In 2005, a researcher at the University of Iowa asked participants in a card game to make a series of bets. All players were given $20 and shown four decks of cards. Some cards awarded money; others caused losses.

Unknown to the players, two decks were rigged to produce frequent small gains and occasional catastrophic losses. The other two decks had frequent small losses but occasional large wins, a better expected outcome overall.

Normal participants began avoiding the rigged decks before they could consciously explain why. Their palms would sweat when they reached for a bad deck, a physiological signal registered before the mind caught up.

But patients with damage to the ventromedial prefrontal cortex, a brain region involved in integrating emotion with decision-making, kept reaching for the bad decks even after they intellectually understood the odds. They had the information.

They lacked the emotional signal that makes information actionable.

This Iowa Gambling Task revealed something profound: good financial decision-making is not purely a matter of information or intelligence. It depends on emotional processing, on the integration of past experience into present choice, and on systems of the brain that most of us never consciously control.

The psychology of money is the study of exactly this: how our emotions, mental shortcuts, social environment, and personal history shape the financial decisions we make, often far more powerfully than any spreadsheet or rational calculation.

"Doing well with money has a little to do with how smart you are and a lot to do with how you behave. And behavior is hard to teach, even to really smart people.", Morgan Housel, The Psychology of Money (2020)

Key Definitions

Behavioral finance, The field that combines psychology and economics to explain why people make financial decisions that diverge from the predictions of classical economic theory.

Where standard economics assumed rational, self-interested actors optimizing expected utility, behavioral finance studies the predictable ways that cognition and emotion cause systematic deviations from rationality.

Prospect theory, The foundational theory of behavioral finance, developed by Daniel Kahneman and Amos Tversky (1979), which describes how people actually evaluate gains and losses. The central finding: losses loom roughly twice as large as equivalent gains, losing $100 feels approximately as bad as gaining $200 feels good.

People are risk-averse when facing potential gains and risk-seeking when facing potential losses. This explains behaviors that standard utility theory cannot.

Loss aversion, The specific tendency, established by Kahneman and Tversky, to weigh potential losses more heavily than equivalent potential gains. A powerful force in investing behavior, contract design, and everyday spending.

Mental accounting, Richard Thaler's term for the cognitive practice of assigning money to separate mental "accounts" based on its source or intended use, then treating those accounts differently even though fungibility means all dollars are equivalent.

Status goods, Goods purchased primarily to signal social position or relative standing rather than for their intrinsic utility. Economist Thorstein Veblen introduced the term "conspicuous consumption" in 1899 to describe the purchase of expensive goods specifically to display wealth.

Recency bias, The cognitive tendency to overweight recent events and underweight the broader historical record when making predictions.

In financial contexts, investors who experienced the 2008 financial crisis were more risk-averse for years afterward, even in rising markets, because recent dramatic losses dominate the experiential record.

Anchoring, The tendency to rely heavily on the first piece of information encountered (the "anchor") when making decisions. In financial negotiations and investment decisions, initial prices, valuations, or reference numbers disproportionately influence subsequent judgments, even when they are arbitrary.

The Behavioral Finance Revolution

Before behavioral finance, the dominant framework for financial decision-making was expected utility theory, the model that rational agents maximize the expected value of outcomes weighted by their probability. This model made clean mathematical predictions but routinely failed to describe actual human behavior.

The revolution began with Maurice Allais's 1953 paradox, a pair of choices that demonstrated systematic violations of expected utility theory, and accelerated with Daniel Kahneman and Amos Tversky's program of research in the 1970s and 1980s.

Their 1979 paper "Prospect Theory: An Analysis of Decision Under Risk" in Econometrica is the most cited academic paper in economics, with over 70,000 citations.

It replaced expected utility theory with a descriptive account of how people actually evaluate prospects, one that incorporated loss aversion, reference dependence, and probability weighting.

Richard Thaler extended this work into practical financial behavior through the 1980s and 1990s, developing mental accounting theory, the endowment effect, and the "save more tomorrow" program. Thaler won the Nobel Prize in Economics in 2017 for these contributions.

Robert Shiller, who won the Nobel Prize in 2013, demonstrated that stock market prices show far more volatility than fundamental value models can explain, a finding attributable to the emotional amplification and herd behavior that behavioral finance documents.

The implications extended beyond academic theory. By the early 2000s, behavioral finance insights were reshaping pension policy (through automatic enrollment and default contribution rates), consumer protection regulation, and the design of financial products.

