Economic: Your company offers free snacks in the kitchen. Within weeks, the fridge is always empty by 10 AM, people stockpile snacks at their desks, and the budget triples. You didn't anticipate this, it's just food.

But you encountered a fundamental economic principle: when something is free (zero price), demand becomes effectively infinite. The cost to acquire is zero, so people take until they're full, then take more "just in case."

Economic principles aren't just about money and markets, they're about how humans make choices under scarcity. Every decision involves tradeoffs, opportunity costs, and responses to incentives.

Understanding these principles clarifies behavior that seems irrational, explains why policies create unintended consequences, and reveals patterns across vastly different domains.

This article explains core economic principles in plain language, without jargon or math, showing how they apply far beyond traditional economics to everyday decisions, organizational behavior, and systems design.

Core Principle 1: Scarcity and Tradeoffs

The Foundation

Economics starts with scarcity: Resources (time, money, attention, materials, energy) are limited. Desires are unlimited.

Result: You can't have everything. Every choice means giving up something else.

This isn't about money, it's about fundamental constraints.

"The first lesson of economics is scarcity: there is never enough of anything to fully satisfy all those who want it.", Thomas Sowell

Tradeoffs Are Unavoidable

Choosing X means not choosing Y.

Examples:

| Choice | Tradeoff |

|---|---|

| Study for exam | Give up socializing that evening |

| Hire engineer | Can't afford designer with same budget |

| Build feature A | Delay feature B (limited development time) |

| Server reliability | More cost, or accept downtime risk |

Pretending tradeoffs don't exist doesn't eliminate them, it just makes them unconscious and unmanaged.

TANSTAAFL: "There Ain't No Such Thing As A Free Lunch"

Every apparent "free" thing has hidden costs:

"Free" social media:

- Cost: Your attention, data, privacy

- You're not the customer; you're the product

"Free" shipping:

- Cost: Bundled into product price

- Not free, just invisible

"Free" features:

- Cost: Complexity, maintenance burden, cognitive load

Economic principle: Costs exist whether visible or not. Making costs invisible doesn't eliminate them, it hides tradeoffs.

Core Principle 2: Opportunity Cost

Definition

Opportunity cost: The value of the next-best alternative you give up when making a choice.

It's not just the dollar cost, it's what you could have done with those same resources.

"In the department of economy, an act, a habit, an institution, a law, gives birth not only to an effect, but to a series of effects. Of these effects, the first only is immediate; it manifests itself simultaneously with its cause, it is seen. The others unfold in succession, they are not seen.", Frédéric Bastiat

Examples

Spend $50,000 on marketing campaign:

- Dollar cost: $50,000

- Opportunity cost: Could have hired engineer for a year, built new feature, or saved for harder times

Spend evening watching TV:

- Dollar cost: $0

- Opportunity cost: Could have read, exercised, worked on side project, spent time with family

CEO spends 10 hours on task junior employee could do:

- Dollar cost: CEO salary doesn't change

- Opportunity cost: 10 hours not spent on strategy, major decisions, or leadership

Why Opportunity Cost Matters

Ignoring opportunity cost leads to:

| Mistake | Why It Happens | Example |

|---|---|---|

| Sunk cost fallacy | Focus on spent costs, ignore future opportunities | Continue failing project because "we've already invested so much" |

| False economies | Save money but lose more value elsewhere | Cheap tools save $100, waste 20 hours of expensive time |

| Misallocated time | High-value people do low-value work | Executive does admin work (saves $30/hr cost, wastes $500/hr value) |

Decision rule: Compare opportunity costs, not just dollar costs.

Ask: "What am I giving up by choosing this?"

Core Principle 3: Incentives Matter

The Fundamental Principle

People respond to incentives.

Change incentives → Change behavior

Often in unexpected ways (including second-order effects).

"One of the great mistakes is to judge policies and programs by their intentions rather than their results.", Milton Friedman

Why Incentives Are Powerful

Incentives signal:

- What's rewarded

- What's punished

- What's tolerated

- What matters to the system

People optimize for what's measured and rewarded, not necessarily what you want.

Examples of Incentive Effects

Example 1: Cobra Effect (India, British Colonial Era)

Problem: Too many cobras in Delhi

Policy: Pay bounty for dead cobras

Intent: Reduce cobra population

Incentive created: Profit from cobras

Result:

- People bred cobras to kill for bounty

- Program canceled

- Breeders released cobras

- Cobra population increased

Lesson: Incentives can backfire spectacularly.

