Thinking: In 1997, Jeff Bezos was considering leaving a well-paid job at a New York hedge fund to start an online bookstore. He was not sure it would work. He described the decision process in a 2010 commencement speech: "I knew that when I was 80 I would never regret having tried this.

I would not regret failing. But I knew the one thing I might regret is not ever having tried."

This is long-term thinking applied to a personal decision: evaluating a choice from a future vantage point rather than the anxious present, and weighting future regret more heavily than near-term risk.

Most people believe they think long-term. Most evidence suggests they do not, or at least, that they do so far less than they believe. The gap between our self-image as forward-thinking strategic agents and our actual decision-making patterns is one of the best-documented findings in behavioral science.

What Is Long-Term Thinking?

Long-term thinking is the practice of making decisions that give appropriate weight to future consequences, not just immediate outcomes. It involves accurately imagining future states, discounting them at a realistic rate rather than an instinctively steep one, and building commitments that protect future options and wellbeing.

The concept is deceptively simple. In practice, it requires overriding a set of deeply ingrained cognitive biases that systematically push human decision-making toward the immediate future at the expense of the distant one.

Long-term thinking is not the same as:

- Planning, planning is a process; long-term thinking is a cognitive orientation that determines whether the plan appropriately accounts for future consequences

- Pessimism, long-term thinking sometimes means accepting short-term cost for long-term gain, which optimists and pessimists alike can do or fail to do

- Caution, investing aggressively in a durable business is long-term thinking even though it involves risk; avoiding all risk to preserve current status is sometimes short-term thinking in disguise

The field of behavioral economics has spent decades documenting the gap between how people think they make decisions and how they actually do.

Kahneman and Tversky's foundational work on cognitive biases (1979, 1984) established that the mind uses heuristics, mental shortcuts that work well in ordinary situations but fail systematically in certain contexts, including those that require accurate temporal reasoning.

Long-term thinking, when it succeeds, is an effortful process of overriding instinct with deliberate analysis. Understanding what makes it so difficult is the first step toward doing it better.

The Neuroscience of Short-Termism: Hyperbolic Discounting

The primary neurological mechanism driving short-termism is called hyperbolic discounting, a pattern of time preference that values immediate rewards dramatically more than future rewards, with a discount rate that falls steeply with time horizon.

Classical economics assumed exponential discounting: future rewards are discounted at a constant rate per time period. If you discount at 10% per year, a reward worth $100 in one year is worth $91 today, and a reward worth $100 in two years is worth $83 today, a consistent pattern that produces time-consistent preferences.

Research by psychologists Richard Thaler, George Loewenstein, and others established that humans actually discount hyperbolically.

We discount very heavily between "now" and "soon," but very little between "ten years from now" and "eleven years from now." This creates time inconsistency: preferences reverse as the moment of decision approaches.

The classic demonstration: most people prefer to receive $100 today over $110 in one month (impatient preference), but prefer $110 in 13 months over $100 in 12 months (patient preference). The interval is identical, one month, but the temporal distance reverses the preference.

This is why New Year's resolutions fail at the scale they do: the future self who will benefit from the habit seems real in December, but by January, the immediate cost of the behavior overwhelms the abstract future benefit.

A landmark study by Norcross, Mrykalo, and Brinker (2002) published in the Journal of Clinical Psychology found that 54% of resolution-makers had abandoned their goals by six months, with the steepest dropout occurring in the first two weeks, precisely the period when present-moment temptation is strongest and the future reward most abstract.

Measurable Discount Rates

Research by Laibson (1997) at Harvard formalized hyperbolic discounting into a mathematical model and estimated that people effectively apply annual discount rates of 20-40% to near-future events, far higher than any reasonable long-term investment return, but much lower rates of 2-5% to events in the distant future.

This asymmetry means that near-term costs and benefits are wildly over-weighted compared to long-term consequences, with enormous practical implications for health, savings, and policy.

| Time Horizon | Implied Behavioral Discount Rate |

|---|---|

| Today vs. tomorrow | Often hundreds of percent (annualized) |

| This month vs. next month | 40-80% (annualized) |

| This year vs. next year | 20-40% |

| 5 years from now vs. 6 years | 5-10% |

| 20 years from now vs. 21 years | 2-4% |

Source: Laibson (1997), Frederick, Loewenstein, O'Donoghue (2002)

The policy implications are significant. If people behave as though they discount next year's income at 30% but their retirement income at 4%, they will systematically under-save, not out of ignorance about retirement, but because the psychological weight of present spending crushes the abstract appeal of a comfortable retirement 30 years away.

