, a significant deceleration from the 27% surge of 2020 but roughly double pre-pandemic growth rates of 4-6% annually.

The pandemic permanently accelerated e-commerce penetration, estimates suggest the COVID-19 period compressed approximately 5-7 years of typical e-commerce adoption into 18 months.

Asia-Pacific dominates global e-commerce, accounting for approximately 60% of total sales.

China alone represents approximately 52% of global e-commerce, a staggering concentration driven by Alibaba's Taobao/Tmall ecosystem, JD.com, and the extraordinary digital commerce infrastructure built into WeChat, Douyin, and Meituan.

China's online retail penetration rate exceeds 52% of total retail, the highest of any major economy.

The United States is the second-largest e-commerce market at approximately $1.2 trillion in 2025, per US Census Bureau quarterly e-commerce reports. US e-commerce represents approximately 16% of total retail sales, a share that has grown steadily for a decade.

Western Europe collectively represents approximately $700 billion, with the UK, Germany, and France as the largest individual markets.

Emerging e-commerce markets showing the fastest growth rates include India ($150 billion in 2025, growing approximately 22% per year), Southeast Asia ($250 billion collectively, led by Indonesia and Vietnam), and Latin America ($175 billion, with Brazil and Mexico dominant).

Africa's e-commerce market, while still small in absolute terms, is growing at approximately 35% annually, primarily via mobile-first markets in Nigeria, Kenya, and South Africa.

Platform Market Share

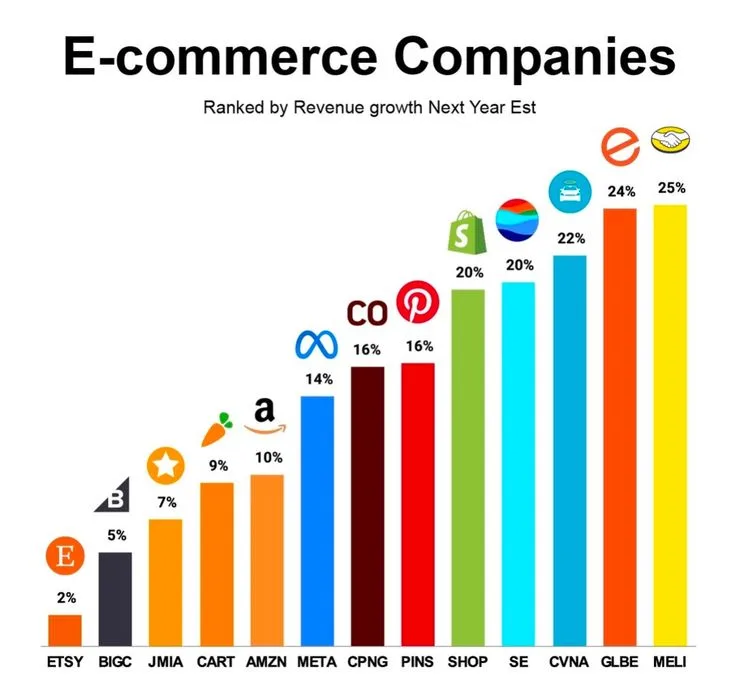

Amazon's e-commerce dominance in the United States is substantial. Amazon commands approximately 40% of all US e-commerce sales, per eMarketer data, a market share that has been remarkably stable over the past several years despite intensifying competition.

Amazon's marketplace model (where third-party sellers account for approximately 60% of units sold, per Amazon's own reports) makes it simultaneously the largest e-commerce retailer and the largest e-commerce platform enabling other retailers.

Walmart has emerged as a credible second-place competitor in US e-commerce, with approximately 7% market share.

Walmart's strategy of leveraging its 4,700+ US stores as fulfillment nodes has allowed it to compete effectively on delivery speed and grocery e-commerce, where it has outgrown Amazon in several categories. Apple, eBay, and Target each hold approximately 3-4% of US e-commerce market share.

Shopify deserves special consideration. With approximately 10% of US e-commerce flowing through its platform as of 2025, Shopify is both a major platform and an invisible infrastructure layer, its merchants appear under their own brands, making Shopify's collective footprint underestimated in standard market share analyses.