Example 2: Soviet Nail Factory

Goal: Produce useful nails

Metric/Incentive: Tons of nails produced → bonuses

Result: Factories produced huge, useless nails (maximized weight)

Changed metric: Number of nails produced → bonuses

Result: Factories produced tiny, useless nails (maximized count)

Lesson: People optimize for the measured incentive, not the underlying goal.

Example 3: Wells Fargo Account Scandal

Incentive: Bonuses for opening new accounts

Intent: Grow customer relationships

Result:

- Employees opened millions of unauthorized accounts

- Customers didn't know or want them

- Massive scandal, billions in fines

Lesson: Aggressive incentives without checks create fraud.

Unintended Consequences

Whenever you create incentive, ask:

- What behavior does this reward?

- What's the easiest way to game this?

- What unmeasured factors might suffer?

Test: "If I wanted to maximize my rewards without achieving the actual goal, how would I do it?"

If answer is obvious, incentive is poorly designed.

Core Principle 4: Marginal Thinking

Definition

Marginal thinking: Decisions are made at the margin, comparing the next unit's cost and benefit, not the total.

Key insight: Past costs are sunk. Only future costs and benefits matter.

Why "Average" Misleads

Average cost/benefit: Total divided by quantity

Marginal cost/benefit: Cost/benefit of the next unit

Decisions happen at the margin, not the average.

Example: Should you go to the gym?

Wrong framing (averages):

- Gym membership: $60/month

- Average cost per visit: $60 / visits per month

- "If I only go twice, that's $30/visit, too expensive!"

Right framing (marginal):

- Membership already paid (sunk cost)

- Marginal cost of next visit: $0 (plus time/effort)

- Marginal benefit: Health, energy, stress relief

- Decision: Compare marginal cost (time) vs. marginal benefit (value of workout)

Marginal thinking: Go to gym if value of this workout > value of next-best use of time.

Example: Should restaurant stay open late?

Wrong framing (average):

- Need to cover all costs: rent, utilities, salaries, food cost, etc.

- Average cost per meal: $40

- Average revenue per meal: $35

- "We lose $5 per meal, close!"

Right framing (marginal):

- Rent, utilities already paid (sunk costs)

- Marginal cost: Food cost ($15), hourly labor ($50)

- Marginal revenue: Late customer meals ($35 each)

- If 3+ customers in hour: $105 revenue > $95 cost

- Stay open as long as marginal revenue > marginal cost

Sunk costs don't matter for decision. Only incremental costs and revenues.

Sunk Costs

Sunk cost: Already spent, can't be recovered.

Sunk cost fallacy: Continuing because "we've already invested so much."

Economic principle: Sunk costs are irrelevant. Only future costs and benefits matter.

Example: Failing project

Situation:

- Spent $500K and 18 months on project

- Forecast: Need $300K and 12 more months to finish

- Expected value if finished: $200K

Sunk cost fallacy reasoning:

- "We've already invested $500K, can't give up now!"

- Continue project

Marginal reasoning:

- $500K is sunk (irrelevant)

- Decision: Spend $300K to get $200K?

- No, lose $100K more

- Cancel project

Hard emotionally, right economically.