Your Future Self Is a Stranger

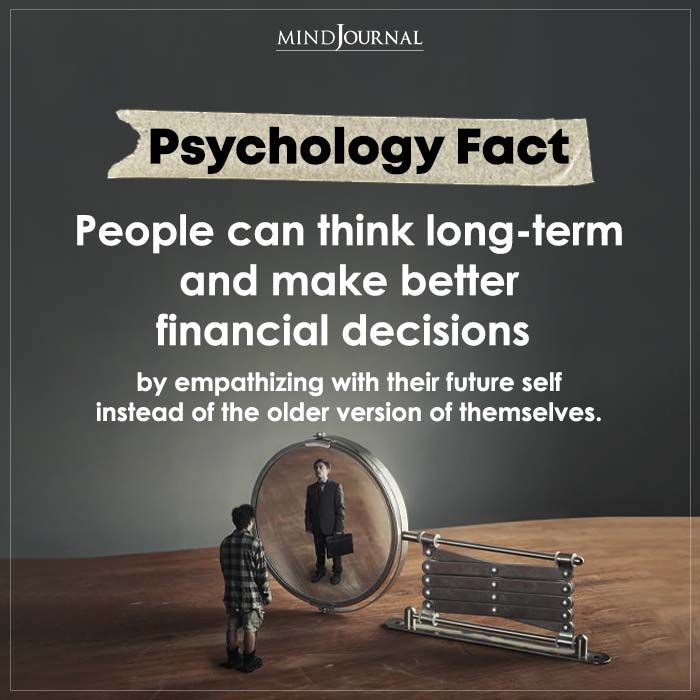

Brain imaging research has added a striking finding to the story of temporal discounting. Psychologist Hal Ersner-Hershfield and colleagues (2009) used fMRI to examine neural responses when people thought about their current selves, their future selves, and a stranger.

The finding: neural patterns while thinking about the future self were significantly more similar to neural patterns while thinking about a stranger than to patterns while thinking about the current self. Psychologically, our future selves are not fully "us", they are partially experienced as other people.

"The degree to which people feel continuity with their future selves predicts their retirement savings, ethical behavior, and long-term planning.", Hal Ersner-Hershfield, UCLA Anderson School of Management (2011)

This has direct implications for decisions with delayed consequences. Accepting health risks now (sedentary lifestyle, poor diet, financial under-saving) is neurologically somewhat like passing the costs to someone else. The future person who will experience those consequences does not fully register as self.

Interventions that make the future self more vivid and concrete, including age-progression technology that shows people their older faces, have been shown to increase long-term financial savings. In a 2011 study by Ersner-Hershfield et al.

published in Journal of Marketing Research, participants shown age-progressed photographs of themselves allocated more than twice as much money to a hypothetical retirement account compared to a control group that saw only their current appearance. The mechanism is making the future self feel more like the current self.

This insight has practical implications beyond research. Apps that show users the projected effect of dietary choices on their future health, or retirement calculators that display a personalized future spending scenario, are applying the same principle: making the distant, abstract future concrete and personal enough to motivate present-day behavior change.

Why Organizations Are Also Short-Sighted

Short-termism is not only a problem of individual psychology. Organizations and markets create structural pressures that compound individual biases.

Quarterly Earnings Pressure

Publicly listed companies are evaluated on quarterly earnings, creating pressure on executives to manage toward quarterly targets at the expense of multi-year investment.

Research by McKinsey Global Institute (Barton, Manyika, and Williamson, 2017) found that companies with long-term orientation, investing in R&D, human capital, and infrastructure over a five-year period regardless of short-term earnings impact, generated 47% higher revenue growth, 36% higher earnings growth, and added nearly 12,000 more jobs than short-term-oriented peers over the 2001-2014 measurement period.

The same McKinsey analysis found that long-term-oriented companies delivered better shareholder returns: their total return to shareholders exceeded that of short-term peers by roughly 50% over the ten years studied.