Behavioral economics is now a standard component of policy design in governments across Europe, North America, and Asia.

Loss Aversion: The Fear That Drives Bad Investing

Loss aversion is one of the most replicated findings in behavioral science. In the laboratory, most people reject a coin flip that pays $110 if heads and loses $100 if tails, they require a winning payoff of roughly $200 to accept an equal chance of losing $100.

The ratio is not constant, but the asymmetry is universal and appears across cultures, age groups, and levels of financial sophistication.

In investing, loss aversion produces a well-documented pattern of costly mistakes.

The disposition effect is the tendency to sell winning investments too early (to lock in gains and avoid the possibility of those gains being lost) and hold losing investments too long (to avoid realizing a loss and making it "real").

Terrance Odean studied 10,000 trading accounts and found that investors systematically sold their winners and held their losers, a strategy that produced lower returns than simply holding or selling the losing positions.

Odean and Brad Barber's subsequent research, published in the Journal of Finance (2000), found that frequent traders dramatically underperformed infrequent traders and the market index, after controlling for transaction costs.

The most active quartile of traders earned annual returns approximately 6.5 percentage points lower than the market.

The mechanism is loss aversion combined with overconfidence: frequent traders believe their judgment adds value, but the emotional pattern of selling winners and holding losers systematically destroys it.

Myopic loss aversion describes why investors check their portfolios too frequently. The more often you check, the more often you will observe a loss, even in a rising market, daily fluctuations produce losses roughly half the time. Each observed loss triggers a pain response.

Shlomo Benartzi and Richard Thaler demonstrated that investors who received annual performance evaluations were willing to hold significantly more equities (and earn higher long-term returns) than investors who received monthly evaluations, simply because less frequent observation meant fewer painful loss experiences.

Flight to safety in downturns is perhaps loss aversion's most expensive consequence. When markets decline sharply, investors sell equities and move to cash or bonds, exactly the opposite of what long-term wealth building requires. They sell low out of fear.

When markets recover and the pain recedes, they buy back in near the peak. Buy high, sell low.

| Loss Aversion Effect | Behavior | Financial Consequence |

|---|---|---|

| Disposition effect | Sell winners, hold losers | Portfolio drag vs. buy-and-hold |

| Myopic loss aversion | Check portfolio too often | More emotional selling at lows |

| Nominal loss aversion | Fear of any paper loss | Overweighting stable, low-return assets |

| Flight to safety | Sell equities in downturns | Buying high, selling low |

| Status quo bias | Avoid rebalancing | Drift from target allocation |

| Endowment effect | Overvalue things you own | Holding underperforming assets |

Mental Accounting: Why Not All Money Is Equal in Your Mind

Richard Thaler's mental accounting framework describes a set of cognitive operations that violate basic economic principles but are extremely common in human financial behavior.

Windfall spending is the clearest example. People spend "found" money, a tax refund, a work bonus, a gambling win, an inheritance, more freely than equivalent money earned through regular wages, even though the dollars are perfectly fungible.

A family that would never take an expensive vacation on regular savings will spend a tax refund on exactly that vacation, thinking of it as "extra" money rather than money they would otherwise have saved. Research consistently shows that windfall money is saved at significantly lower rates than wage income.

Amos Tversky and Richard Thaler's studies on mental accounting found that people treated money differently based on its source even when the amounts were identical. A $200 windfall was spent; $200 in earned income was saved.

A $200 loss felt worse when it came from "savings" than when it came from "entertainment budget," even when the underlying financial picture was identical. The label assigned to money in the mental accounting system determines its fate.

Earmarking is the flip side: people maintain rigid mental accounts for specific purposes and refuse to mix them, even when mixing would be rational.

A household might carry $5,000 in credit card debt at 20% interest while simultaneously maintaining a $5,000 "emergency fund" earning 1%, a clear net loss, because the emergency fund feels like a different kind of money that cannot be used to pay down debt.

Sunk cost fallacy operates through mental accounting: because money has already been "spent" in a mental account, we continue investing to feel we are getting value from that account, even when the rational choice is to stop. You keep watching a bad movie because you paid for the ticket.

You stay in a failing project because you have already spent months on it. The sunk cost is gone regardless of your choice; only future costs and benefits should matter, but the pain of writing off the mental account is real.

House money effect describes increased risk-taking with money already won in the same session. Casino gamblers play more aggressively after a winning streak; investors take more risk with portfolio gains than with original capital, even though the portfolio gains are equally their money.