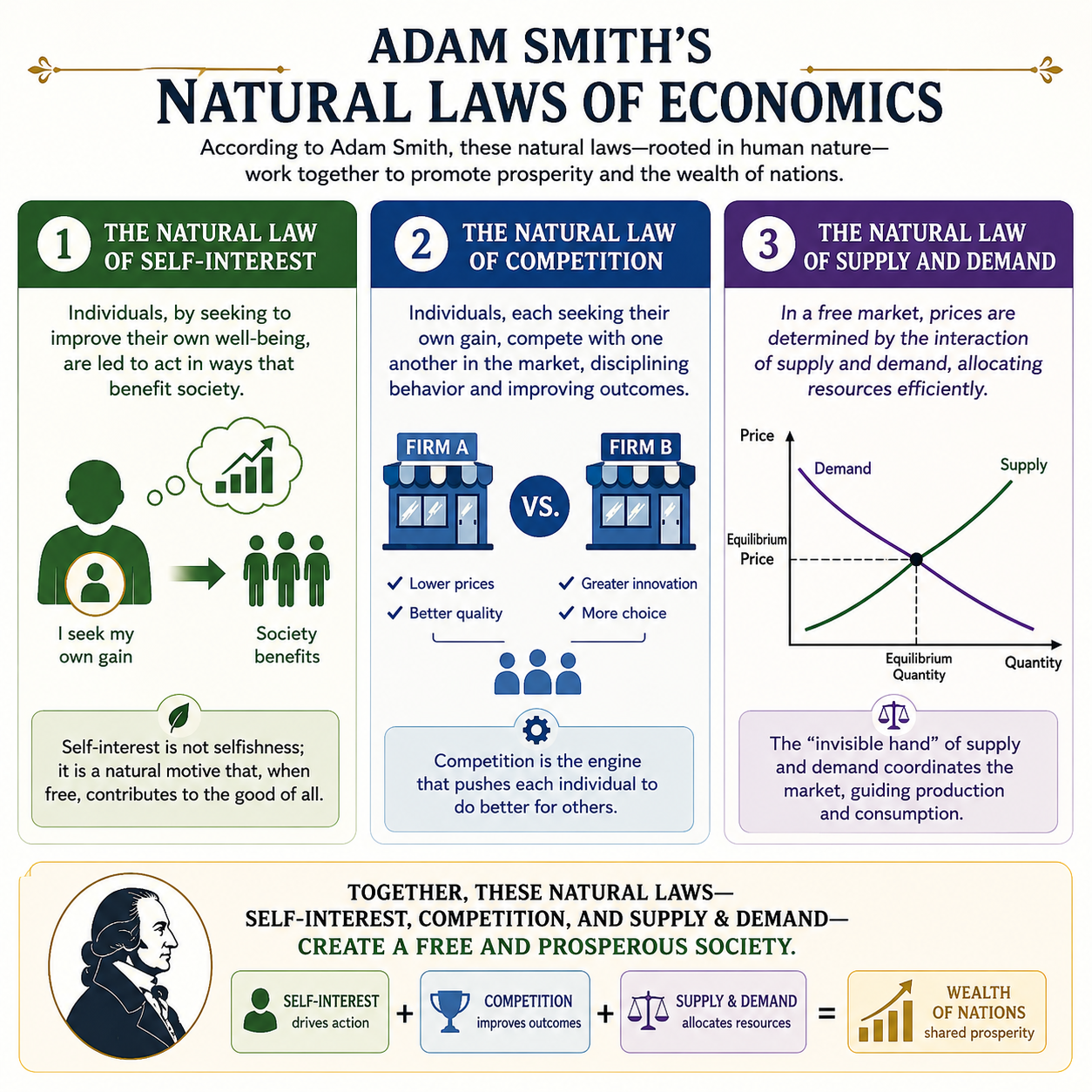

Core Principle 5: Supply and Demand

The Basics

Supply: How much sellers willing to provide at given price

Demand: How much buyers willing to purchase at given price

Price: Adjusts until supply = demand (equilibrium)

The Mechanism

Price too high:

- Demand low (expensive)

- Supply high (profitable)

- Surplus → Price falls

Price too low:

- Demand high (cheap)

- Supply low (unprofitable)

- Shortage → Price rises

Equilibrium: Price where quantity supplied = quantity demanded

Why It Matters Beyond Markets

Supply and demand apply to:

- Labor markets (salaries adjust to balance job openings and applicants)

- Attention (scarce attention drives content creators to compete)

- Meeting room availability (scheduling conflicts signal undersupply)

- Open source contributions (project popularity affects contributor supply)

Anywhere scarcity meets human choice, supply-and-demand dynamics emerge.

"It is not from the benevolence of the butcher, the brewer, or the baker that we expect our dinner, but from their regard to their own interest.", Adam Smith

Example: Developer salaries

Supply: Developers seeking jobs

Demand: Companies hiring developers

Observation: Salaries rise when demand > supply

Why:

- Companies compete for talent

- Bidding war pushes salaries up

- Higher salaries attract more people to learn development (supply increases)

- Eventually equilibrium (salaries stabilize)

Policy implication: Can't legislate high-demand skills into low salaries, market adjusts.