This is the cruel irony of institutional short-termism: the pressure to deliver quarterly results undermines the very performance that produces superior long-run shareholder value.

Political Cycles

Democratic governments face re-election cycles that create incentives to deliver visible benefits before the next election and defer costs beyond it.

Infrastructure maintenance (which prevents future deterioration but creates no ribbon-cutting moment), pension reform (which benefits future retirees at the cost of current ones), and climate policy (which imposes current costs for future benefits) all suffer from short electoral time horizons.

A striking empirical analysis by Besley and Case (1995) found that US governors in their final term, freed from re-election pressure, made significantly different budget decisions than those facing future elections, spending less on visible short-term programs and more on infrastructure investment.

The finding suggests that at least some political short-termism reflects rational strategic behavior rather than genuine preference for short-term outcomes.

Principal-Agent Problems

In many organizations, the people making long-term decisions do not bear the long-term consequences. Executives who will retire or move companies before a 20-year investment pays off have weakened incentives to make it.

Fund managers evaluated annually have diminished incentives to hold positions over a decade. Short-termism is partly a consequence of misaligned incentives, not just cognitive bias.

The financial crisis of 2008 illustrated this problem with devastating clarity. Mortgage originators who sold loans and immediately securitized them bore no risk from the long-term performance of those loans, creating incentives to maximize volume at the expense of quality.

The time horizon mismatch between those making the decisions and those bearing the eventual consequences was a structural driver of the crisis, as documented extensively in the Financial Crisis Inquiry Commission report (2011).

Frameworks That Enable Long-Term Thinking

Jeff Bezos's Regret Minimization Framework

Bezos's framework projects decision-making to age 80 and asks which choice produces less regret at that vantage point.

It is effective because it shifts temporal framing: instead of evaluating a decision from the immediate present (where near-term fear dominates), it evaluates from a future point where near-term costs have dissolved and the long-term pattern is visible.

The framework does not always point toward risk-taking. Sometimes the regret-minimizing choice is caution. But it consistently discounts the emotional intensity of present-moment anxiety, which tends to create excessive short-termism.

Bezos has extended this framework institutionally. Amazon's annual shareholder letters consistently reference the company's willingness to accept years of unprofitability in pursuit of market-building, and its philosophy of measuring itself over three-year and five-year horizons rather than quarterly ones.

Amazon's willingness to operate at near-zero profit margins for its first decade, a strategy that baffled Wall Street analysts focused on quarterly earnings, ultimately produced the platform dominance that generated its current profit streams.

Stewart Brand's Pace Layers

Architect and author Stewart Brand introduced the pace layers framework in his 1999 book The Clock of the Long Now and the Long Now Foundation's work on long-term civilization thinking.

Brand describes civilization as composed of six nested layers that change at different rates:

| Layer | Change Rate | Examples |

|---|---|---|

| Fashion and art | Fastest | Trends, styles, zeitgeist |

| Commerce | Fast | Products, companies, markets |

| Infrastructure | Moderate | Roads, power grids, buildings |

| Governance | Slow | Laws, political institutions |

| Culture | Very slow | Shared values, language, religion |

| Nature | Slowest | Ecosystems, climate, geology |

The faster layers innovate and adapt; the slower layers provide stability and constraint. Healthy systems maintain the friction between layers, fashion can innovate freely within commercial infrastructure, but cannot rewrite governance at the same pace. When a fast layer tries to move at its pace through a slow layer, disruption follows.

The framework illuminates why "moving fast and breaking things" in technology has produced genuine innovation alongside governance and cultural crises: the fast commercial and technological layers moved faster than governance and culture could absorb.

Long-term thinking requires attending to the slower layers, not just the fast ones.

The Long Now Foundation's 10,000-Year Clock

The Long Now Foundation was established in 01996 (they add a leading zero to all years to discourage 10,000-year clocks being the century problem of future civilizations) to promote long-term thinking as a cultural practice.

Their flagship project, a mechanical clock designed to run accurately for 10,000 years inside a mountain in Texas, is explicitly symbolic: an attempt to make geological timescales viscerally real.

Their work identifies the short-term bias as partly a failure of imagination: it is difficult to care about futures you cannot vividly imagine. Institutions, artifacts, and practices that make long futures imaginable serve a function beyond their direct utility.