The label in the mental account, "house money" vs. "my real money", changes behavior.

The Endowment Effect

Related to mental accounting, the endowment effect (Thaler, 1980; Kahneman, Knetsch, and Thaler, 1990) is the tendency to value things more highly simply because you own them.

In classic experiments, participants randomly assigned a coffee mug demanded approximately twice as much money to sell it as other participants were willing to pay to buy an identical mug. The act of ownership inflated perceived value.

In financial contexts, the endowment effect explains why investors hold appreciated assets they would never buy at current prices, and why homeowners systematically overestimate the market value of their homes.

The owned asset has been incorporated into the self, selling it triggers loss aversion even when the financial rationale for selling is clear.

Status Spending and the Social Dimension of Money

Morgan Housel observes that most people do not desire wealth so much as they desire what wealth signals to others. The desire is not for a $100,000 car, it is for the admiration and status the car is assumed to confer.

This conflation of wealth with its signals leads to a specific and costly error: spending money on visible status signals reduces the accumulation of actual wealth.

Thorstein Veblen's classic analysis identified this pattern in the gilded age of American capitalism, and it has not changed. Luxury car sales, designer goods, oversized houses, and expensive watches are largely purchased for their signaling value, what they communicate about the buyer to an audience of observers.

Robert Frank's research on "expenditure cascades" shows that this is not simply individual vanity. When top earners in a community spend more on houses, cars, and weddings, the reference group for everyone below shifts upward.

Middle-income households spend more to maintain relative position, often financed by reduced saving and increased debt. The effect cascades down the income distribution. Everyone is running harder to stand in the same relative place.

The irony Housel identifies: when someone drives an expensive car past you, you probably do not think about how impressive the driver is. You think about how impressive you would look in that car. The social signal the owner hoped to send is largely not received.

People use wealth to buy admiration, but wealth is admired in the abstract, not in the specific instance of its display.

The "Keeping Up With the Joneses" Effect: Research Evidence

Economists Erzo Luttmer (2005) and Andrew Clark and Andrew Oswald (1996) have produced influential research on relative income and subjective well-being. Their findings consistently show that happiness is more closely related to income relative to one's reference group than to absolute income level.

Luttmer's analysis of the National Survey of Families and Households found that a $1 increase in neighbors' income reduced self-reported happiness by approximately as much as a $1 reduction in one's own income, a striking demonstration that social comparison, not absolute standard of living, drives much of the dissatisfaction that motivates status spending.

Robert Frank's research, extended in Luxury Fever (1999), documents how this comparison dynamic operates at the household level through financial choices.

Higher-income households set the norm for wedding spending, car purchasing, and housing, which cascades down through the income distribution as each group attempts to maintain relative position.

Frank calculates that expenditure cascades have resulted in the median American household spending substantially more on status goods and substantially less on safety, time, and financial security than they would if their social comparison reference group had not shifted.

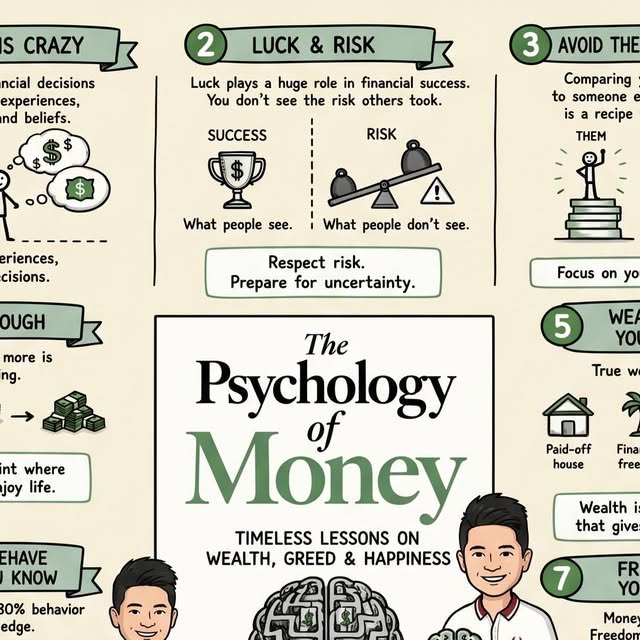

Luck vs. Skill: The Uncomfortable Truth About Financial Success

One of Morgan Housel's most important observations in The Psychology of Money concerns the role of luck in financial outcomes, a topic that wealthy people, financial media, and success narratives systematically underweight.