In China, Alibaba's Taobao/Tmall combination holds approximately 47% market share (down from 70%+ five years ago), followed by JD.com at 18% and Pinduoduo/Temu at 16%. Douyin (TikTok's Chinese version) has grown to approximately 10% share, entirely through social commerce.

The Chinese market's fragmentation is an important signal: even China's most dominant player is losing ground to social and livestream commerce competitors.

Globally, Amazon, Alibaba, and JD.com collectively account for approximately 45% of all e-commerce revenue. The long tail of independent retailers, niche platforms, and direct-to-consumer brands accounts for the remaining 55%.

Mobile Commerce Deep Dive

Mobile's dominance of e-commerce transaction volume is the defining structural fact of the industry in 2026. Globally, 73% of all e-commerce transactions by count are initiated on mobile devices, though mobile accounts for approximately 62% of e-commerce revenue due to higher average order values on desktop.

The mobile-desktop gap in conversion rate remains persistent and significant. Baymard Institute's benchmarks show desktop conversion rates averaging 3.65% versus mobile rates of approximately 2.1%, a roughly 42% gap.

This reflects a combination of factors: checkout friction on mobile (small keyboard inputs, security concerns, credit card numbers), comparison shopping behavior (consumers browse on mobile, purchase on desktop), and screen size limitations for complex product evaluations.

The markets with highest mobile commerce penetration are almost entirely in Asia and Africa, where mobile-first internet access is the norm. India's mobile commerce share exceeds 85% of all online purchases, with consumers who never used desktop internet now transacting entirely via smartphone.

Indonesia, Vietnam, Nigeria, and Kenya show similarly high mobile-first patterns.

In the US and Europe, mobile's share varies by category. Fast fashion (SHEIN, H&M's app, fast-fashion competitors) shows mobile rates exceeding 85%. Grocery delivery (Instacart, DoorDash, Walmart Grocery) is almost entirely mobile. High-ticket electronics, automotive parts, and B2B e-commerce remain disproportionately desktop.

Apple Pay, Google Pay, and 'buy now, pay later' (BNPL) services like Afterpay, Klarna, and Affirm have collectively reduced mobile checkout friction and improved mobile conversion rates.

Data from Shopify merchants shows that orders using one-click payment methods (Apple Pay, Shop Pay) convert at approximately 1.7x the rate of orders using standard credit card entry on mobile.

Cart Abandonment: The $18 Trillion Opportunity

The Baymard Institute's meta-analysis of 49 cart abandonment studies, widely considered the gold standard source, puts the global average cart abandonment rate at 70.19% as of 2025.

Applied to the $6.9 trillion global e-commerce market, and accounting for the fact that cart abandonment research typically focuses on 'abandonment by shoppers who show intent to purchase,' this implies a theoretical recoverable opportunity of extraordinary scale.

The reasons for cart abandonment are well-documented. In Baymard's 2025 US user research survey, the top reasons included: unexpected costs (shipping, taxes, fees), cited by 48% of abandoners; requirement to create an account, 26%; complex checkout process, 22%; inability to trust the site with payment information, 17%; and estimated delivery time too long, 16%.

Critically, Baymard distinguishes between 'necessary' abandonment (shoppers who were browsing, not ready to purchase) and 'recoverable' abandonment (shoppers who intended to purchase but encountered friction).

They estimate that approximately 26% of cart abandonment is recoverable through UX and process improvements, representing a very large opportunity for merchants willing to invest in checkout optimization.

Cart abandonment email sequences remain among the most high-ROI marketing tactics in e-commerce. Klaviyo's benchmark data for 2025 shows that abandoned cart email sequences generate an average 15% recovery rate, meaning 15% of abandoned carts that receive a follow-up email eventually complete a purchase.

Push notifications show a 7-9% recovery rate. Retargeting ads recover approximately 3-5%. The optimal strategy combines all three channels.

Mobile cart abandonment rates of approximately 85% are substantially higher than desktop rates (67%), confirming that mobile checkout friction is the single largest unsolved UX problem in e-commerce. Progressive web apps (PWAs), in-app checkout, and native app checkout experiences are all strategies merchants use to close the gap.