Price Controls and Shortages

Price ceiling (maximum price):

- If below equilibrium → Shortage

- Quantity demanded > quantity supplied

- Non-price rationing emerges (queues, favoritism, black markets)

Price floor (minimum price):

- If above equilibrium → Surplus

- Quantity supplied > quantity demanded

Example: Rent control

Intent: Make housing affordable

Policy: Cap rents below market rate

Result (supply-demand prediction):

- Demand increases (it's cheaper)

- Supply decreases (less profitable, landlords exit market)

- Shortage emerges

- Quality declines (no incentive to maintain)

- Black markets develop

Reality: Matches prediction in most rent-controlled cities.

Lesson: Can't repeal supply and demand by law. Constraints remain, manifest differently.

Core Principle 6: Comparative Advantage

Definition

Comparative advantage: You should specialize in what you're relatively better at, even if not absolutely better.

Counterintuitive insight: Even if you're worse at everything, you still have comparative advantage in something.

The Classic Example

Scenario:

- Alice: Writes code in 1 hour, writes docs in 2 hours

- Bob: Writes code in 3 hours, writes docs in 4 hours

Absolute advantage: Alice is faster at both tasks.

Naïve conclusion: Alice should do everything, Bob is useless.

Economic conclusion: Both should specialize based on comparative advantage.

Opportunity cost analysis:

Alice:

- 1 hour coding costs 0.5 hours of docs (opportunity cost)

- 1 hour docs costs 2 hours of coding

Bob:

- 1 hour coding costs 0.75 hours of docs

- 1 hour docs costs 1.33 hours of coding

Comparative advantage:

- Alice: Lower opportunity cost in coding (0.5 vs. 0.75) → Specialize in code

- Bob: Lower opportunity cost in docs (1.33 vs. 2) → Specialize in docs

Result with specialization:

Scenario: Need 1 code unit + 1 doc unit

No specialization (both do both):

- Alice: 1hr code + 2hr docs = 3 hours

- Bob: 3hr code + 4hr docs = 7 hours

- Total: 10 hours

With specialization:

- Alice: 2 units code = 2 hours

- Bob: 1 unit docs = 4 hours

- Trade: Alice gets docs from Bob, Bob gets code from Alice

- Total: 6 hours (40% faster)

Both benefit from specialization, even though Alice is better at everything.

Why It Matters

Implications:

- Trade creates value (both parties can gain)

- Specialization increases productivity (focus on what you're relatively best at)

- Being worse at everything doesn't mean useless (you still have comparative advantage somewhere)

Applications beyond work:

- Companies outsource non-core tasks

- Countries trade based on comparative advantage

- Teams divide work by relative strengths

Core Principle 7: Diminishing Returns

Definition

Diminishing returns: As you add more of one input (holding others constant), the marginal benefit of each additional unit declines.

Also called: Law of diminishing marginal returns, diminishing marginal utility

Examples

Eating pizza:

- 1st slice: Delicious, high value

- 2nd slice: Still good

- 3rd slice: Okay

- 4th slice: Meh

- 5th slice: Uncomfortable

- 6th slice: Sick

Each additional slice provides less satisfaction than the previous.

Studying for exam:

- First hour: Learn a lot

- Second hour: Learn less (diminishing returns)

- Hour 10: Exhausted, learn little

- Hour 14: Counterproductive (too tired)

Hiring engineers:

- Engineer #1: Massive impact

- Engineer #5: Still valuable

- Engineer #50: Marginal impact smaller (communication overhead, coordination costs)

- Engineer #500: May reduce productivity (bureaucracy, complexity)

Why It Matters

Implications for optimization:

Don't keep adding same input indefinitely.

Better: Balance inputs, diversify approaches, find complementary factors.

Example: Marketing budget

First $10K: High ROI (reach low-hanging fruit)

Next $50K: Good ROI (reach more people)

Next $500K: Diminishing returns (reaching marginal audience, higher costs per conversion)

Mistake: Keep pouring money into same channel

Better: Diversify (try new channels, improve product, invest in retention)

Core Principle 8: Prices Aggregate Information

The Insight

Prices coordinate behavior without central control.

Prices reflect:

- Scarcity of resources

- Value to users

- Costs of production

- Supply and demand conditions

All aggregated into single number.

Hayek's Knowledge Problem

Friedrich Hayek (1945): Knowledge is dispersed throughout society.