The year you were born matters enormously. An American who graduated from college in 1982 and entered the workforce as the longest bull market in history began inflated their 401(k) through a 17-year expansion.

An equally intelligent, equally hardworking person who graduated in 1929 or 2001 or 2007 faced a very different early-career trajectory. The stock of luck accumulated in someone's early wealth-building years compounds just as financial capital does.

This is not fatalism. What Housel argues, and what behavioral finance research supports, is calibration: recognizing that individual outcomes in financial markets depend heavily on factors outside any individual's control allows more accurate attribution of success and failure, reduces the tendency to copy others' specific strategies when their results partly reflect luck, and encourages humility in financial advice-giving.

The richest person at a casino is not necessarily the best gambler. The richest investor in a bull market is not necessarily the most skilled analyst. The distinction between skill and luck-amplified-skill is extremely difficult to observe in a single lifetime of outcomes.

"Bill Gates once said that success is a lousy teacher. It seduces smart people into thinking they can't lose. But in investing, nothing fails like success. When a strategy has worked, you double down on it. Sometimes, that's right. Sometimes it's just continuation of luck.", Morgan Housel

Survivorship Bias in Financial Success Stories

The psychological literature on survivorship bias, the systematic error of focusing on successful outcomes and ignoring failures, is directly relevant to financial decision-making.

Nassim Taleb, in The Black Swan (2007), points out that financial literature and financial media overwhelmingly document the strategies of successful investors, while the far larger population of investors who used the same strategies and failed is invisible.

Research by Hendrik Bessembinder (2018) in the Journal of Financial Economics found that of all US stocks from 1926 to 2016, only 42% outperformed Treasury bills over their lifetimes. The entire net wealth creation of the US stock market was generated by fewer than 4% of listed companies.

The typical stock was a disappointing investment; the exceptional few created the returns that retrospectively validated "investing in stocks" as a strategy.

The practical implication is that the strategy narratives constructed from successful outcomes, "I invested in tech stocks and got rich", are systematically misleading guides to future behavior, because they sample only from the successful end of a distribution that was shaped substantially by chance.

Behavioral finance researchers recommend explicit accounting for base rates and counterfactuals when evaluating any financial strategy or narrative.

The Difference Between Being Rich and Being Wealthy

The most counterintuitive insight in the psychology of money literature is the distinction between income and wealth, between appearing prosperous and actually accumulating financial security.

A person earning $500,000 per year who spends $490,000 is rich in the technical sense of high income. But they have almost no financial resilience: one job loss, one medical crisis, one recession means crisis.

Wealth, in the sense Housel defines it, is money not spent, it is the savings rate, not the income level, that determines financial security.

Visible consumption signals current income, not accumulated wealth. The most financially secure people in any neighborhood may be those driving 12-year-old cars and taking modest vacations, quietly accumulating in index funds.

The most financially fragile may be driving new luxury vehicles and posting vacation photos, appearances maintained by debt and the absence of any buffer.

Research on lottery winners illustrates this distinction. Studies of lottery winners in the US and UK find that within three to five years, a substantial proportion are in worse financial shape than before their windfall.

Jay Zagorsky's (2003) study in the Review of Income and Wealth found that lottery winners were not significantly wealthier than control groups five years after winning, because spending increased to match the windfall.

Large sudden income, without the habits and frameworks of wealth accumulation, is spent rather than converted into lasting financial security.

The Savings Rate as the True Measure

Thomas Stanley and William Danko's landmark study The Millionaire Next Door (1996) surveyed individuals with net worth over $1 million and found that the majority did not live in expensive neighborhoods, drive luxury cars, or wear designer clothing.

The modal millionaire was a small business owner living in a modest home, driving a domestic vehicle, and maintaining a high savings rate over decades.

The book's central finding was that wealth accumulation was strongly predicted not by income but by the ratio of net worth to income, what Stanley called the "wealth accumulation factor", which was higher among individuals who lived well below their income and lower among those who conspicuously consumed.

This finding aligns with behavioral finance research showing that savings rate, the proportion of income not spent, is the single most controllable variable in long-term wealth outcomes.

Unlike investment returns, which are partially determined by market conditions outside any individual's control, savings rate is directly responsive to behavioral decisions.

