Credit is one of those financial tools that is nearly invisible when it is working well and enormously disruptive when it is not. A good credit score can save tens of thousands of dollars over a lifetime in lower interest rates on mortgages, car loans, and personal loans.

It affects whether you can rent an apartment, the deposit required for utilities, and increasingly, even job applications in financial industries.

Yet millions of people, particularly young adults, recent immigrants, and those recovering from financial hardship, find themselves in a frustrating bind: you need credit to build credit.

This guide explains how the credit scoring system actually works, what specifically determines your score, and how to build a strong credit history efficiently from any starting point.

The Real Stakes: Why Credit Scores Matter Financially

Before diving into mechanics, it's worth quantifying what good versus poor credit actually costs. The financial consequences of credit scores are substantial and compound over a lifetime.

Consider a 30-year fixed mortgage on a $350,000 home in a typical interest rate environment. According to data from FICO's loan savings calculator, the difference in interest rate between a borrower with a score of 760-850 and one with a score of 620-639 is typically 1.5-2.0 percentage points.

On a $350,000 mortgage, that difference in rate translates to approximately $350-$430 per month in additional interest payments, over $126,000 over the life of the loan. That is entirely avoidable cost, determined purely by credit score.

Beyond mortgages, the Consumer Financial Protection Bureau (CFPB) has documented that consumers with poor credit pay higher insurance premiums (in states that permit credit-based insurance scoring), face higher deposit requirements for utilities and housing, and are denied employment in financial services roles at rates that reflect credit history checks.

A 2020 CFPB report found that approximately 26 million Americans are "credit invisible", having no credit file at all, and another 19 million have files too thin or stale to generate a score.

These 45 million people face systematically worse financial terms across virtually every financial product they access.

How Credit Scores Work

Your credit score is a three-digit number, typically between 300 and 850, that summarizes your creditworthiness from the perspective of lenders. The most widely used scoring model is the FICO score, developed by the Fair Isaac Corporation and first introduced in 1989.

VantageScore is a competing model developed jointly by the three major credit bureaus in 2006, now used by some lenders, but FICO remains the industry standard for most mortgage and major loan decisions.

Approximately 90% of top lenders use FICO scores in their underwriting decisions, according to FICO's own reporting. There are actually multiple FICO score versions (FICO 8, FICO 9, FICO 10) and industry-specific scores (FICO Auto Score, FICO Bankcard Score), but the general factors and weights are similar across versions.

Your FICO score is calculated from information in your credit report, which is maintained by three credit bureaus: Equifax, Experian, and TransUnion.

Lenders who extend you credit (banks, credit card companies, auto lenders) report your account activity to these bureaus, which compile it into your report. Your score is then calculated from that report data.

The Five Factors of Your FICO Score

| Factor | Weight | What It Measures |

|---|---|---|

| Payment history | 35% | Whether you pay on time |

| Credit utilization | 30% | How much of your available credit you use |

| Length of credit history | 15% | Age of your oldest, newest, and average accounts |

| Credit mix | 10% | Variety of account types (cards, loans, mortgage) |

| New credit | 10% | Recent applications and hard inquiries |

Payment history and credit utilization together account for 65% of your score. Everything else is secondary. If you pay on time and keep balances low, you will build good credit, full stop.

It is important to understand that FICO scores are recalculated each time a lender pulls your report, they are not static numbers stored in a database, but calculations run on the current state of your credit file. This means scores can change month to month as new information is reported.

What the Score Ranges Mean

| Score Range | Category | Typical Impact |

|---|---|---|

| 800-850 | Exceptional | Best available rates on all products |

| 740-799 | Very Good | Near-best rates, easy approvals |

| 670-739 | Good | Approved for most products at standard rates |

| 580-669 | Fair | Higher rates, some denials, deposits required |

| 300-579 | Poor | Most credit denied; secured products only |

The distribution of American credit scores, according to Experian's 2023 State of Credit report, shows median FICO scores around 714 for the general population.

Average scores vary significantly by state, Minnesota residents average around 742, while Mississippi residents average around 681, reflecting differences in income levels, credit access history, and financial education.