"The price system is just one of those formations which man has learned to use (though he is still very far from having learned to make the best use of it) after he had stumbled upon it without understanding it.", Friedrich Hayek

No central planner can know:

- What everyone wants

- What everyone can produce

- Best use of every resource

Prices solve this:

- High price signals scarcity → allocate carefully

- Low price signals abundance → use freely

- Price changes signal changing conditions → adjust behavior

Example: Pencil production (I, Pencil)

No one person knows how to make a pencil:

- Requires wood (forestry), graphite (mining), rubber (agriculture/chemistry), metal (smelting), paint, glue

- Thousands of people, different countries

- No central coordinator

How it works:

- Prices coordinate

- If graphite scarce → price rises → pencil makers economize, miners produce more

- If wood abundant → price low → use freely

Result: Pencils exist, no master plan needed.

Implications

When prices are missing or distorted:

- Coordination breaks down

- Shortages or surpluses emerge

- Resources misallocated

Examples:

- Soviet price controls → chronic shortages, waste

- Free resources → overconsumption (tragedy of commons)

- Internal company "free" resources → misallocation (IT time, design time treated as unlimited)

Solution: Create prices (or price-like signals) to coordinate decisions.

Applying Economic Principles

Application 1: Designing Incentives

Principles:

- Incentives matter (people respond)

- Marginal thinking (optimize at decision point)

- Unintended consequences (gaming)

Design process:

- Define actual goal (not proxy)

- Test: How would someone game this incentive?

- Balance multiple metrics (resist gaming)

- Monitor for unintended consequences

Example: Support team incentives

Goal: High-quality customer support

Bad incentive: Tickets closed per hour

- Gaming: Close without solving, reopen later

Better incentive:

- Tickets closed + Customer satisfaction + First-contact resolution rate

- Harder to game all three simultaneously

Application 2: Resource Allocation

Principles:

- Opportunity cost (what you're giving up)

- Diminishing returns (don't over-invest in one area)

- Comparative advantage (specialize)

Process:

- Identify opportunity costs

- Allocate to highest-value uses first

- Stop when marginal benefit < marginal cost

- Regularly reassess (opportunity costs change)

Application 3: Pricing Decisions

Principles:

- Supply and demand (find equilibrium)

- Marginal cost (don't include sunk costs)

- Price signals value and coordinates behavior

Approach:

- Price above marginal cost (need profit)

- Test elasticity (how demand responds to price changes)

- Use pricing to manage demand

- Accept that prices exclude some customers (tradeoff vs. over-capacity)

Application 4: Trade and Specialization

Principles:

- Comparative advantage (specialize in relative strengths)

- Trade creates value (both parties gain)

Application:

- Outsource low-comparative-advantage tasks

- Focus team on core strengths

- Trade (internal or external) beats self-sufficiency

Common Misconceptions

Misconception 1: Economics = Money

Reality: Economics is about choice under scarcity.

Money is one resource, but:

- Time, attention, energy, materials also scarce

- Economic principles apply to non-monetary decisions

Misconception 2: People Are Perfectly Rational

Reality: People are boundedly rational, biased, emotional. Behavioral economics documents these biases in detail.

But:

- Economic principles describe aggregate patterns better than individual predictions

- Incentives still matter, even for "irrational" people

- Principles are framework, not perfect prediction

Misconception 3: Selfishness Is Required

Reality: Economic principles don't require selfishness.

They work with:

- Altruism (people respond to incentives to help)

- Social norms (reputation matters, community values)

- Mixed motivations (self-interest + caring about others)

Key: Whatever people value, incentives affect behavior.

Misconception 4: Markets Are Always Best

Reality: Markets work well under certain conditions.

Market failures exist:

- Externalities (costs/benefits to third parties not captured in price)

- Public goods (non-excludable, non-rival)

- Information asymmetry (one party knows more)

- Monopolies (no competition)

Economic principles help identify when markets work and when they fail.

Conclusion: Principles, Not Prescriptions

Economic principles are:

- Descriptive frameworks (how the world works)

- Not ideological (apply regardless of political views)

- About constraints (scarcity, tradeoffs, incentives)

- Broadly applicable (beyond traditional economics)

Core principles:

- Scarcity and tradeoffs: Resources limited, choices involve giving something up

- Opportunity cost: Real cost is best alternative forgone

- Incentives matter: People respond to rewards and punishments, often unexpectedly

- Marginal thinking: Decisions at the margin, sunk costs irrelevant

- Supply and demand: Prices adjust to balance what people want and what's available

- Comparative advantage: Specialize in relative strengths, trade creates value

- Diminishing returns: More of same input yields declining marginal benefit

- Prices aggregate information: Coordinate behavior without central control

Practical takeaways:

- Think in tradeoffs (no free lunch)

- Consider opportunity costs (what am I giving up?)

