Social: Every 60 seconds, users upload 500 hours of video to YouTube, send 41 million WhatsApp messages, and scroll past roughly 1.7 billion TikTok videos.

Social media is no longer a supplement to daily life for most of the connected world, it is woven into the fabric of how people consume news, maintain relationships, build careers, and spend leisure time.

As of 2026, 5.42 billion people use at least one social media platform, meaning two out of every three humans on earth participates in some form of networked digital conversation.

But the headline user numbers only scratch the surface. What matters equally is how behavior has shifted, which platforms are gaining and losing ground, where advertising money is flowing, and what the research actually says about the consequences of that much time spent in algorithmically curated environments.

This piece compiles the most current, well-sourced data across all of those dimensions.

The picture that emerges is one of a maturing industry experiencing fragmentation rather than uniform growth. Meta's dominance is real but contested. Short-form video has cannibalized nearly every other content format. The creator economy has graduated from a curiosity into a multi-hundred-billion-dollar sector.

And the debate over social media's psychological impact has moved from opinion-column fodder into peer-reviewed medical literature. Here is what the numbers actually say.

"The question is no longer whether social media matters, it clearly does. The question is whether societies are governing it with anywhere near the seriousness the scale demands.", Renee DiResta, Stanford Internet Observatory, 2025

Key Definitions

Monthly Active Users (MAU): A person who has logged into or opened a platform at least once in the past 30 days.

Platforms self-report MAU figures and methodologies vary, Meta counts any Facebook or Messenger access, including automated bots that pass detection, while TikTok's figures exclude users under 13 even in markets without age verification.

Engagement Rate: Typically expressed as (likes + comments + shares) divided by total reach or followers, then multiplied by 100. Industry benchmarks vary significantly by platform and audience size; a 1% engagement rate on a platform like Twitter/X is considered good, while the same rate on TikTok would be considered poor.

Creator Economy: The ecosystem of individuals who monetize original content, encompassing professional YouTubers and TikTok stars, but also part-time bloggers, newsletter writers, and Twitch streamers earning supplemental income. Goldman Sachs defines 'professional creators' as those earning a primary income from content creation.

Social Commerce: The integration of purchase capability directly within social media platforms, allowing users to buy products without leaving an app. Distinct from social media advertising, which drives traffic to external storefronts.

Share of Voice: A metric used in marketing to describe the proportion of social conversation that mentions a specific brand relative to competitors. Often used as a proxy for brand visibility and competitive positioning.

Global User Counts by Platform

The competitive landscape in 2026 looks markedly different from five years ago. Facebook retains the largest absolute user base at approximately 3.12 billion monthly active users, according to Meta's own Q3 2025 earnings disclosures.

However, that number represents growth of only 2.1% year-over-year, a dramatic slowdown from the double-digit growth rates that defined the platform's first decade.

YouTube sits in second place globally with approximately 2.85 billion monthly logged-in users, per Alphabet's investor reports. The platform benefits from a uniquely dual identity: it functions as both a social network and the world's second-largest search engine.

YouTube Shorts, its short-form vertical video product, crossed 2 trillion daily views in mid-2025 after years of struggling to compete with TikTok.

TikTok has reached approximately 1.8 billion monthly active users globally, a figure that excludes markets where the app is banned or restricted, most notably the United States, where it faced a series of legal and legislative challenges throughout 2024 and 2025.

Instagram reports 2.3 billion MAU, with Reels now accounting for more than 50% of all time spent on the platform, according to Meta's internal disclosures cited in their 2025 annual report.

WhatsApp and WeChat each exceed 2 billion users but function more as messaging utilities than traditional social networks, complicating direct comparisons. Telegram has grown substantially, crossing 1 billion users in late 2024.

LinkedIn reports 1.1 billion registered members, though its monthly active figures are typically around 400 million, a distinction the platform's marketing materials tend to obscure.

X (formerly Twitter) has reported approximately 570 million monthly users, though independent researchers and data firms estimate actual engaged monthly users at closer to 350 million.