Average scores have risen approximately 14 points over the past decade, largely attributed to consumer education, wider access to free credit monitoring, and changes in how medical debt is reported.

The Three Major Credit Bureaus: What You Need to Know

The three bureaus, Equifax, Experian, and TransUnion, operate independently and competitively. They collect the same general types of data but there is no requirement that lenders report to all three, and the data in your reports can differ between bureaus.

This creates a practical complication: you may have a significantly different score from each bureau. Lenders applying for mortgages will typically pull all three scores and use the middle score. Credit card issuers may pull only one bureau.

An error or missing account at one bureau can affect your score with lenders who use that bureau, even if the other two bureaus show clean records.

FICO calculates separate scores from each bureau's data. It is entirely normal and common to have three different FICO scores, sometimes differing by 20-50 points, not because of scoring model differences but because the underlying data in each bureau file is different.

The implication: monitoring only one bureau's score gives you an incomplete picture. You are entitled to one free report from each bureau annually through AnnualCreditReport.com (mandated by the Fair and Accurate Credit Transactions Act of 2003, or FACTA).

During the COVID-19 pandemic, the bureaus extended free weekly reports; as of 2024, weekly free reports remain available through AnnualCreditReport.com.

Starting From Zero: The Thin File Problem

If you have never had a credit account, you have what the industry calls a thin file, too little history to generate a reliable score. Lenders cannot assess your risk because there is no track record.

FICO requires at least one account open for six months and at least one creditor reporting within the past six months before it can generate a score.

The 26 million "credit invisible" Americans documented by the CFPB disproportionately include young adults under 25, recent immigrants, and lower-income individuals who have primarily used cash and debit.

They are not financially irresponsible, they simply have not participated in the credit system in ways that generate reportable history.

The good news is that thin files respond quickly to the right moves. A person with no credit history can have a scoreable file within 60 days and a decent score within six months by taking the right steps.

An important recent development: FICO and VantageScore have introduced alternative data models that can score credit-invisible consumers using bank account transaction data, rent payment history, and utility payment history.

FICO's UltraFICO score and Experian Boost both offer mechanisms for consumers to add this data to their credit assessment.

Experian Boost, launched in 2019, allows consumers to add positive payment history from utility, phone, and streaming services directly to their Experian credit file.

According to Experian's data, users who add this data and have thin or fair-credit files see an average score increase of 12-14 points, with some consumers becoming scoreable for the first time.