Pre-Mortem Analysis

The pre-mortem, developed by cognitive psychologist Gary Klein and described in his 2007 article in the Harvard Business Review, is a structured technique for prospective thinking.

Before committing to a decision, a team is asked to imagine that the decision has already been made, that significant time has passed, and that the outcome was a failure. The team then works backward to identify the most plausible reasons for that failure.

The pre-mortem works because it exploits prospective hindsight, the cognitive phenomenon by which imagining a specific outcome as already having occurred makes it easier to identify its causes.

Klein's research found that pre-mortems increased the ability to identify reasons for future outcomes by approximately 30% compared to traditional forward-looking analysis.

For long-term decisions, the pre-mortem is particularly valuable because it forces consideration of second and third-order consequences that optimistic forward planning tends to dismiss.

Institutions That Enable Long-Term Thinking

Individual willpower is not sufficient to override systematic short-termism. Sustained long-term thinking requires institutional structures that create long time horizons and protect decisions from short-term pressure.

University Endowments

Major university endowments are managed to exist in perpetuity and support institutional missions across centuries. Endowment management practices, targeting a sustainable withdrawal rate (typically 4-5% annually) while preserving real principal, operationalize multi-generational time horizons.

The Yale endowment approach developed by David Swensen (detailed in his 2000 book Pioneering Portfolio Management) demonstrated that long-horizon investing could sustain higher allocations to illiquid assets with premium returns.

Yale's endowment generated annualized returns of approximately 12.4% over the 20 years following Swensen's restructuring, substantially outperforming conventional balanced portfolios, a direct result of the endowment's ability to tolerate illiquidity that shorter-horizon investors could not.

Sovereign Wealth Funds

Norway's Government Pension Fund Global, the world's largest sovereign wealth fund at over $1.7 trillion, was established to invest Norway's oil revenues for future generations.

It holds shares in approximately 9,000 companies globally, publishes its ethical standards for investment, and has an explicit mandate to benefit future citizens.

The fund's governance structure is explicitly designed to insulate investment decisions from short-term political pressure.

Norway's approach provides a striking contrast with countries that extracted similar natural resource wealth without creating inter-generational savings structures.

Norway's per-capita government financial assets rank among the highest in the world; many other significant oil producers have little to show for decades of resource extraction.

Japan's Long-Lived Companies

Japan has an unusual concentration of very old businesses, companies that have operated continuously for centuries or more. These shinise (literally "long-established") businesses, which include sake breweries, construction firms, and hotels, are often family-owned or managed with strong identity preservation.

Research by Stadler (2011) and Hamel and Valikangas (2003) has attributed their longevity to conservative financial management, deep craft identity, and institutional practices that transfer knowledge across generations.

Of the world's approximately 5,600 companies that are more than 200 years old, more than half are Japanese. The country has a distinct institutional culture of jokamachi, castle town businesses, that has persisted through industrialization, war, and technological disruption.

These businesses have not survived through static preservation; they have adapted, but always with a core identity that is itself a long-term asset.

Constitutional Commitments

Constitutional provisions that are deliberately difficult to change, supermajority requirements, multi-step amendment processes, judicial review, are mechanisms for protecting long-run commitments from short-run political pressure.

They represent a recognition that future majorities should be constrained by the commitments of past ones in certain domains.

James Madison's argument in Federalist No. 51 for constitutional checks and balances is, at its core, an argument about the management of short-termism in politics: that present majorities cannot be trusted to make decisions that fully respect the interests of future majorities, and that institutional friction is the mechanism that creates the temporal buffer.

The Compounding Argument: Why Time Is the Most Powerful Variable

One of the clearest demonstrations of long-term thinking's value is compound growth. Einstein reportedly called compounding the eighth wonder of the world, though the attribution is disputed. The mathematics are real regardless of the source.

An investor who begins saving $500 per month at age 25 and earns 8% annually will have approximately $1.7 million at age 65. The same investor starting at 35, ten years later, will have approximately $745,000.

The difference of $755,000 comes from ten additional years of compounding, not from an additional $60,000 in contributions (which the later-starting investor could easily have saved from later higher earnings).