Platform growth rates tell a different story than absolute size. Pinterest grew by 11% year-over-year, driven by AI-enhanced discovery features and strong performance among women aged 25-45. Reddit grew by 18% following its IPO and international expansion.

BeReal, after a viral peak and steep decline, stabilized at around 40 million daily users. Snapchat's DAU (daily active users) grew 9% to 450 million, with its strongest growth coming from India and the Middle East.

Time Spent: Where Attention Goes

DataReportal's 2026 Global Digital Report, which aggregates panel data from GWI and third-party measurement firms, puts global average daily social media use at 2 hours and 27 minutes. That figure has remained relatively stable since 2022, suggesting attention has reached a saturation point even as user counts grow.

Regional variation is extreme. Filipino internet users spend an average of 3 hours and 53 minutes per day on social media, the highest of any country measured. Brazil, Nigeria, and Colombia all exceed 3 hours. At the opposite end, Japanese users average 51 minutes and German users average 1 hour and 7 minutes.

These differences reflect cultural norms around technology use, the nature of available leisure alternatives, and the relative penetration of mobile-first internet access.

Among platforms, TikTok drives the highest average session time. Comscore data from Q2 2025 shows the average TikTok session lasting 10.85 minutes, compared to 8.44 minutes for YouTube and 6.35 minutes for Instagram.

Facebook sessions average 4.7 minutes, reflecting its transition toward being a utility checked briefly for events, marketplace listings, and group updates rather than a passive scrolling experience for younger demographics.

Video content now dominates time spent across all platforms. Nielsen's Total Audience Report for 2025 found that 67% of all social media time was spent consuming video content of some kind, including short-form (under 60 seconds), medium-form (1-10 minutes), and long-form (over 10 minutes).

Live streaming alone accounts for 5% of total social media time, with gaming and sports content driving the bulk of that category.

Age Demographics

The demographic composition of social media has shifted significantly since the mid-2010s.