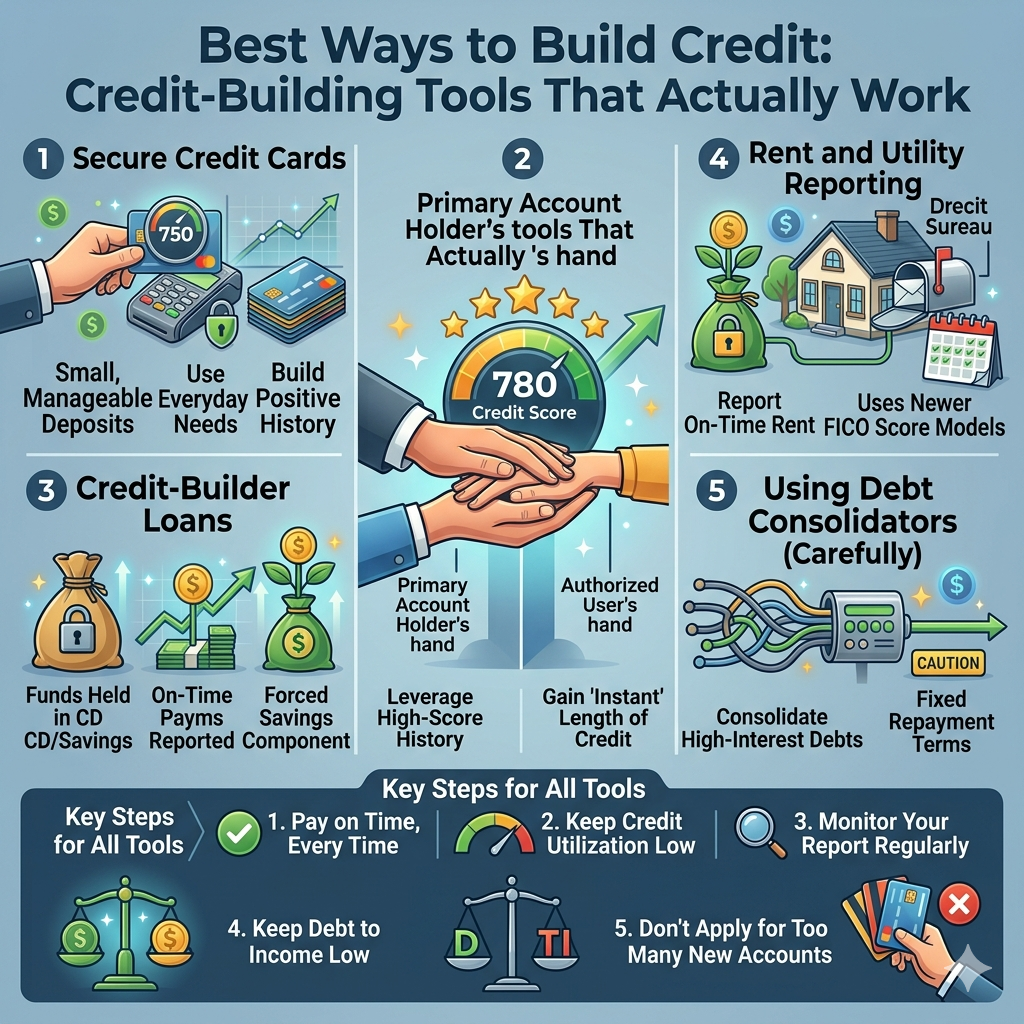

Strategy 1: Become an Authorized User

The fastest path to a credit score for someone starting from zero is becoming an authorized user on someone else's credit card account, typically a parent, spouse, or close family member with a well-established, responsibly managed account.

When you are added as an authorized user, the primary account's entire history on that card can appear on your credit report. If the primary cardholder has had a card for ten years with perfect payment history, that ten-year history now also helps establish your credit profile.

You do not even need to use the card, or have the physical card at all.

This strategy requires a trusting relationship. If the primary cardholder carries a high balance, makes late payments, or defaults, that negative information will also appear on your report. Choose someone with excellent credit habits.

The authorized user approach works best as a starting point combined with other strategies below. It can get you a score quickly, but building your own independent credit history is the long-term goal.

Research supports the effectiveness of this strategy. A 2010 study by the Federal Reserve Board found that authorized user status accounts for approximately 10% of the predictive power of thin-file credit scores.

For credit-invisible consumers, authorized user accounts can be the difference between having no score and having a functional credit profile immediately.

There is a practice sometimes called "piggybacking credit" in which strangers pay to be added as authorized users to unrelated accounts, essentially renting someone else's credit history.

FICO took steps to reduce the scoring benefit of unrelated authorized user additions in later scoring models, but family-member authorized user relationships continue to function as intended.

Strategy 2: Open a Secured Credit Card

A secured credit card is a credit card backed by a cash deposit you make upfront. If you deposit $300, you typically have a $300 credit limit. The deposit protects the lender if you default, making secured cards accessible to people with no credit or damaged credit.

Secured cards function exactly like regular credit cards for credit-building purposes. The issuer reports your payment behavior to the credit bureaus every month. Use the card for small, routine purchases, a grocery run, a streaming subscription, and pay the balance in full every month.

What to look for in a secured card:

- No annual fee (several issuers offer fee-free secured cards)

- Reports to all three major credit bureaus (some only report to one or two)

- Clear upgrade path to an unsecured card after 12-18 months

- Minimal additional fees (look for cards without monthly maintenance fees)

- Interest rate is less important if you pay in full every month, but matters if you ever carry a balance

Issuers like Discover, Capital One, and many credit unions offer competitive secured card products. After 12 to 18 months of responsible use, most issuers will upgrade you to an unsecured card and return your deposit, often without requiring a new application.