The first decade is worth far more than its face value because of the compounding time it enables.

| Starting Age | Monthly Contribution | Rate of Return | Balance at Age 65 |

|---|---|---|---|

| 22 | $500 | 8% | $2.07 million |

| 25 | $500 | 8% | $1.74 million |

| 30 | $500 | 8% | $1.17 million |

| 35 | $500 | 8% | $745,000 |

| 40 | $500 | 8% | $466,000 |

The gap between starting at 22 and starting at 40, $1.6 million, is not primarily explained by contribution amount. It is explained by 18 additional years of compounding. Long-term thinking, applied to the specific decision of when to start investing, produces outcomes that cannot be replicated by later effort or higher contributions.

This is why time in the market is consistently cited by financial economists as more valuable than timing the market.

The investor who tries to time market cycles and is out of the market for even a handful of the best-performing days over decades ends up with dramatically inferior outcomes compared to the patient investor who simply holds through volatility.

Practical Applications of Long-Term Thinking

Personal Decisions

The regret minimization framework applies broadly. Before a major decision, career change, relationship, significant financial commitment, project to age 70 or 80 and ask which choice you would look back on with regret.

This does not always recommend the bolder option, but it consistently deflates the emotional weight of near-term fear and loss aversion.

For investments and saving, the compounding argument for starting early is overwhelming and widely known.

What is less appreciated is that the decision of whether to start investing at 25 versus 35 is not primarily a financial question, it is a question of whether you can maintain the long-term frame when short-term consumption is immediately rewarding.

Research on present bias by O'Donoghue and Rabin (1999) showed that people who are aware of their own present bias can use commitment devices to protect long-term goals: automatic enrollment in retirement plans, commitment savings accounts that impose penalties for early withdrawal, and pre-committing to future actions before the moment of temptation arrives.

These behavioral tools work by mechanically enforcing long-term preferences before the short-term self can override them.

Organizational Decisions

Long-term organizational thinking requires creating structures that survive individual leadership changes. Strategic principles, not just strategic plans; values embedded in hiring and evaluation, not just mission statements; financial structures that provide runway for multi-year investments rather than requiring quarterly justification.

The practice of writing pre-mortems, imagining that a decision has failed and working backward to understand why, is a technique for expanding temporal consideration before commitment.

Companies like 3M that have institutionalized a percentage of employee time for exploratory work without immediate commercial application are building organizational structures that enable long-term thinking even under short-term commercial pressure.

3M's "15% time" policy, allowing employees to spend 15% of their work time on projects of their own choosing, produced Post-it Notes and Scotch Tape, products that became commercial pillars of the company decades after their development.

Environmental and Societal Decisions

Climate change is the defining long-term thinking challenge of the current era. The costs of mitigation are immediate and visible; the benefits are distant and diffuse. The victims of inaction are future people who do not yet exist and cannot vote.

Every structural feature of short-termism works against adequate response: hyperbolic discounting, the psychological distance of future selves, short political cycles, misaligned incentives.

The Stern Review on the Economics of Climate Change (2006) explicitly framed climate policy as a question of temporal discounting: how much should current generations sacrifice for the benefit of future generations?

Stern's controversial recommendation for a near-zero social discount rate, treating future people's welfare almost as equally important as current people's welfare, directly challenged the hyperbolic discounting patterns that characterize most human decision-making.

The solutions are correspondingly structural: carbon pricing that makes future costs present costs, independent central bank-style climate institutions insulated from electoral cycles, and international commitments that constrain domestic short-term politics.

Measuring Long-Term Thinking: The CEOS Index and Corporate Evidence

Researchers at McKinsey, Harvard, and the University of Toronto have attempted to quantify corporate long-termism systematically. The McKinsey Corporate Horizon Index assigns companies long-term or short-term orientation based on patterns in capital investment, R&D spending, earnings quality, and management guidance practices.

Their analysis of the S&P 500 found that approximately 65% of large US companies were operating with a primarily short-term orientation as of 2017.

The evidence consistently shows that long-term-oriented companies:

- Invest more in R&D as a share of revenue

- Show less sensitivity to quarterly earnings miss thresholds

- Generate higher total shareholder returns over 10-year periods

- Create more employment per dollar of revenue growth

Yet short-termism persists because of the structural incentives that produce it, fund managers with annual performance reviews, analyst estimates creating quarterly pressure, and executive compensation tied to near-term stock performance rather than decade-long compounding.