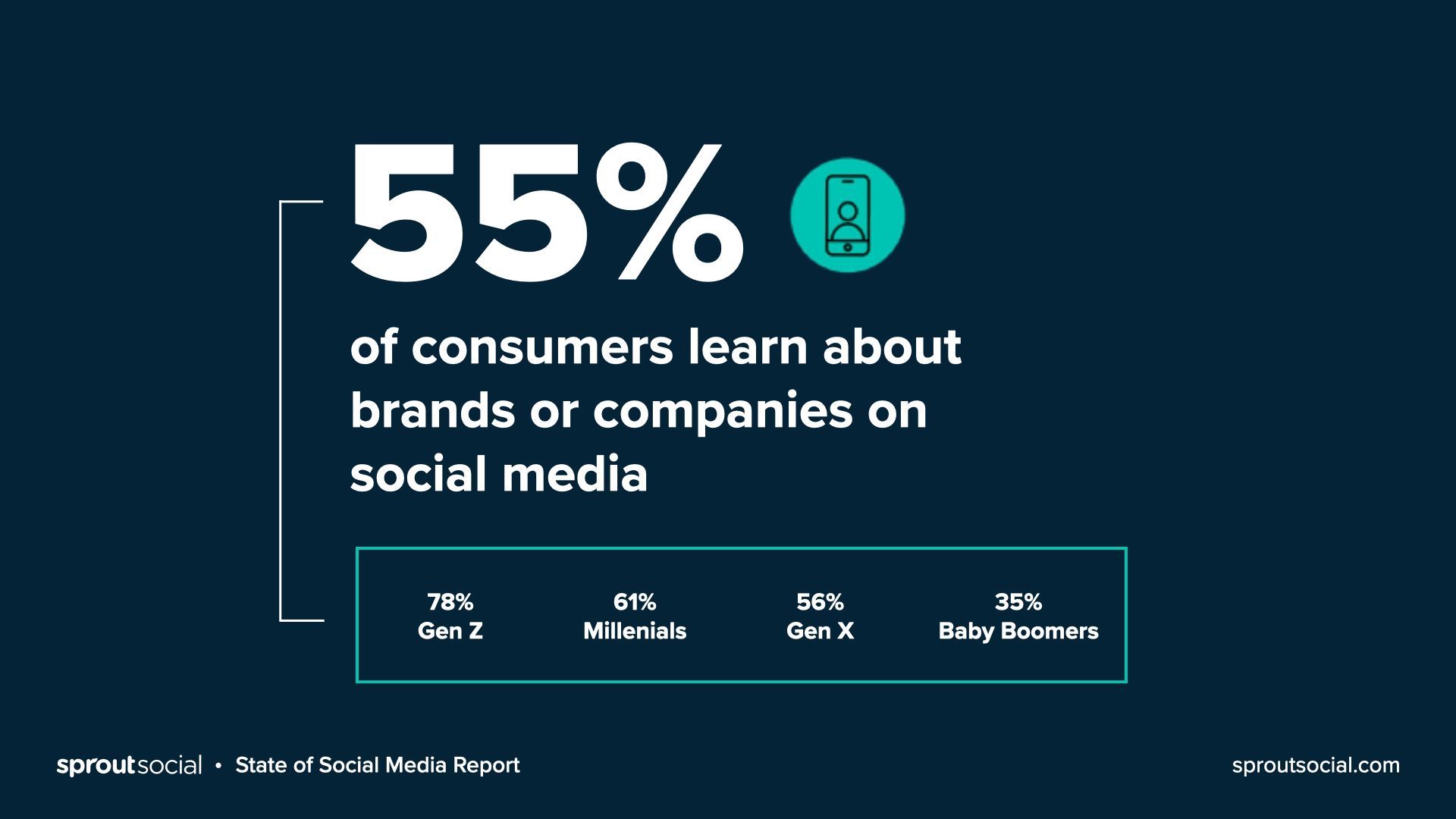

Pew Research Center's 2025 Social Media Use report found that 84% of Americans aged 18-29 use YouTube, making it the dominant platform for young adults, ahead of Instagram (78%), TikTok (72%), and Snapchat (65%).

Facebook, by contrast, is used by only 54% of that age group, compared to 72% of adults over 50.

The youth migration away from Facebook toward TikTok, Instagram, and Snapchat is now essentially complete in North America and Western Europe. The average age of a Facebook user in the United States is estimated at 40.5 years as of 2025, up from 37 in 2020.

This is not inherently a crisis for Meta, older demographics control more disposable income and are often more receptive to advertising, but it represents a fundamental repositioning of the platform's identity.

TikTok's age skew has also shifted upward. Among TikTok's US user base in 2025, 40% were over 35, compared to 26% in 2021. The platform is no longer primarily a teenage phenomenon.

YouTube's demographic spread remains the most even: Pew data shows 83% of 50-to-64-year-olds using it, close to the 84% among 18-to-29-year-olds, a remarkable breadth for a single platform.

LinkedIn's user base skews heavily toward 25-to-44-year-olds (54% of users), with strong representation among college-educated professionals. Pinterest's core audience is women aged 25-44, a demographic that represents 60% of its active users.

Reddit's user base remains male-skewed (approximately 62% male globally) and younger, with 42% of users between 18 and 29.

Advertising Revenue and Market Share

Social media advertising is a $247 billion global market in 2026, according to Statista's digital advertising forecasts. This represents a compound annual growth rate of roughly 9% since 2022, outpacing overall digital advertising growth. Social media now captures approximately 28% of all digital advertising spend globally.

Meta remains the dominant player. Facebook and Instagram combined generated approximately $162 billion in advertising revenue in 2025, per Meta's annual report, representing about 28% of the global social ad market.

Meta's average revenue per user (ARPU) in the United States and Canada was $68.44 per quarter in Q4 2025, a figure that illustrates the enormous monetization gap between Western markets and developing regions.

TikTok's advertising business has grown explosively. Its global ad revenue exceeded $32 billion in 2025, up from $18 billion in 2023, according to eMarketer estimates. This growth has been driven primarily by TikTok for Business's expansion in Southeast Asia, the Middle East, and Europe.