The Discover it Secured card, in particular, is frequently recommended by consumer financial educators because it has no annual fee, reports to all three bureaus, offers a clear graduation path to unsecured credit, and provides cash back rewards, unusual features for a secured product.

Capital One's secured card has a low minimum deposit ($49 or $99 for an initial $200 line, depending on credit profile) and also offers an upgrade path.

What to Avoid

Predatory secured cards: Some issuers charge excessive fees, annual fees of $75+, monthly maintenance fees, and processing fees that can consume much of your initial deposit before you even use the card. Read the full fee schedule before applying.

Cards with an all-in annual cost above $50 (including annual fee) are generally overpriced for what is a simple credit-building tool.

Store credit cards as first credit: Retail store cards are easy to obtain but typically have very high interest rates, low limits, and limited acceptance. They can help establish a credit history but are not ideal as your primary credit-building tool.

Strategy 3: Credit-Builder Loans

A credit-builder loan works in reverse from a traditional loan. Instead of receiving funds upfront and repaying them, you make monthly payments into a locked savings account. When the loan term ends, you receive the accumulated savings (minus fees and interest). The payment history is reported to the credit bureaus throughout the term.

Credit-builder loans are offered primarily by credit unions, community banks, and online lenders like Self (formerly Self Lender). They typically range from $300 to $1,500 with terms of 12 to 24 months. The monthly payment is usually $25 to $50.

The benefit is twofold: you build a positive payment history and add an installment account to your credit mix (which differs from revolving credit card accounts), both of which improve your score. The savings you accumulate at the end are a small bonus.

Research on credit-builder loans is favorable. A 2020 study by the Consumer Financial Protection Bureau found that credit-builder loans increased the likelihood of having a credit score by 24 percentage points for participants without existing debt, and improved scores by an average of 60 points for those who made all payments on time.

Importantly, the CFPB study found that participants with existing debt (who may have competing payment obligations) showed smaller or no benefits, suggesting that credit-builder loans work best as a standalone starting strategy rather than as an addition to a debt-heavy financial profile.

Strategy 4: Building With a Regular Credit Card

Once you have an initial credit history established through the steps above, you may qualify for entry-level unsecured credit cards. These typically come with low credit limits initially, which is fine, the limit is less important than the responsible use pattern.

The rules for credit card use that builds credit are simple:

- Pay on time, every time. Set up autopay for at least the minimum payment so you never miss a due date, even if you forget. Then pay the full balance separately before the due date.

- Keep utilization low. Using more than 30% of your available credit hurts your score. Using more than 50% hurts it substantially. Aim for under 10% utilization for the best scores.

- Do not close old accounts. Closing a credit card reduces your available credit (raising utilization) and can shorten your average account age. Keep old accounts open even if you rarely use them.

- Do not apply for many cards quickly. Each application triggers a hard inquiry. Multiple hard inquiries in a short period signal financial stress to scoring models.

Understanding Credit Utilization in Depth

Credit utilization deserves special attention because it is the most actionable factor for most people. Unlike payment history, which takes months to build, utilization can be changed quickly.

Your utilization is calculated at the moment your statement is generated, typically at the end of your billing cycle. If your card has a $1,000 limit and your statement shows a $600 balance, your utilization is 60%, even if you always pay the full balance by the due date.

The solution for people who regularly use a large portion of their limit is to pay down the balance before the statement date, not just before the due date. This ensures the lower balance gets reported to the bureaus.

Alternatively, requesting a credit limit increase (without increasing spending) immediately lowers your utilization percentage.

FICO calculates utilization both per card (each individual card's balance versus its limit) and in aggregate (total balances across all cards versus total limits). Even if your overall utilization is low, a single card at high utilization can negatively affect your score.

Spreading purchases across multiple cards, or paying down a heavily used card strategically before its statement date, can meaningfully improve scores even without changing total spending.

A common misconception is that utilization "memory" persists, in fact, utilization is calculated entirely from the current statement balance. If you had 90% utilization last month and 5% this month, your score reflects the 5% with no penalty for last month's high utilization.