A 2021 analysis by Vanguard found that increasing the savings rate by 1 percentage point produced a more reliable long-term wealth effect than any equally achievable improvement in investment returns.

What Behavioral Finance Tells Us About Practical Money Decisions

The research on financial psychology converges on several practical implications:

Automate to remove emotion from the decision loop. Automatic payroll deductions for retirement accounts remove the decision from the domain where loss aversion can interfere.

Richard Thaler and Shlomo Benartzi's "Save More Tomorrow" program found that employees who pre-committed to saving a portion of future raises dramatically increased their savings rates without ever consciously choosing to sacrifice current spending.

In the original study, published in the Journal of Political Economy (2004), the average savings rate of participants increased from 3.5% to 13.6% over 40 months, a nearly fourfold increase achieved not through discipline but through commitment architecture.

Check investment performance less often. Quarterly or annual reviews rather than daily or weekly monitoring reduces the number of times you observe short-term losses and reduces the emotional pressure to act on them.

Long-term investors who check daily essentially experience a different asset class than those who check annually, because daily checking produces a much higher frequency of apparent losses.

Recognize windfall money as real money. Tax refunds, bonuses, and gifts are not "extra" money separate from your finances, they are part of your financial picture and respond to the same logic as regular income.

Treating them as such rather than spending them as found money can substantially increase net savings rates over time.

Separate investment accounts from mental accounts. The practice of earmarking money into separate labeled accounts, "vacation fund," "emergency fund," "investment account", while psychologically comforting, can create inefficiencies.

The rational approach evaluates the whole balance sheet, using high-cost debt payoff before low-return savings.

Define "enough." Without a clear personal definition of what financial security looks like, the target perpetually recedes as income grows. Research on hedonic adaptation shows that income increases produce only temporary improvements in wellbeing before the new level becomes the reference point.

Defining what "enough" means, in concrete terms, for your actual life, before spending decisions, rather than after, is one of the most financially protective psychological strategies available.

Summary Table: Key Behavioral Finance Concepts

| Concept | Definition | Financial Behavior It Explains |

|---|---|---|

| Loss aversion | Losses feel ~2x as painful as equivalent gains feel pleasurable | Selling winners too early; holding losers too long |

| Mental accounting | Treating money differently based on source or label | Windfall spending; earmarking inefficiencies |

| Sunk cost fallacy | Factoring already-spent money into current decisions | Continuing bad investments to avoid "realizing" a loss |

| Status spending | Purchasing visible goods to signal position | Consuming rather than accumulating wealth |

| Planning bias | Overconfidence in future financial plans | Underpreparing for emergencies |

| Recency bias | Weighting recent events too heavily in predictions | Buying at market peaks; selling at troughs |

| Herd behavior | Following others' financial decisions under uncertainty | Buying assets at inflated prices during manias |

| Anchoring | Over-relying on initial price as reference point | Refusing to sell below purchase price; misjudging "discounts" |

| Overconfidence | Overestimating skill relative to luck | Excessive trading; underdiversification |

| Present bias | Overvaluing the immediate present vs. future | Undersaving; overspending on immediate consumption |

Money, Childhood, and the Formative Money Scripts

One dimension of the psychology of money that Morgan Housel and behavioral economists address only partially is the developmental origin of financial beliefs and behaviors.

Brad Klontz, a financial psychologist at Creighton University, has developed the concept of money scripts, the core beliefs about money formed in childhood and carried, often unconsciously, into adult financial decisions.

Klontz and colleagues (2011) identified four money script clusters through factor analysis of a large sample: money avoidance (money is bad, corrupt, or dangerous), money worship (more money will solve problems and produce happiness), money status (self-worth equals net worth), and money vigilance (money must be saved and protected at all costs).

Each cluster is associated with distinct financial behavior patterns and mental health outcomes.

Money avoidance is associated with giving money away impulsively, being financially self-sabotaging, and having negative beliefs about wealth. Money worship predicts compulsive spending, hoarding, and chronic financial dependence. Money status correlates with overspending, lying about finances, and dependent relationships with money.

Money vigilance, the most financially "adaptive" script, is associated with higher savings rates and less financial risk-taking, but also financial anxiety and difficulty enjoying money.

The key finding is that these scripts operate largely outside conscious awareness.

People do not typically choose to believe that "money is evil" or that "I don't deserve financial security", they have absorbed these beliefs from parental behavior, family financial events (bankruptcy, sudden wealth, depression-era scarcity), and cultural context, and they act on them habitually without interrogating the underlying belief.