- Design incentives carefully (anticipate gaming)

- Use marginal thinking (ignore sunk costs, focus on incremental)

- Respect supply-demand dynamics (constraints manifest somehow)

- Leverage comparative advantage (specialize and trade)

- Watch for diminishing returns (diversify, balance)

- Use prices to coordinate (when possible)

Understanding economic principles doesn't require math or jargon.

It requires thinking about choices, constraints, and how humans respond to incentives. These principles function as mental models, lenses that bring hidden structure into view.

Master these principles, and much that seemed irrational or confusing becomes clear.

Sources & Further Reading

Sowell, T. (2014). Basic Economics: A Common Sense Guide to the Economy (5th ed.). Basic Books.

Harford, T. (2012). The Undercover Economist (Revised ed.). Oxford University Press.

Hayek, F. A. (1945). "The Use of Knowledge in Society." American Economic Review, 35(4), 519–530.

Smith, A. (1776). An Inquiry into the Nature and Causes of the Wealth of Nations. W. Strahan and T. Cadell.

Ricardo, D. (1817). On the Principles of Political Economy and Taxation. John Murray.

Friedman, M. (1962). ""Capitalism and Freedom."" University of Chicago Press.

Kahneman, D., & Tversky, A. (1979). "Prospect Theory: An Analysis of Decision under Risk." Econometrica, 47(2), 263–291.

Thaler, R. H., & Sunstein, C. R. (2008). Nudge: Improving Decisions About Health, Wealth, and Happiness. Yale University Press.

Coase, R. H. (1937). "The Nature of the Firm." Economica, 4(16), 386–405.

Akerlof, G. A. (1970). "The Market for 'Lemons': Quality Uncertainty and the Market Mechanism." Quarterly Journal of Economics, 84(3), 488–500.

Levitt, S. D., & Dubner, S. J. (2005). Freakonomics: A Rogue Economist Explores the Hidden Side of Everything. William Morrow.

Kerr, S. (1975). "On the Folly of Rewarding A, While Hoping for B." Academy of Management Journal, 18(4), 769–783.

Read, L. E. (1958). "I, Pencil: My Family Tree as Told to Leonard E. Read." The Freeman.

Buchanan, J. M., & Tullock, G. (1962). "The Calculus of Consent: Logical Foundations of Constitutional Democracy." University of Michigan Press.

Ostrom, E. (1990). Governing the Commons: The Evolution of Institutions for Collective Action. Cambridge University Press.

About This Series: This article is part of a larger exploration of principles and laws. For related concepts, see [Tradeoffs: The Universal Law], [Cognitive Principles That Shape Decisions], [Constraints That Govern Systems], and [Why Principles Outlast Tactics].

Incentive Design Failures: What the Research Shows

The academic literature on incentive misalignment is extensive, and its findings are consistently sobering: well-intentioned incentive systems reliably produce behavioral responses their designers did not anticipate.

Steven Kerr's 1975 paper "On the Folly of Rewarding A While Hoping for B," published in the Academy of Management Journal, remains one of the most cited management papers ever written because its central observation has not aged: organizations routinely measure and reward one set of behaviors while hoping for a different set.

The paper documented this pattern across the US military (rewarding quantifiable body counts, hoping for strategic success in Vietnam), universities (rewarding publication volume, hoping for teaching quality), and businesses (rewarding short-term financial metrics, hoping for long-term value creation).

Uri Gneezy and Aldo Rustichini's 2000 study, published in the Journal of Legal Studies, tested the effect of introducing fines at Israeli daycare centers for parents who arrived late to pick up their children. Standard economic theory predicted that fines would reduce late pickups by increasing the cost of tardiness.

The opposite occurred: late arrivals roughly doubled and did not return to previous levels even after the fines were removed. The researchers concluded that the fine converted a social norm (obligation, guilt, relationship with caregivers) into a market transaction.