This is why emergency credit use followed by quick repayment does not permanently damage your score.

Rent Reporting: A Growing Credit-Building Tool

Historically, one of the inequities in the credit system was that on-time rent payments, the largest monthly financial obligation for most Americans under 40, did not appear in credit files, while any late or missed payments could be reported as collections.

Renters were essentially making their largest payment every month with no credit benefit and substantial credit risk.

This has begun to change. Several services now report rent payments to credit bureaus:

- Experian RentBureau: Integrated into many property management software systems

- RentTrack, PayYourRent, Rental Kharma: Services that renters can sign up for independently

- Fannie Mae and Freddie Mac policy: Both GSEs updated underwriting guidelines in 2021-2022 to consider positive rent payment history in mortgage applications

Research by Experian found that adding 12 months of on-time rent payments to thin credit files improved average scores by approximately 21 points. For credit-invisible consumers, rent reporting can be the most natural and least costly path to initial credit scoring, since it simply records what they are already doing.

What Actually Counts as Good Credit Behavior

| Action | Effect on Score | Timeline |

|---|---|---|

| Paying on time for 12+ months | Strong positive impact | Gradual, cumulative |

| Keeping utilization below 10% | Immediate positive impact | Reflected in next cycle |

| Becoming an authorized user | Immediate positive (if account is good) | Within 30-60 days |

| Missing a payment | Significant negative impact | Can persist 7 years |

| Maxing out a card | Immediate negative impact | Reverses when balance drops |

| Applying for new credit | Small temporary drop | Recovers in 12 months |

| Closing an old account | Can lower score | Permanent history reduction |

| Opening a credit-builder loan | Adds installment mix, builds history | 12-24 month process |

| Adding rent via Experian Boost | Moderate positive, especially for thin files | Within one report cycle |

Common Credit Myths Debunked

Myth: Carrying a balance helps your credit score.False. You do not need to carry a balance or pay interest to build credit. Paying your full balance every month demonstrates responsible use while avoiding interest charges.

This myth persists because some people confuse "using the card" (which does help) with "carrying a balance" (which is unnecessary and costly).

Credit card companies may benefit from this myth spreading, they earn interest on carried balances. There is no mechanism in FICO's model by which carrying a balance provides scoring benefit over full payment.

Myth: Checking your credit hurts your score.False. Checking your own credit is a soft inquiry and has zero effect on your score.

Only hard inquiries, from lenders when you apply for credit, affect your score, and those effects are small (typically 5 points or less) and temporary (fading within 12 months and falling off your report entirely after 2 years).

Myth: Income affects your credit score.False. Your income does not appear on your credit report and is not factored into your FICO score. Lenders ask about income when evaluating loan applications, but income is irrelevant to the credit score calculation itself.

A high earner who never pays on time will have a worse score than a low earner with a perfect payment history.

Myth: Closing credit cards improves your score.Usually false, and often harmful. Closing a card reduces your total available credit (raising utilization) and may shorten your credit history (reducing the length factor).

Closed accounts remain on your report for up to ten years if the history was positive, but it is generally better to keep old accounts open.

Myth: Debit card use builds credit.False. Debit cards are linked to your bank account, not a credit account. Debit card transactions are not reported to credit bureaus and have no effect on your credit score.

Many consumers believe they are "building credit" by responsibly managing a debit card, they are not. Only credit accounts (credit cards, loans, lines of credit) generate the payment history that credit scores measure.

Myth: You only have one credit score.False. You have multiple scores from different scoring models and different bureaus. You have at least three FICO scores (one from each bureau's data), potentially multiple FICO score versions, and a separate VantageScore.

These can vary substantially. When a lender says they will "check your credit," ask which bureau and which scoring model they use.

Myth: Paying off a collection eliminates its impact.Partially false. Paying a collection account changes its status to "paid collection," which is more favorable under some newer scoring models (FICO 9 and VantageScore 3.0 and 4.0 ignore paid collections; FICO 8 does not).

But the collection itself remains on your report for seven years from the original delinquency date. The impact diminishes over time regardless of payment status.