Conclusion

"In the short run, the market is a voting machine but in the long run it is a weighing machine.", Benjamin Graham, The Intelligent Investor (1949), describing how long time horizons reveal fundamentals that short-term noise obscures, a principle that applies far beyond finance

Long-term thinking is not a personality trait that some people have and others lack. It is a practice that runs against deeply wired cognitive tendencies, tendencies that served our ancestors well in environments where the future was unpredictable and immediate survival mattered most.

In complex modern environments where decisions made today have consequences across decades, in climate, finance, health, career, and institutional design, the cost of systematic short-termism is enormous.

The frameworks that help: making future selves more vivid, projecting decisions to long-horizon vantage points, building institutional structures that create durable time horizons, and designing incentive systems that align decision-makers with future consequences.

The 10,000-year clock in a Texas mountain may seem like an eccentric art project. What it represents is more serious: the recognition that civilization's hardest problems are the ones where the rewards for getting it right are most visible to people who are not yet born.

Key References

- Kahneman, D., & Tversky, A. (1979). Prospect theory: An analysis of decision under risk. Econometrica, 47(2), 263-291.

- Laibson, D. (1997). Golden eggs and hyperbolic discounting. Quarterly Journal of Economics, 112(2), 443-478.

- Ersner-Hershfield, H., Garton, M. T., Ballard, K., Samanez-Larkin, G. R., & Knutson, B. (2009). Don't stop thinking about tomorrow: Individual differences in future self-continuity account for saving. Judgment and Decision Making, 4(4), 280-286.

- Frederick, S., Loewenstein, G., & O'Donoghue, T. (2002). Time discounting and time preference: A critical review. Journal of Economic Literature, 40(2), 351-401.

- Barton, D., Manyika, J., & Williamson, S. K. (2017). Where companies with a long-term view outperform their peers. McKinsey Global Institute.

- Stern, N. (2006). The Stern Review on the Economics of Climate Change. HM Treasury.

- Klein, G. (2007, September). Performing a project premortem. Harvard Business Review.

- O'Donoghue, T., & Rabin, M. (1999). Doing it now or later. American Economic Review, 89(1), 103-124.

Frequently Asked Questions

What is long-term thinking?

Long-term thinking is the practice of making decisions that weigh consequences over years or decades, not just immediate outcomes. It involves accurately estimating future states, discounting them less severely than our instincts suggest, and building commitments that protect future options. Long-term thinkers ask not just ‘what does this gain me now?’ but ‘what future does this make more or less likely?’

Why is long-term thinking so difficult?

The primary reason is hyperbolic discounting, a deeply ingrained neurological bias in which the brain heavily devalues rewards that arrive in the future compared to equivalent rewards available now. Brain imaging studies show that thinking about the future self activates neural patterns similar to thinking about a stranger, not oneself. This psychological distance from our future selves makes long-term consequences feel abstract and unreal compared to immediate gains.

What is Jeff Bezos's regret minimization framework?

Jeff Bezos’s regret minimization framework is a decision heuristic he described when explaining his choice to leave a Wall Street job to start Amazon. He imagined himself at age 80 looking back at his life and asked which choice he would regret more. He concluded he would not regret trying and failing, but would deeply regret never trying. The framework helps overcome short-term fear by shifting perspective to the long run, where inaction often causes more regret than action.

What are Stewart Brand's pace layers?

Stewart Brand’s pace layers framework, introduced in ‘The Clock of the Long Now,’ describes civilization as composed of six nested layers that change at different rates: fashion and art change fastest, followed by commerce, infrastructure, governance, culture, and nature, which changes slowest. The model explains why fast-moving layers often create disruption when they run ahead of slower layers that provide stability. It provides a framework for thinking about where durable change must happen versus where surface-level change is temporary.

What institutions enable long-term thinking?

Effective long-term institutions share several features: they have long time horizons built into their structure (endowments, hundred-year plans), they use mechanisms like constitutional protections that insulate decisions from short-term political pressure, and they create accountability across generations. Examples include university endowment management, Japan’s multi-century family firms (shinise), sovereign wealth funds like Norway’s Government Pension Fund, and constitutional amendments designed to be difficult to reverse.