YouTube's advertising revenue hit approximately $36 billion in 2025, per Alphabet's financial disclosures, with a growing proportion coming from connected TV (YouTube on smart TVs and streaming devices).

LinkedIn's advertising business crossed $10 billion annually for the first time in 2025, driven by demand for B2B lead generation tools. Snap's advertising revenue grew 14% to approximately $5.4 billion.

Pinterest reported $3.7 billion, up 11% year-over-year, benefiting from its 'shoppable pins' product and AI-powered visual search.

The concentration of social ad spend is notable: Meta, Google (YouTube), TikTok, and LinkedIn collectively account for over 80% of all social media advertising revenue globally. Smaller platforms collectively share the remaining approximately 20%.

Engagement Rates by Platform and Content Type

| Platform | Average Engagement Rate per Post | Top Content Format | Ad Revenue (2025) |

|---|---|---|---|

| TikTok | 4.1% | Short-form video | ~$32 billion |

| Instagram Reels | 2.8% | Short-form video | (part of Meta $162B) |

| YouTube | 1.9% (per view) | Long and short video | ~$36 billion |

| 0.54% | Video, text | ~$10 billion | |

| Facebook Pages | 0.61% | Live video, groups | (part of Meta $162B) |

| X (Twitter) | 0.23% | Text, short video | Declining |

Engagement rates have declined across most platforms as content volume has surged.

Socialinsider's 2025 Social Media Benchmarks report, which analyzed over 22 million posts, found average engagement rates as follows: TikTok leads with 4.1% average engagement per post; Instagram Reels average 2.8%; YouTube average 1.9% (measured by interactions per view); Facebook Pages average 0.61%; LinkedIn posts average 0.54%; Twitter/X averages 0.23%.

Video consistently outperforms static content. On Instagram, Reels receive 3x the engagement of static image posts, according to Meta's own Creator Insights data from 2025. On LinkedIn, video posts receive 5x more comments than text-only posts. On Facebook, live video generates 6x the engagement of pre-recorded video.

Smaller accounts consistently show higher engagement rates than large accounts, a pattern that has held across multiple years of data.

Influencer marketing platform HypeAuditor's 2025 report found that nano-influencers (1,000 to 10,000 followers) achieve an average Instagram engagement rate of 3.7%, compared to 0.9% for mega-influencers with over 1 million followers.

This has driven a sustained shift toward micro and nano influencer marketing strategies among brands.

The Creator Economy: Scale and Economics

Goldman Sachs projected in its 2024 report 'The Creator Economy' that the sector would reach approximately $480 billion in value by 2027.

By comparison, the global music industry is worth approximately $28 billion and the film industry approximately $95 billion, numbers that illustrate the creator economy's staggering scale relative to traditional entertainment.

Approximately 207 million people globally identify as content creators in some capacity, according to Adobe's 'Future of Creativity' report (2022, with 2025 follow-up updates). Of these, roughly 4 million earn a primary income from content creation.

The distribution of earnings is extremely unequal: the top 1% of creators earn a median of $232,000 annually, while the median creator earns approximately $8,500 per year from content-related income.

YouTube's Partner Program paid out over $30 billion to creators through AdSense in the 12 months ending September 2025, per Alphabet's disclosures. TikTok's Creativity Program (the renamed Creator Fund) and brand marketplace added an estimated $15 billion to creator incomes.

Substack, Patreon, and other subscription platforms collectively pay out approximately $3.2 billion annually to creators.

Brand sponsorships and partnerships account for approximately 68% of professional creator revenue, according to Creator Economy research firm Influencer Marketing Hub. Platform payouts account for 17%, and merchandise, courses, and digital products make up the remaining 15%.

The financial dependence on brand deals makes creators vulnerable to shifts in advertiser sentiment and platform algorithm changes.

Platform Growth and Decline Trends

Not all platforms are growing. Snapchat's daily active user count in the United States peaked in 2022 and has grown only marginally since, with the platform increasingly competing for relevance among users under 25.