How to Monitor Your Progress

You are entitled to one free credit report from each of the three bureaus annually (currently weekly) through AnnualCreditReport.com. Check all three because lenders do not always report to all three bureaus, and errors are surprisingly common.

A 2013 FTC study found that approximately 1 in 5 consumers had at least one verified error on their credit reports, and 1 in 20 had errors significant enough to affect their score materially.

Errors include incorrect personal information, accounts that don't belong to you (identity theft or bureau mix-up with a common name), incorrect payment status, and duplicate accounts.

Beyond annual checks, many credit card issuers and banks now offer free credit score monitoring as a feature. Services like Credit Karma provide free access to VantageScore-based scores pulled from Equifax and TransUnion. These are useful for tracking trends even if they do not reflect the exact FICO score a lender might pull.

When reviewing your report, look for:

- Incorrect personal information (name, address, Social Security number)

- Accounts you do not recognize (potential identity theft or error)

- Incorrect payment status on accounts

- Duplicate accounts

- Negative items approaching their 7-year removal date

Dispute errors directly with the relevant credit bureau. Under the Fair Credit Reporting Act (FCRA), bureaus must investigate disputes within 30 days and correct verified errors. The FTC provides detailed guidance on dispute processes.

For serious errors, consider disputing directly with the furnishing creditor (the lender who reported the error) in addition to the bureau, as the creditor has the original data and more ability to issue a correction.

Identity Theft and Credit Freezes

Identity theft is a significant and growing threat to credit health. The FTC received 1.4 million identity theft reports in 2021, up dramatically from prior years.

New account fraud, where a thief opens credit accounts in your name, is particularly damaging because it can go undetected for months while the accounts accumulate negative history.

A credit freeze (also called a security freeze) is free under federal law and is the most effective protection against new account fraud. A freeze prevents any new lenders from pulling your credit report, making it effectively impossible to open new credit in your name.

You can temporarily lift the freeze when you are applying for credit yourself.

You must freeze your report separately at each of the three major bureaus, plus potentially at other specialty consumer reporting agencies like ChexSystems (used by banks) and NCTUE (used by utilities and telecom companies). The process takes minutes at each bureau's website.

A fraud alert is a less restrictive option that requires lenders to take extra steps to verify your identity before opening new credit. Initial fraud alerts last 1 year; extended fraud alerts (for confirmed identity theft victims) last 7 years.

Rebuilding After Damaged Credit

If you are recovering from missed payments, a collection account, bankruptcy, or other negative marks, the path is the same as building from scratch, but patience is required because negative information persists.

Late payments stay on your credit report for seven years from the date of the first missed payment. However, their impact fades over time. A late payment from five years ago matters far less than one from six months ago.

FICO's scoring model weights recent payment history more heavily than older history, a late payment from last month has far more impact than one from three years ago.

Collection accounts also remain for seven years. Paying a collection account does not remove it from your report, but it changes the status to "paid collection," which newer FICO models treat more favorably.

Some collection agencies will negotiate a "pay for delete" agreement, paying the debt in exchange for them removing the tradeline entirely.

This is not required by law and not all agencies agree, but it is worth requesting, particularly for significant collection balances.

Bankruptcy stays on your report for 7 years (Chapter 13) or 10 years (Chapter 7). Credit scores typically recover significantly within two to three years after bankruptcy as new positive history accumulates.

A consistent finding in credit research is that the post-bankruptcy score recovery for consumers who immediately begin rebuilding (secured card, on-time payments) is faster than commonly assumed, many consumers can reach the 650-700 range within 2-3 years of a bankruptcy discharge.

The consistent strategy for rebuilding is: add positive information as quickly as possible, keep existing accounts in good standing, and let time do its work on the older negative marks.