Conversion Rate Benchmarks

| Product Vertical | Average Conversion Rate | Traffic Source with Best Conversion |

|---|---|---|

| Food and beverage | 4.9% | Email (4.5%) |

| Health and beauty | 4.1% | Direct (3.8%) |

| Home accessories | 2.9% | Organic search (3.2%) |

| Sporting goods | 2.8% | Paid search (2.9%) |

| Apparel | 1.8% | Organic search (3.2%) |

| Electronics | 1.4% | Direct (3.8%) |

E-commerce conversion rates, the percentage of website sessions that result in a purchase, are the most scrutinized metric in the industry and the one most frequently distorted by selective benchmarking.

IRP Commerce's industry benchmark data for 2025, drawn from billions of transactions across thousands of merchants, shows average conversion rates by vertical: food and beverage 4.9%, health and beauty 4.1%, home accessories 2.9%, sporting goods 2.8%, apparel 1.8%, electronics 1.4%.

Consumer electronics' low conversion rate despite high purchase intent reflects extensive comparison shopping, consumers visit multiple sites before purchasing.

Traffic source profoundly affects conversion. Email marketing drives the highest conversion rates (approximately 4.5%) because recipients are already customers or interested prospects. Organic search converts at approximately 3.2%. Paid search (Google Shopping, text ads) converts at approximately 2.9%.

Direct traffic (people who type the URL directly) converts at approximately 3.8%. Social media organic traffic converts at approximately 0.9-1.5%, the lowest of major sources, though social commerce native checkout experiences are improving these figures as the friction of leaving the social platform is removed.

The relationship between traffic volume and conversion rate is negative for most merchants: as paid traffic scales, marginal traffic quality typically decreases. A merchant with excellent conversion rates at low traffic volume will usually see rates decline as paid media spend increases and less-qualified visitors arrive.

Site speed is among the most empirically reliable conversion drivers. Google's research found that a 1-second delay in mobile load time can reduce conversion rates by up to 20%.

A site that loads in 1 second converts approximately 3x better than a site that loads in 5 seconds, per Google's data. This is one of the most consistent findings across e-commerce research.

Social Commerce: The Fastest Growing Segment

Social commerce is the segment of e-commerce attracting the most investor and operator attention in 2025-2026, and for defensible reasons.

Global social commerce sales are forecast at approximately $1.3 trillion in 2026, up from $724 billion in 2022, compound annual growth of approximately 16%, roughly double the overall e-commerce market growth rate.

China dominates global social commerce totals. Douyin (TikTok's Chinese version) has become a full commerce platform, with livestream shopping sessions generating hundreds of millions of dollars per day. WeChat's mini-programs support seamless in-app purchasing across millions of merchants.

This model, entertainment and commerce fully merged, with purchase capability native to the content consumption experience, is now being exported to Western markets with varying degrees of success.

TikTok Shop is the primary vehicle for this export. Launched in the US, UK, and several Southeast Asian markets in 2023, TikTok Shop generated an estimated $50 billion in GMV in 2024 and is projected to reach $80-100 billion in 2025, per eMarketer.

Its growth has been driven primarily by beauty, apparel, electronics accessories, and impulse-purchase categories, areas where short-form video can effectively demonstrate product value in seconds.

Instagram Shopping and Pinterest Shopping represent the more established Western social commerce infrastructure. Meta has invested heavily in Instagram's shopping features, though adoption of in-app checkout has been slower than TikTok Shop's.

Pinterest's 'buyable pins' and visual search shopping features align naturally with the platform's discovery and aspiration use cases, users browsing for home decor or fashion inspiration can purchase directly from boards.

YouTube Shopping, launched in 2023, has grown to be a meaningful commerce channel, particularly in conjunction with YouTube's live shopping functionality.

YouTube's advantage is its longer-form content, product reviews, tutorials, and demonstrations that drive high purchase intent among viewers who have watched extended content about a product.

Delivery, Fulfillment, and Logistics Data

Consumer expectations for delivery speed have been permanently transformed by Amazon Prime's two-day (and increasingly same-day) delivery standard.

A 2025 Convey consumer survey found that 53% of shoppers had abandoned a cart or chosen a different retailer due to slow estimated delivery, and 96% said delivery speed affected where they chose to shop.

Same-day and next-day delivery options have expanded dramatically outside Amazon. Walmart offers same-day delivery from over 4,700 stores, covering approximately 80% of the US population. Target launched same-day delivery in partnership with Shipt.

DoorDash and Instacart have expanded from food into general merchandise delivery, providing same-day logistics infrastructure for thousands of local retailers.