X (formerly Twitter) has seen sustained advertiser exodus following its 2022 acquisition, eMarketer estimates X's US ad revenue declined approximately 35% between 2022 and 2025, though international markets partially offset those losses.

Tumblr, once a major creative platform, has stabilized at approximately 135 million monthly active users after years of decline following its 2018 adult content ban.

Pinterest's growth recovery, driven by Gen Z's 'visual search' behavior and AI recommendations, represents one of the more notable platform revivals in recent memory, with MAU growing from 460 million in 2022 to approximately 560 million in 2025.

Reddit's IPO in March 2024 injected capital and operational discipline into a platform that had long punched below its weight in monetization. Monthly active users grew from 73 million at IPO to approximately 107 million by Q4 2025, with international growth (particularly in India, the UK, and Brazil) accounting for much of the gain.

Mastodon and the broader 'fediverse' (decentralized social networks built on open protocols) have grown to approximately 12 million registered accounts, a tiny fraction of mainstream platforms but a meaningful signal of interest in non-algorithmic, non-advertising-dependent social networking.

Bluesky reached approximately 25 million users by end of 2025 and continues to grow as a Twitter/X alternative.

Social Media and Mental Health: What the Research Shows

The scientific literature on social media and mental health has matured significantly. Rather than sweeping claims in either direction, researchers now distinguish between types of use, user age, and platform design features.

A 2025 meta-analysis published in JAMA Psychiatry, analyzing 59 studies covering more than 150,000 participants, found that passive social media consumption, scrolling without liking, commenting, or interacting, showed consistent associations with increased loneliness, lower self-esteem, and depression symptoms.

Active, interactive use showed neutral or slightly positive mental health associations.

The U.S. Surgeon General's 2024 advisory on social media and youth mental health cited data showing that adolescents who spend more than 5 hours daily on social media are 66% more likely to report depression symptoms than those who do not use social media.

The advisory stopped short of calling for a minimum age requirement but explicitly encouraged Congress to consider one.

Particularly among girls aged 10-14, the period from 2012 to 2023 saw significant increases in anxiety, depression, and self-harm rates in countries where smartphone adoption accelerated, a correlation noted by researchers Jean Twenge and Jonathan Haidt, though causation remains debated.

A 2025 study by the Adolescent Brain Cognitive Development (ABCD) study, tracking over 11,000 US children, found that heavy social media use at age 9-10 predicted reduced gray matter development in attention-related brain regions by age 11-12.

Sleep disruption via social media use at night is one of the more consistent findings across the literature. A 2025 study in Sleep Medicine Reviews found that social media use within 30 minutes of bedtime was associated with an average 23-minute delay in sleep onset and reduced sleep quality scores across all age groups.

Practical Implications

For brands and marketers, the data points toward several actionable conclusions. Platform diversification matters more than it did three years ago, no single platform commands the attention of all demographic groups, and algorithmic volatility makes over-reliance on any one channel risky.

Video investment is no longer optional; it is the dominant content format by engagement on every major platform.

For parents and educators, the research supports time limits and delayed smartphone adoption, not as absolute prohibitions, but as reasonable precautions given the growing body of evidence linking heavy passive use with mental health impacts, particularly in adolescents.

Active, connected use (messaging family, participating in communities) appears substantially less harmful than passive algorithmic scrolling.

For policymakers, the scale of the industry, $247 billion in advertising revenue, 5.42 billion users, and children as young as 8 routinely using platforms designed for adults, suggests that voluntary industry self-regulation has reached its limits.

Regulatory frameworks governing data collection, algorithmic transparency, and age verification are under active development in the EU, UK, Australia, and several US states.

For individuals, the most consistent finding across the research is one of intentionality: people who approach social media use with specific purposes and time awareness report significantly better experiences than those who open apps reflexively or habitually.

The platforms are engineered for the latter behavior, understanding that is the first step toward a healthier relationship with them.