Financial therapy, which combines financial planning with psychological exploration of money beliefs, addresses this layer of the problem.

The Larger Picture

Money is not just an economic variable. It is loaded with meaning, about security, freedom, status, identity, generosity, and fear.

The psychological relationship people have with money is shaped by childhood experiences with scarcity or abundance, cultural messages about what wealth means, the comparison group they see themselves embedded in, and the stories they tell themselves about whether they deserve to be financially secure.

Morgan Housel's core thesis, and the thesis of behavioral finance more broadly, is not that people are irrational and should be replaced by algorithms. It is that human financial behavior is predictably, systematically influenced by forces that are not captured in traditional economic models.

Understanding those forces is the first step toward designing better personal financial systems, better policy interventions, and a more honest relationship with money and what it can and cannot do for a human life.

The science is clear on one practical point: financial outcomes depend less on intelligence or information than on behavior sustained over time. And behavior is governed not by what we know but by what we feel, by the emotions and mental frameworks that this field is, slowly, beginning to map.

Further Reading

- Housel, M. (2020). The Psychology of Money: Timeless Lessons on Wealth, Greed, and Happiness. Harriman House.

- Kahneman, D. (2011). Thinking, Fast and Slow. Farrar, Straus and Giroux.

- Thaler, R. H., & Sunstein, C. R. (2008). Nudge: Improving Decisions About Health, Wealth, and Happiness. Yale University Press.

- Kahneman, D., & Tversky, A. (1979). Prospect theory: An analysis of decision under risk. Econometrica, 47(2), 263-292.

- Thaler, R. H. (1985). Mental accounting and consumer choice. Marketing Science, 4(3), 199-214.

- Odean, T. (1998). Are investors reluctant to realize their losses? Journal of Finance, 53(5), 1775-1798.

- Benartzi, S., & Thaler, R. H. (1995). Myopic loss aversion and the equity premium puzzle. Quarterly Journal of Economics, 110(1), 73-92.

- Frank, R. H. (1999). Luxury Fever: Why Money Fails to Satisfy in an Era of Excess. Free Press.

- Stanley, T. J., & Danko, W. D. (1996). The Millionaire Next Door. Longstreet Press.

- Klontz, B., Britt, S. L., Mentzer, J., & Klontz, T. (2011). Money beliefs and financial behaviors: Development of the Klontz Money Script Inventory. Journal of Financial Therapy, 2(1), 1-22.

- Taleb, N. N. (2007). The Black Swan: The Impact of the Highly Improbable. Random House.

- Luttmer, E. F. P. (2005). Neighbors as negatives: Relative earnings and well-being. Quarterly Journal of Economics, 120(3), 963-1002.

Frequently Asked Questions

What is the psychology of money?

The psychology of money is the study of how emotions, cognitive biases, and social forces shape financial decisions. People do not make financial choices based on pure calculation, they are influenced by fear, status, identity, past experiences, and systematic thinking errors that often work against their long-term financial interests.

What is loss aversion in investing?

Loss aversion is the tendency to feel the pain of a financial loss roughly twice as intensely as the pleasure of an equivalent gain, a finding established by Daniel Kahneman and Amos Tversky in prospect theory. In investing, this leads people to sell winning positions too early to lock in gains and hold losing positions too long to avoid realizing a loss, the opposite of rational wealth-building behavior.

What is mental accounting?

Mental accounting, a concept developed by economist Richard Thaler, is the tendency to treat money differently depending on where it came from or what it is mentally earmarked for. People spend windfall money (a tax refund, a work bonus) more freely than earned wages, even though a dollar is a dollar regardless of its source. This leads to predictably irrational spending and saving decisions.

What is the difference between being rich and being wealthy?

Morgan Housel, in The Psychology of Money, draws this distinction clearly: being rich means having a high current income or visible spending, while being wealthy means having accumulated assets that are not spent. Many high-earning people appear rich but have little wealth because they convert income into visible consumption. True wealth is often invisible, it is the car not bought, the lifestyle not inflated.

How does luck affect financial outcomes?

Research and historical analysis show that individual financial outcomes are substantially shaped by luck, the country and era you were born in, the economic cycle that greeted you when you entered the workforce, whether a crisis hit at an early or late stage of your career. Morgan Housel argues that acknowledging luck is not defeatist but clarifying: it reduces the temptation to attribute others’ success purely to skill and your own failures purely to bad character.