Last-mile delivery remains the most expensive segment of the fulfillment chain, accounting for approximately 53% of total shipping costs according to a 2024 Capgemini Research Institute study.

Autonomous delivery vehicles and drone delivery programs from Amazon (Prime Air), Walmart (through partnerships with Wing and Zipline), and FedEx are in testing or limited deployment phases.

McKinsey estimated in 2024 that autonomous last-mile delivery could reduce costs by 10-40% at scale, though regulatory and technical challenges mean widespread adoption remains several years away.

Cross-border e-commerce is an increasingly significant segment. Juniper Research projected that cross-border e-commerce would reach $3.3 trillion by 2028, driven by platforms like SHEIN, Temu, and AliExpress that ship directly from Chinese manufacturers to global consumers.

The average cross-border cart abandonment rate is higher than domestic (approximately 80%), primarily due to uncertainty about customs duties, longer delivery times, and return complexity.

Returns remain an enormous cost center for e-commerce. The National Retail Federation estimated that US e-commerce returns exceeded $428 billion in value in 2024, approximately 36% of all online purchases were returned.

Return rates are highest in apparel (approximately 40-50% of items purchased online are returned) and lowest in grocery. Return fraud (purchasing with intent to return after use) cost US retailers approximately $24.5 billion in 2024.

Virtual try-on technology, augmented reality fitting rooms, and improved size recommendation algorithms are the primary strategies retailers are deploying to reduce apparel return rates; Shopify data suggests that AR product previews can reduce return rates by 25-40% for applicable categories.

AI and Personalization in E-Commerce

Artificial intelligence is rapidly reshaping the e-commerce experience. McKinsey's 2025 report on AI in retail estimated that personalization engines, systems that tailor product recommendations, search results, and marketing messages to individual users based on behavioral data, drive 10-30% of total e-commerce revenue for merchants that deploy them effectively.

Amazon's recommendation engine alone is estimated to generate 35% of the company's total sales, according to a widely cited McKinsey analysis.

Generative AI applications in e-commerce expanded significantly in 2025. Shopify launched Sidekick, an AI assistant for merchants handling product descriptions, marketing copy, and customer service. Amazon introduced AI-generated product listing summaries that aggregate customer review insights.

Google's Search Generative Experience (SGE) began displaying AI-curated product comparisons directly in search results, with early data suggesting these features increase click-through rates to merchant sites by 12-18% for certain categories.

Conversational commerce, shopping through AI chatbots and voice assistants, generated approximately $290 billion globally in 2025, per Juniper Research.

The integration of large language models into customer service and shopping assistants has made these interactions substantially more useful than the rigid chatbot experiences of previous years.

Klarna reported in 2025 that its AI customer service agent handled two-thirds of all customer service interactions in its first month of deployment, performing the equivalent work of 700 full-time agents.

Practical Implications

For merchants, the data identifies several high-return investment priorities. Checkout optimization, particularly for mobile, consistently shows the highest conversion rate upside.

Cart abandonment recovery sequences (email, push, retargeting) generate immediate, measurable revenue from existing traffic. Site speed improvement affects every visitor and compounds across all marketing efforts.

For brands considering social commerce, TikTok Shop's growth trajectory makes it impossible to ignore for categories with visual demonstration appeal.

The investment required to build a social commerce presence, inventory integration, content production, live shopping capability, is substantial but represents genuine strategic access to a buying-intent audience in a native environment.

For investors and analysts, the concentration of global e-commerce in a handful of platforms (Amazon, Alibaba, and a small number of others) versus the long tail of independent retailers and direct-to-consumer brands is the defining structural tension.

Shopify's growth represents the most credible long-term alternative to platform dependency, giving merchants infrastructure while preserving brand ownership.

For deeper context on the economic forces shaping these trends, see how the stock market works, what is behavioral economics, the long tail explained, and network effects explained.

Sources & Further Reading

- eMarketer / Insider Intelligence. (2025). Global Ecommerce Forecast 2026. emarketer.com.

- US Census Bureau. (2025). Quarterly Retail E-Commerce Sales Q3 2025. census.gov.

- Statista. (2025). Social Commerce Market Worldwide. statista.com.

- Baymard Institute. (2025). Cart Abandonment Rate Statistics. baymard.com.