Sources & Further Reading

- DataReportal. (2026). Digital 2026: Global Overview Report. DataReportal.com.

- Meta Platforms, Inc. (2025). Q4 2025 Earnings Report and 10-K Filing. investor.fb.com.

- Statista. (2026). Social Media Advertising Revenue Worldwide 2018-2028. statista.com.

- Goldman Sachs. (2024). The Creator Economy: Sizing the Opportunity. goldmansachs.com.

- Pew Research Center. (2025). Social Media Use in 2025. pewresearch.org.

- Alphabet Inc. (2025). 2025 Annual Report and Form 10-K. abc.xyz.

- eMarketer / Insider Intelligence. (2025). US Social Network Ad Revenues 2025. emarketer.com.

- Socialinsider. (2025). Social Media Benchmarks 2025. socialinsider.io.

- HypeAuditor. (2025). State of Influencer Marketing 2025. hypeauditor.com.

- Adobe. (2022, updated 2025). Future of Creativity. adobe.com.

- U.S. Surgeon General. (2024). Social Media and Youth Mental Health: The Surgeon General's Advisory. hhs.gov.

- Twenge, J.M. & Haidt, J. (2023). The Anxious Generation. Penguin Press. (Updated with 2025 follow-up data.)

Frequently Asked Questions

How many people use social media in 2026?

As of 2026, approximately 5.42 billion people use social media globally, representing roughly 66% of the world’s population. This marks a significant increase from 4.95 billion in 2023. Growth is primarily driven by expanding internet access in Southeast Asia, Sub-Saharan Africa, and Latin America. The average person now uses 6.7 social media platforms per month, up from 6.1 in 2022. Facebook remains the largest single platform with over 3.1 billion monthly active users, though its user growth has plateaued in North America and Europe. TikTok and YouTube continue to see the strongest growth trajectories globally.

How much time do people spend on social media daily?

The global average time spent on social media in 2026 is 2 hours and 27 minutes per day, according to DataReportal. This varies considerably by region and age. Filipinos spend the most time on social media at approximately 3 hours 53 minutes daily, while Japanese users average just 51 minutes. Among 18-to-24-year-olds in the United States, daily social media use averages 3 hours 11 minutes. Video-centric platforms, TikTok, YouTube, and Instagram Reels, now account for over 65% of total social media time spent. Short-form video content drives the highest engagement per session.

What is the total social media advertising revenue in 2026?

Global social media advertising revenue reached an estimated \(247 billion in 2026, up from \)207 billion in 2023, according to Statista projections. Meta (Facebook and Instagram combined) commands approximately 28% of global social ad spend, making it the largest single player. TikTok’s advertising revenue surpassed \(32 billion, cementing its position as the third-largest social ad platform. LinkedIn ad revenue exceeded \)10 billion for the first time, driven by B2B demand. The United States remains the single largest market, generating roughly $84 billion in social ad revenue annually.

How large is the creator economy in 2026?

The creator economy was projected by Goldman Sachs to reach approximately \(480 billion in value by 2027. Approximately 207 million people globally identify as content creators in some capacity. Of these, roughly 4 million are considered 'professional creators' earning a primary income from content. YouTube pays out over \)30 billion annually to creators through AdSense alone. TikTok’s Creator Fund and brand partnership ecosystem adds another estimated $15 billion. Brand sponsorship deals account for roughly 68% of professional creator revenue, with merchandise and platform payouts making up the remainder.

What does the research say about social media and mental health?

Research on social media and mental health shows a nuanced picture. A 2025 meta-analysis published in JAMA found that passive consumption of social media, scrolling without interacting, was associated with higher rates of loneliness and depression symptoms, particularly among adolescents. However, active use such as messaging and community participation showed neutral or slightly positive mental health associations. Among teenagers who use social media more than 5 hours daily, rates of depression symptoms are approximately 66% higher than among non-users, per data from the U.S. Surgeon General’s 2024 advisory. Platforms with algorithmic infinite scroll designs show the strongest associations with compulsive use patterns.