The FICO Algorithm's Evolving Treatment of Medical Debt

Medical debt has historically been treated identically to other collection debt in credit scoring, a significant policy concern given that most medical debt arises from illness rather than financial irresponsibility. As of 2022-2023, significant changes have been made:

- FICO 9 and VantageScore 4.0 began treating paid medical collections differently from other paid collections, with reduced scoring impact

- The three major bureaus announced in 2022 that they would no longer include medical collections under $500 in credit reports

- Equifax, Experian, and TransUnion further announced they would remove all paid medical collections from reports by July 2022

- Unpaid medical collections under $500 are no longer reported as of 2023

The Consumer Financial Protection Bureau under Director Rohit Chopra proposed additional rules in 2024 that would remove medical debt from credit reports entirely, based on research showing medical debt is a poor predictor of creditworthiness. If implemented, these rules could improve credit scores for tens of millions of Americans.

A Realistic Timeline

For someone starting from zero with no derogatory history:

- Month 1-2: Become an authorized user; open a secured card or credit-builder loan; optionally add rent/utilities via Experian Boost

- Month 3-6: First credit score generated (usually 580-640 range)

- Month 6-12: Score likely reaches 640-680 with consistent on-time payments and low utilization

- Year 1-2: Score can reach 700+ with no negative marks and expanded credit mix

- Year 3-5: Excellent score (750+) becomes achievable with a strong, consistent track record

| Milestone | Typical Timeline | Required Actions |

|---|---|---|

| First credit score | 3-6 months | One account open 6 months with recent activity |

| "Fair" score (580+) | 6-9 months | On-time payments, low utilization |

| "Good" score (670+) | 12-18 months | Consistent history, low utilization, no negatives |

| "Very Good" score (740+) | 2-4 years | Long history, low utilization, credit mix |

| "Exceptional" score (800+) | 5-7+ years | Long history, very low utilization, excellent mix, no negatives |

Building credit is a slow process, but it is also a reliable one. The behaviors that produce good credit, paying on time, using credit modestly, avoiding unnecessary debt, are also simply good financial habits. The score is not the goal; it is the measure of habits that serve you well in far more ways than just the number.

The financial benefit of building strong credit is not marginal. For a 30-year-old who achieves an 800 credit score by age 35 and maintains it through homeownership, car purchases, and routine credit decisions, the lifetime financial benefit, in lower interest rates, lower insurance premiums, and eliminated deposit requirements, is credibly in the range of $150,000-$300,000 compared to a peer who drifts in the 620-650 range.

That is not a small prize for the disciplined practice of paying bills on time and keeping balances low.

Frequently Asked Questions

How long does it take to build good credit from scratch?

Building a credit score from no credit history typically takes three to six months to generate a scoreable file, and reaching a good score (670+) generally takes one to two years of consistent responsible behavior. Building an excellent score (750+) typically takes three to five years. The timeline depends on how many accounts you open, how responsibly you manage them, and whether any negative marks appear on your report.

What is the fastest way to build credit?

The fastest combination is becoming an authorized user on someone else’s well-managed account (which can add history immediately), opening a secured credit card, and making small charges you pay off in full each month. Getting a credit-builder loan from a credit union simultaneously adds an installment account to your mix. Most people with these three approaches in place have a scoreable file within 30 to 60 days and a decent score within six months.

What percentage of my credit limit should I use?

Credit utilization, the percentage of your available credit you are using, accounts for 30% of your FICO score. Most experts recommend keeping utilization below 30%, and those with excellent credit scores typically keep it below 10%. This applies both to individual cards and to your total utilization across all cards. Paying your balance in full each month naturally keeps utilization low and also avoids interest charges.

Does checking your own credit score hurt it?

No. Checking your own credit score is a soft inquiry and has no effect on your score. Hard inquiries, which occur when a lender checks your credit in response to an application, do affect your score slightly, typically by less than five points, and their effect fades within 12 months. You can and should check your own credit report regularly without any concern about damaging your score.

Can you build credit without a credit card?

Yes. Credit-builder loans from credit unions are specifically designed to establish credit without requiring a card. Reporting rent payments through services like Experian RentBureau or rent-reporting apps adds a positive payment history. Some utilities and phone carriers also report on-time payments. However, credit cards remain the most efficient tool for building credit quickly because of how frequently the positive activity is reported and how directly they affect the two biggest score factors.