Once parents had paid for the option to be late, the social cost disappeared. The economic incentive destroyed a more powerful non-economic incentive.

This finding has been replicated in related forms. Roland Benabou and Jean Tirole's 2003 theoretical framework, confirmed by multiple empirical studies, shows that external rewards can "crowd out" intrinsic motivation when the reward signals that the task is not intrinsically worth doing.

Children rewarded with prizes for drawing subsequently drew less than control groups who received no reward - the prize communicated that drawing was work rather than play, shifting the activity's meaning and the child's motivation.

Organizations that monetize employee behaviors previously governed by professional norms (patient care, academic research, teaching quality) observe similar deterioration.

The practical implication is that incentive design requires understanding not just what behavior is being rewarded but what signals the reward sends about the nature of the activity and the organization's values.

Economic laws describe how incentives work; they do not specify which incentives to create. Creating the wrong incentive with technical precision produces precisely targeted bad outcomes.

Comparative Advantage in Practice: From Ricardo to Modern Supply Chains

David Ricardo formalized comparative advantage in 1817, but the principle's practical implications have become dramatically clearer through the natural experiments of the past three decades of global trade integration.

Economists Elhanan Helpman (Harvard) and Paul Krugman (Princeton, Nobel 2008) extended Ricardian trade theory to explain why similar countries trade similar goods - a pattern that classical comparative advantage cannot fully explain.

Their "new trade theory" (1979-1985) incorporated economies of scale and product differentiation, showing that comparative advantage is partly created rather than simply discovered: countries develop advantage in industries where they achieve scale, which further reinforces advantage.

The China trade shock, documented by David Autor, David Dorn, and Gordon Hanson in a 2013 American Economic Review paper, demonstrated the distributional consequences of comparative advantage realignment at scale.

That paper found import competition from China explains roughly a quarter of the contemporaneous decline in US manufacturing employment over the period, with concentrated geographic impact on communities whose local economies depended on those industries. A related follow-up study by the same authors, covering 1999 to 2011, put the total US job losses from Chinese import competition at approximately 2 million, including manufacturing and its local spillover effects on other sectors.

The aggregate gains from trade (lower consumer prices, resource reallocation to higher-value activities) were real but diffuse and slow; the costs were concentrated and immediate.

Ricardo's principle correctly predicted the direction of trade flows; it did not predict how the adjustment costs would be distributed within countries, or that those costs would be borne by specific communities unable to diversify.

At the firm level, Michael Porter's (Harvard Business School) value chain analysis (1985) translated comparative advantage into operational strategy.

Porter documented how firms in the same industry with identical access to factor inputs could develop sustainable competitive advantages by configuring their value chains differently - choosing which activities to perform internally versus outsource based on relative capability.

Nike's decision to retain design and marketing while outsourcing manufacturing is a direct application of comparative advantage logic at the firm level: Nike has comparative advantage in brand management and product design relative to its manufacturing capability, and the global labor market offers comparative advantage in assembly relative to what Nike could achieve internally.

The principle's durability across scales - from Ricardo's national trade examples to Porter's firm-level value chains to individual time allocation - reflects that comparative advantage describes a mathematical property of opportunity costs rather than a historical observation about trade.

Any agent with differentiated capabilities operating in an exchange economy will face comparative advantage tradeoffs in resource allocation, whether that agent is a person, firm, or country.

Frequently Asked Questions

What are the most important economic principles?

Supply and demand, opportunity cost, incentives matter, marginal thinking, comparative advantage, and trade creates value.

What is opportunity cost?

Opportunity cost is the value of the next best alternative you give up when making a choice, the real cost of decisions.

How do incentives work?

People respond to incentives, often in ways that seem irrational but are locally optimal, change incentives, change behavior.

What is marginal thinking?

Marginal thinking focuses on the next unit’s cost and benefit, decisions are made at the margin, not about totals.

What is comparative advantage?

Comparative advantage means specializing in what you’re relatively better at, even if not absolutely better, the basis of beneficial trade.

Why do prices matter?

Prices aggregate dispersed information about scarcity and value, coordinating behavior without central control.

Are people rational economic actors?

People are somewhat rational but bounded, biased, and influenced by psychology, economic principles explain trends better than individuals.

How do economic principles apply outside markets?

Economic principles (incentives, tradeoffs, opportunity cost) apply to any situation involving scarce resources and human choice.