- Shopify Inc. (2025). Commerce Trends 2026. shopify.com.

- National Retail Federation. (2025). 2024 Consumer Returns in the Retail Industry. nrf.com.

- IRP Commerce. (2025). Ecommerce Industry Benchmarks 2025. irpcommerce.com.

- Salesforce. (2025). Shopping Insights from the Salesforce Platform 2025. salesforce.com.

- Klaviyo. (2025). Email Marketing Benchmarks 2025. klaviyo.com.

- Google. (2024). The Need for Mobile Speed: How Mobile Latency Impacts Publisher Revenue. think.withgoogle.com.

- McKinsey & Company. (2025). The Future of Commerce 2025. mckinsey.com.

- Convey. (2025). Consumer Delivery Expectations Survey 2025. conveyco.com.

Frequently Asked Questions

What is the global e-commerce market size in 2026?

Global e-commerce sales are projected to reach approximately \(6.9 trillion in 2026, according to eMarketer forecasts. This represents growth from \)5.8 trillion in 2023 and \(3.3 trillion in 2019. E-commerce now accounts for approximately 22% of total global retail sales. Growth rates have moderated from the pandemic-era surge (27% growth in 2020) to a more sustainable 8-10% annually, but the absolute numbers continue to climb. Asia-Pacific remains the dominant region, accounting for approximately 60% of global e-commerce sales, driven overwhelmingly by China, where online retail penetration exceeds 52% of total retail. The US e-commerce market reached approximately \)1.2 trillion in 2025, per the US Census Bureau, representing about 16% of total US retail sales.

What share of e-commerce is done on mobile devices?

Mobile commerce (m-commerce) accounts for approximately 73% of all global e-commerce transactions by volume in 2026, though mobile’s share of total e-commerce revenue is somewhat lower at approximately 62%, reflecting that higher-value purchases still skew slightly toward desktop. In markets like India and Indonesia, mobile commerce exceeds 85% of all online purchases, reflecting mobile-first internet adoption. In the United States, mobile accounted for 44% of e-commerce revenue in 2025, per Salesforce Shopping Insights data, lower than global averages but growing approximately 8% year-over-year. Shopify’s data from its merchant base shows that 67% of orders are placed on mobile devices, up from 55% in 2020.

What is the average cart abandonment rate?

The global average shopping cart abandonment rate is approximately 70.19% as of 2025, according to the Baymard Institute’s meta-analysis of 49 shopping cart abandonment studies. This means that roughly 7 in 10 online shoppers who add items to a cart do not complete the purchase. The primary reasons for abandonment, per Baymard’s user research, are: extra costs too high, shipping, taxes, fees (48%); required account creation (26%); complicated checkout process (22%); not trusting the site with payment information (17%); and delivery estimated too slow (16%). Cart abandonment rates vary significantly by industry and device: mobile cart abandonment rates are approximately 85%, compared to desktop rates of approximately 67%.

What is the average e-commerce conversion rate?

Average e-commerce conversion rates, the percentage of site visitors who complete a purchase, vary substantially by industry, traffic source, and device. IRP Commerce’s industry benchmark data for 2025 puts the global average e-commerce conversion rate at approximately 3.65% for desktop and 2.1% for mobile. By vertical, food and beverage shows the highest rates (approximately 4.9%), followed by health and beauty (4.1%), and home goods (2.3%). Fashion shows among the lower conversion rates (approximately 1.8%) despite high traffic volumes. Traffic source matters enormously: email marketing converts at approximately 4.5%, organic search at 3.2%, paid search at 2.9%, and social media at approximately 0.9-1.5%, though social commerce native checkout is improving this metric.

How fast is social commerce growing?

Social commerce, buying products directly through social media platforms without leaving the app, is the fastest-growing segment of e-commerce. Global social commerce sales are forecast at approximately \(1.3 trillion in 2026, up from \)724 billion in 2022, according to Statista. That represents compound annual growth of approximately 16%, roughly double the overall e-commerce growth rate. TikTok Shop is the fastest-growing social commerce platform, generating an estimated \(50 billion in gross merchandise value in 2024 and projected to reach \)80-100 billion in 2025. China’s WeChat and Douyin (TikTok’s Chinese version) dominate global social commerce totals. Instagram and Pinterest shopping features account for most of US and European social commerce, though adoption remains lower than in Asia.